April 28, 2022 – Turns out, it wasn’t just for the memes.

After much market speculation, on Monday, Elon Musk inked a definitive agreement to acquire Twitter.

The acquisition price came in at $54.20 cash per share, representing a 37.9% premium and an enterprise value of $44 billion.

No, Elon does not currently own Twitter. However, he may own the bird app in five months or so.

Currently, Elon does own some of the social media platform. Just weeks ago, it was disclosed that he owns 73.1 million Twitter shares, representing a 9.6% stake in the corporation. He has signed an agreement to acquire all the shares he does not own, subject to shareholder and regulatory approvals.

There are several fascinating details in this transaction.

First is the sheer size of the deal. Musk’s acquisition of Twitter represents the largest leveraged buyout in history (by a longshot). Prior to Musk’s announced $44 billion buyout, the previous record for the biggest LBO was a private equity consortium’s $32.1 billion go-private of TXU.

Source: Accelerate, CNBC

Source: Accelerate, CNBC

It is notable that in 2014, TXU filed for bankruptcy, weighed down by more than $40 billion in debt accumulated from the buyout and its struggling operations.

Second, the Twitter arbitrage spread is unwieldy, widening at a rapid and chaotic pace. It is too large to be controlled by the arbitrage community. The spread is pricing in a 40% odds of deal failure while rewarding brave arbitrageurs with a potential 31% yield if the deal closes successfully by September 30th.

Excluding the outliers, the Twitter / Musk deal represents the fourth highest arbitrage yield at 31.1%.

Source: Accelerate

Source: Accelerate

Third, many wonder why the market is ascribing only a 60% odds of Musk successfully acquiring Twitter?

The devil is in the details.

Obviously, a $44 billion acquisition represents the largest purchase by one individual.

Financing the $44 billion acquisition of a business that is expected to produce $1.4 billion of EBITDA this year requires creative solutions. And on this deal, the financiers got creative.

The financing for Musk’s leveraged buyout of Twitter consists of:

- A $21 billion equity commitment

- Debt financing of $13 billion

- Margin loan financing of $12.5 billion

A notable component is the $21 billion equity component of the financing. Specifically, $21 billion is a lot of money, even for the world’s wealthiest person. There is no insight as to where this $21 billion is coming from, given that Mr. Musk is not a sovereign wealth fund or a private equity firm.

The $13 billion of debt, supported by $1.4 billion of EBITDA represents a sky-high leverage multiple of 9.3x debt-to-EBITDA. However, that is not the most noteworthy feature of the debt financing. Specifically, the $12.5 billion margin loan will make a risk manager’s ears perk up.

The collateral for the $12.5 billion margin loan is Musk’s shares of Tesla, a notoriously volatile automobile manufacturer. Currently, Musk’s 16.7% stake in Tesla is worth $155 billion. The lenders require a loan-to-value of 20% upon deal closing, meaning he will be required to put up at least $62.5 billion of unencumbered Tesla shares as collateral. In addition, there would be a margin call at an LTV of 35%, representing a -43% decline in the value of the collateral (Tesla stock).

From a risk perspective, there are three major hurdles in a leveraged buyout:

- Shareholder vote – The Twitter buyout represents a 37.9% premium to the company’s unaffected price, in-line with the average 38.3% premium for M&A deals since 2011. In addition, Musk already owns nearly 10% of the company, while the board of directors and index funds (who would never vote against the board of directors) own almost 25%. While Kingdom Company owns 5.2% of Twitter and has indicated its opposition, the requisite majority approval is a high probability event.

- Regulatory – The buyout presents minimal, if any, issues from an antitrust perspective. The U.S. and international regulatory approvals should be forthcoming in due time.

