May 1, 2022 – We can discuss risk until the cows come home, however, some investors only begin to consider risk management after they are faced with significant market losses.

Every portfolio manager can use Mike Tyson’s quote, “everyone has a plan until they get punched in the mouth”, at least once. I will use mine here.

No matter what, risk is omnipresent. Significant market drawdowns have the habit of making risk visceral.

Given the depressing performance of traditional asset classes in April, with the S&P 500 down -10.2% and long-term Treasury bonds down -9.3%, it makes sense to revisit the concept of risk management.

One asset class that can help with risk management by acting as a steady hand is the Special Purpose Acquisition Company.

Examining the structure of the SPAC, the most important aspect is the downside protection.

The Net Asset Value of a SPAC consists of U.S. Treasury bills, perhaps the safest asset on the planet.

The typical SPAC has more than $10.00 of cash in trust, accruing interest from its short-term T-bills. Most SPACs these days come to market with what is called an overfunded trust, meaning they will have a NAV of $10.20 or $10.30 right out of the gate. The sponsor provides this overfunding of the SPAC’s trust to entice allocators to invest in their blank check company.

As long as an investor buys at or below a SPAC’s redeemable NAV, which consists of T-bills, they will have an investment with the downside protection of the safest asset on the planet.

The beautiful thing about a SPAC acquired at the right price (remember – always at or below NAV!) is that along with providing solid downside protection through its redeemable NAV consisting of T-bills, it also offers significant upside optionality through both a positive deal announcement and potential warrant value.

Source: Accelerate

Source: Accelerate

Nonetheless, in the current market environment, most allocators are concerned with the return of capital not the return on capital. SPACs provide both, however, the rock-solid downside protection provides investor portfolios with stability even while traditional asset classes are rapidly falling.

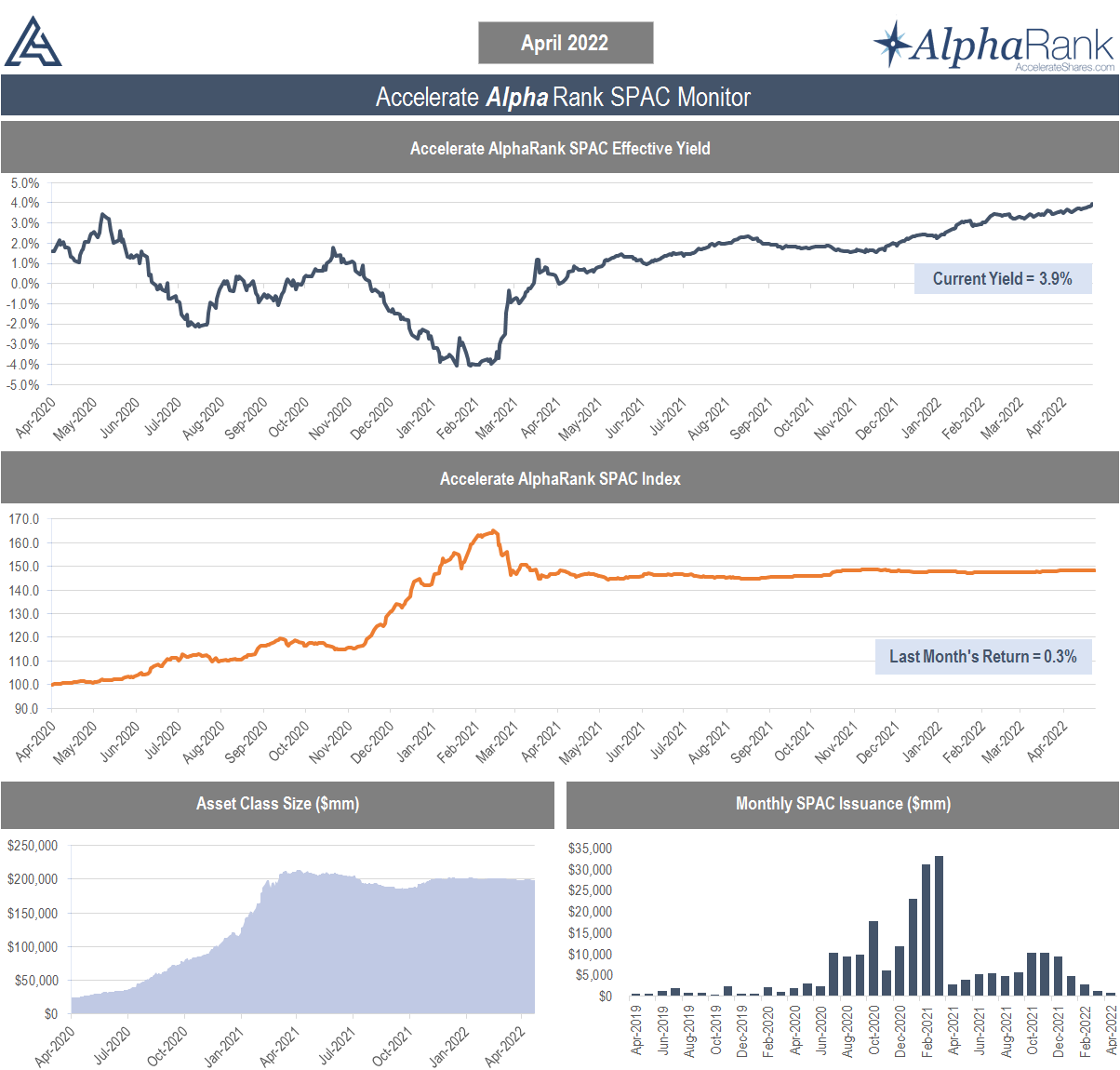

As stocks and bonds both declined precipitously in April, the SPAC Index rose 0.2% in a calm and uneventful manner. In addition, 7 of the 9 SPAC IPOs in the month traded above par. SPACs are truly a honey badger asset class, impervious to geopolitical turmoil, regulatory pressure or even overzealous central banks.

