September 30, 2022 – The law of unintended consequences states that the actions of people, typically governments, are rarely fully thought through and as a result, have unanticipated effects.

No more recent example of unintended consequences resulted from the Inflation Reduction Act of 2022, an amusingly-named law that included policies that would likely increase inflation markedly.

In addition, the formation of the law was one of the most shameful examples of crony capitalism in recent history.

Specifically, the private equity industry has long enjoyed one of the most egregious tax loopholes, the carried interest tax loophole. This preferential tax treatment has allowed private equity firms to enjoy a reduced capital gains tax applied to their performance fees (also known as “carry”), as opposed to traditional income tax that is applied to all others’ incomes. For years, private equity firms have successfully lobbied against bills that aimed to end the quirk in the tax code that allows PE executives to pay lower tax rates than the general working public.

This unjustifiable loophole was set to be closed once and for all, despite the private equity industry fighting it assiduously over decades, until one Democratic Senator objected. For what reason, we will never know (however, I wouldn’t be surprised to see a new Vice Chair at KKR in the near future!).

In exchange for doing away with the carried interest tax provision, the deal that Democratic leaders made with the opposing Senator included a 1% excise tax on share buybacks.

Politicians have long railed against corporate share repurchases. As intelligent investors know, this criticism is misguided. Share buybacks are just an efficient means to return cash to the owners of a business. Share repurchases are not utilized to manipulate share prices or enrich executives. There is nothing nefarious going on with share buybacks.

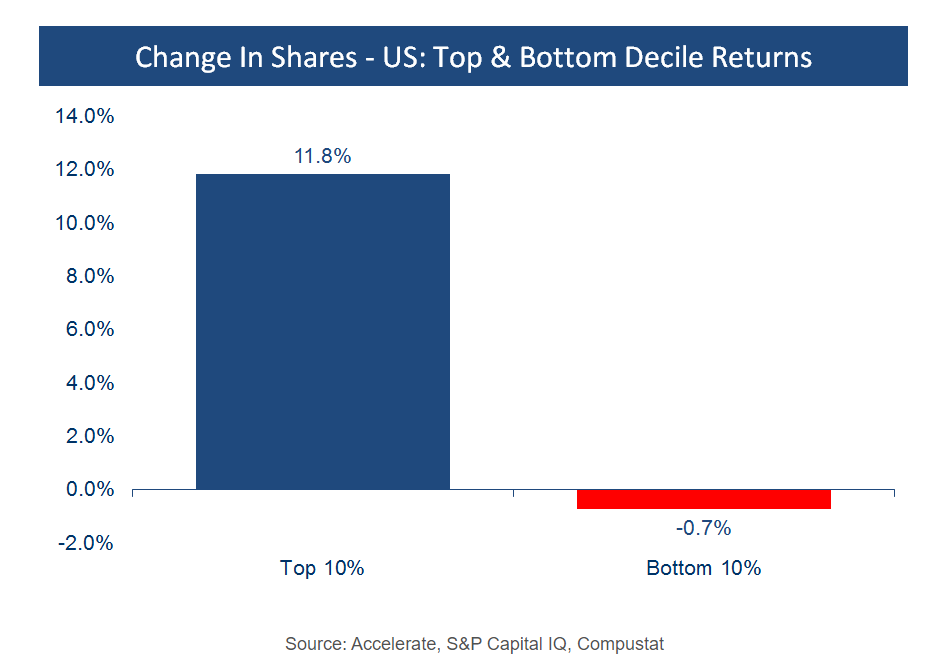

In addition, the 1% excise tax on share buybacks punishes good investments. This tax, to be paid for by the companies and not the shareholders, will only serve to punish good investments. In terms of share price performance, historically, the top decile of share repurchasers have gained 11.8% per annum while the top share issuers have lost 0.7% per year. Over 20 years, this results in a 10x difference in an investor’s portfolio.

Any way you measure it, the excise tax was poorly thought through and executed even worse.

The unintended consequences of the Inflation Reduction Act, in addition to its inflationary policies, was the potential 1% excise tax on SPACs.

Specifically, the excise tax may apply to a public U.S. company that repurchases any of its shares after December 31st, 2022. Repurchases can refer to redemptions or any other transactions in which the company uses its cash to retire shares. However, for the excise tax to be applicable, the shares repurchased or redeemed would be netted against any shares issued in that taxable year. The excise tax is paid by the corporation, not the stockholder. It is equivalent to an additional corporate income tax but is applied even if the company is not profitable.

There are a lot of nuances, and related uncertainties, with respect to the application of the tax for SPAC redemptions.

That being said, there are several situations in which the excise tax will not apply under the current law, including:

- Non-U.S.-domiciled SPACs (which account for 45% of the current market) either liquidating, deSPACing or extending their deadlines, excluding those that redomesticate.

- U.S.-domiciled SPACs that are completing a business combination, given the netting rule of shares issued to the target company and/or the PIPE financing would exceed the redeemable stock.

- U.S.-domiciled SPACs liquidating before year-end 2022.

Scenarios of concern in which the excise tax may apply to SPACs that are U.S.-domiciled and are either liquidating or staging an extension vote (along with a concurrent redemption) in 2023 or later.

The key question facing SPAC investors is: who will pay for the tax, the sponsor, or the trust account (i.e. investors’ redemption payments)?

The constating documents for existing SPACs are unclear, given they predated the announcement of the Inflation Reduction Act. However, for recent SPAC IPO filings, the majority explicitly state that the sponsor would be liable for the tax, if applicable. In addition, recent proxy statements related to SPAC deadline extensions have stated that the SPAC sponsor would be liable for any applicable excise tax.

In any event, clearly, the share buyback tax was not meant for return of capital scenarios such as SPAC redemptions because investors are just getting their money back (plus accrued interest). Imagine you put money in a checking account and the Government wants to take 1% of anything you take out.

Hopefully, the U.S. Treasury Department provides additional guidance with respect to the application of the excise tax and its application to SPACs. Until then, uncertainty will reign.

Many sponsors are taking this in stride and still looking to do deals. Despite the regulatory pressure, rising interest rates, and equity bear market, we are still seeing sponsors IPO their SPACs (4 in September) and remain committed to completing a business combination.

The Accelerate AlphaRank SPAC Monitor details various metrics on the current opportunity set while offering details on every individual SPAC currently outstanding. The Accelerate AlphaRank SPAC Effective Yield tracks the average arbitrage yield offered. The Accelerate AlphaRank SPAC Index tracks the price return of the SPAC universe.

* AlphaRank is exclusively produced by Accelerate Financial Technologies Inc. (“Accelerate”). The Accelerate Arbitrage Fund may hold a number of securities discussed in this research. Visit AccelerateShares.com for more information.