- Financing – The financing of the largest buyout of all time, done by an individual no less, presents by far the most significant risk in the transaction. Specifically, the margin loan presents substantial market exposure to the price of Tesla shares. For example, if Tesla stock were to trade in line with its auto industry comps, a collateral shortfall event would occur, triggering a potential event of default if a margin call is not met. Basically, the margin loan financing risk is analogous to a short put option position in Tesla, whose stock is up 850% over the past five years.

Although the financing is not explicitly a condition for the merger, if the money is not available, then the deal cannot close.While a definitive agreement is notoriously difficult to wriggle out of, it is not inconceivable. Historically, 6% of announced deals have broken, while 94% have been completed successfully. Furthermore, with respect to completed deals, 1% have had their terms revised downward.

The Twitter / Musk deal currently presents investors with a potential 31% arbitrage yield if it closes in five months. However, at the current price, the market is implying just a 60% chance of completion, compared to an average of 85% for the deal universe.

The investment strategy is called risk arbitrage for a reason. While the prospective returns can be extremely attractive, especially in a low interest rate environment, it is essential to astutely manage risks.

And Musk’s historic leveraged buyout of Twitter has it in spades.

Disclosure: No Twitter position in the Accelerate Arbitrage Fund (TSX: ARB).

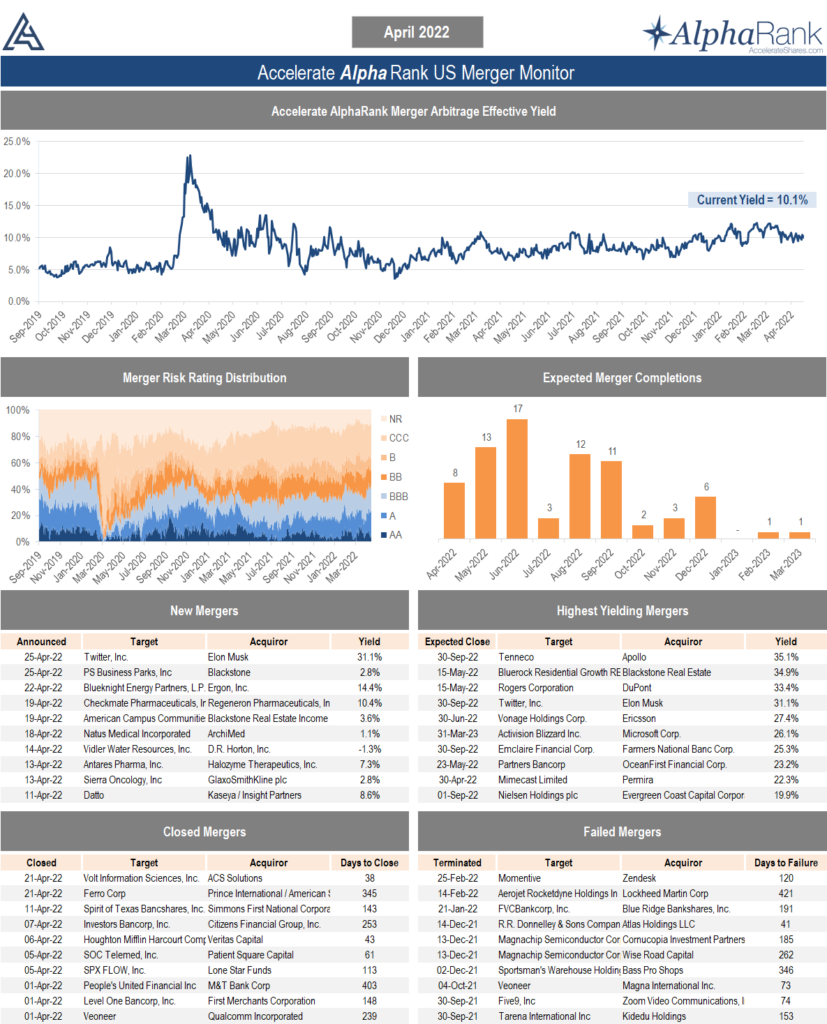

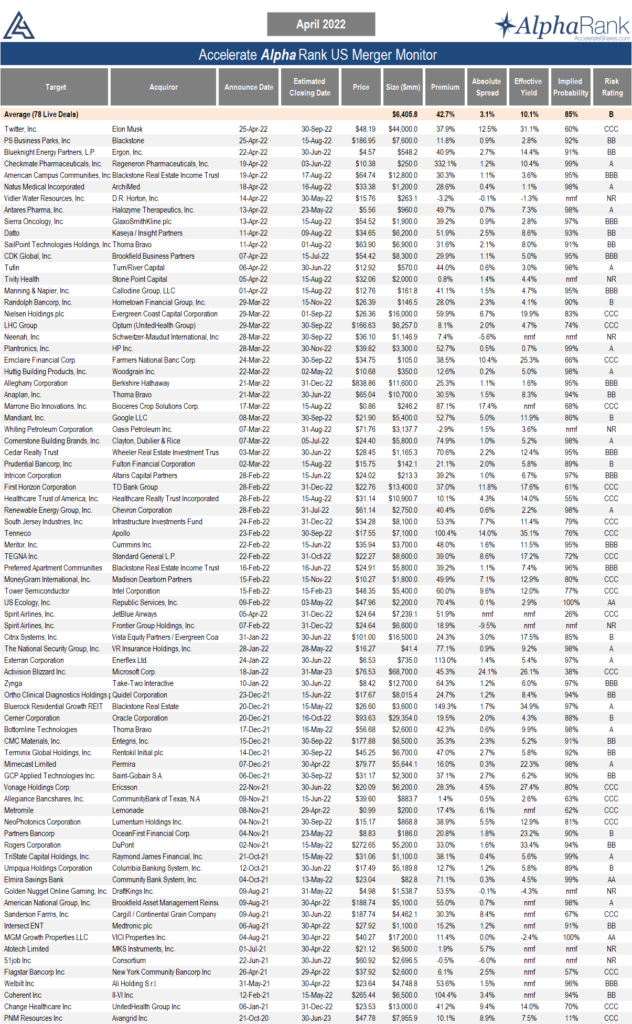

The AlphaRank Merger Monitor below represents Accelerate’s proprietary analytics database on all announced liquid U.S. mergers. The AlphaRank Merger Arbitrage Effective Yield represents the average annualized returns of all outstanding merger arbitrage spreads and is typically viewed as an alternative to fixed income yield.