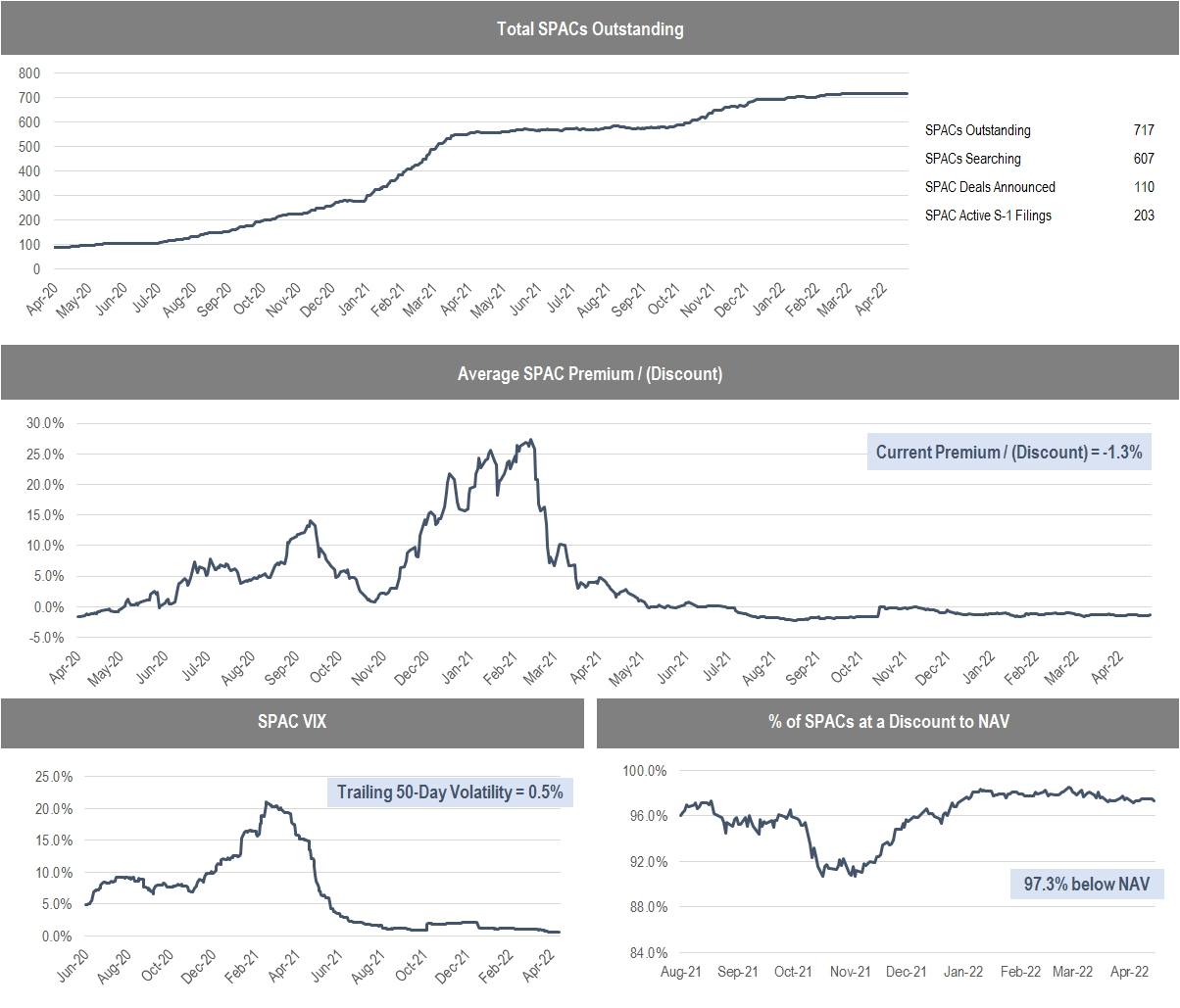

97.3% of SPACs are trading at a discount to NAV, offering an average arbitrage yield of 3.9%. The most compelling part of generating yield from discounted SPACs is their low duration, which pays off in spades as interest rates skyrocket. The average SPAC has a remaining duration of less than 10 months.

Currently, more than $3.8 billion of arbitrage profit is available in discounted SPACs for enterprising investors interested in picking it up. This “free money” is in addition to the SPAC’s downside protection and upside optionality. Basically, investors receive a very generous yield while attaining solid downside protection and exposure to an additional call option-like potential payoff. You can’t make this stuff up.

In any event, SPACs remain a great place to hide. Let the numbers do the talking instead of being influenced by the media’s negative bias toward the asset class. As traditional asset classes get slammed by choppy waters, SPACs act as a portfolio ballast for investors in rough seas to make their financial vessels more resilient and help ensure they complete their investment journeys unscathed.

The Accelerate AlphaRank SPAC Monitor details various metrics on the current opportunity set while offering details on every individual SPAC currently outstanding. The Accelerate AlphaRank SPAC Effective Yield tracks the average arbitrage yield offered. The Accelerate AlphaRank SPAC Index tracks the price return of the SPAC universe.

* AlphaRank is exclusively produced by Accelerate Financial Technologies Inc. (“Accelerate”). The Accelerate Arbitrage Fund may hold a number of securities discussed in this research. Visit AccelerateShares.com for more information.