Each individual merger is assigned a risk rating:

- AA – a merger arbitrage rated ‘AA’ has the highest rating assigned by AlphaRank. The merger has the highest probability of closing.

- A – a merger arbitrage rated ‘A’ differs from the highest-rated mergers only by a small degree. The merger has a very high probability of closing.

- BBB – a merger arbitrage rated ‘BBB’ is of investment grade and has a high probability of closing.

- BB – a merger arbitrage rated ‘BB’ is somewhat speculative in nature and has a greater than 90% probability of closing.

- B – a merger arbitrage rated ‘B’ is speculative in nature and has a greater than 85% probability of closing.

- CCC – a merger arbitrage rated ‘CCC’ is very speculative in nature. The merger is subject to certain conditions that may not be satisfied.

- NR – a merger rated NR is trading either at a premium to the implied consideration or a discount to the unaffected price.

The AlphaRank merger analytics database is utilized in running the Accelerate Arbitrage Fund (TSX: ARB), which may have positions in some of the securities mentioned.

* AlphaRank is exclusively produced by Accelerate Financial Technologies Inc. (“Accelerate”). Visit AccelerateShares.com for more information. Disclaimer: This research does not constitute investment, legal or tax advice. Data provided in this research should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this research is based on current market conditions and may fluctuate and change in the future. No representation or warranty, expressed or implied, is made on behalf of Accelerate as to the accuracy or completeness of the information contained herein. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Accelerate may have positions in securities mentioned. Past performance is not indicative of future results.