![]()

June 27, 2019 – The “hot hand” phenomenon occurs when a person who experiences a successful attempt has a greater chance, or positive momentum, in successful further attempts.

There were plenty of hot hands in the Toronto Raptors’ recent clinching of the NBA Championship. A prime example of the hot hand phenomenon was Raptors’ star forward Kawhi Leonard’s performance throughout the playoffs. Whether it be his series-clinching, 3-point buzzer beater against the Philadelphia 76ers, or his 10-0 run in game 5 of the finals against the venerable Golden State Warriors, Kawhi’s positive momentum showed that basketball is one of the most common areas in which the hot hand phenomenon is displayed.

When a shooter has the hot hand, give them the ball. When a gambler keeps hitting winning bets, double down.

There’s an investing analogy too. When a public company keeps beating capital markets’ expectations, buy the stock!

A Stock’s Hot Hand – Operating Momentum

A stock can have a hot hand, or positive operating momentum, when the company’s fundamental operating performance continues to exceed the expectations of the market.

There are a number of ways to measure a public company’s operating momentum. Two of our preferred operating momentum metrics include:

- Consensus EPS Revisions: The change in consensus earnings per share (EPS) expectations over time.

- Earnings Abnormal Returns: Abnormal share price performance after the release of quarterly results.

A twenty year performance simulation was run to test these operating momentum factors. The simulations ran two model factor portfolios: one that invested in the top 10% (ie. highest operating momentum) and one that invested in the bottom 10% (ie. lowest operating momentum) portfolios of stocks ranked by operating momentum, rebalanced on a monthly basis in both Canada and the U.S.

This empirical data indicates that stocks with positive operating momentum, as measured through high Consensus EPS Revisions or positive Earnings Abnormal Returns, outperform stocks with negative operating momentum.

When EPS Estimates Keep Heading Higher

You know things are going well for a company when analysts are constantly raising their earnings estimates. Conversely, when analysts are revising their earnings forecasts for a company downward, then things are likely going poorly. The share price tends to follow.

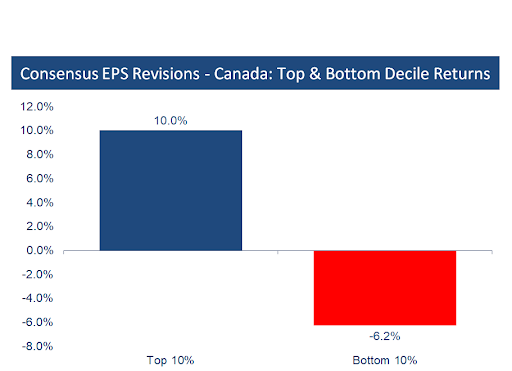

The Consensus EPS Revisions factor ranks stocks based on the month-over-month change in average analyst earnings per share estimate. The data show that the top decile of stocks whose underlying earnings estimates are increasing vastly outperform the bottom decile of stocks, or those whose earnings estimates are decreasing the most.

Source: Accelerate, Compustat, S&P CapitalIQ

Source: Accelerate, Compustat, S&P CapitalIQ

Over the past twenty years, the portfolio of the top 10% highest operating momentum stocks in Canada as measured by rising EPS revisions, rebalanced on a monthly basis, returned 10.0% annually. Over the same time period, the portfolio of the bottom 10% of stocks having the most negative EPS revisions lost -6.2% per year.

Source: Accelerate, Compustat, S&P CapitalIQ

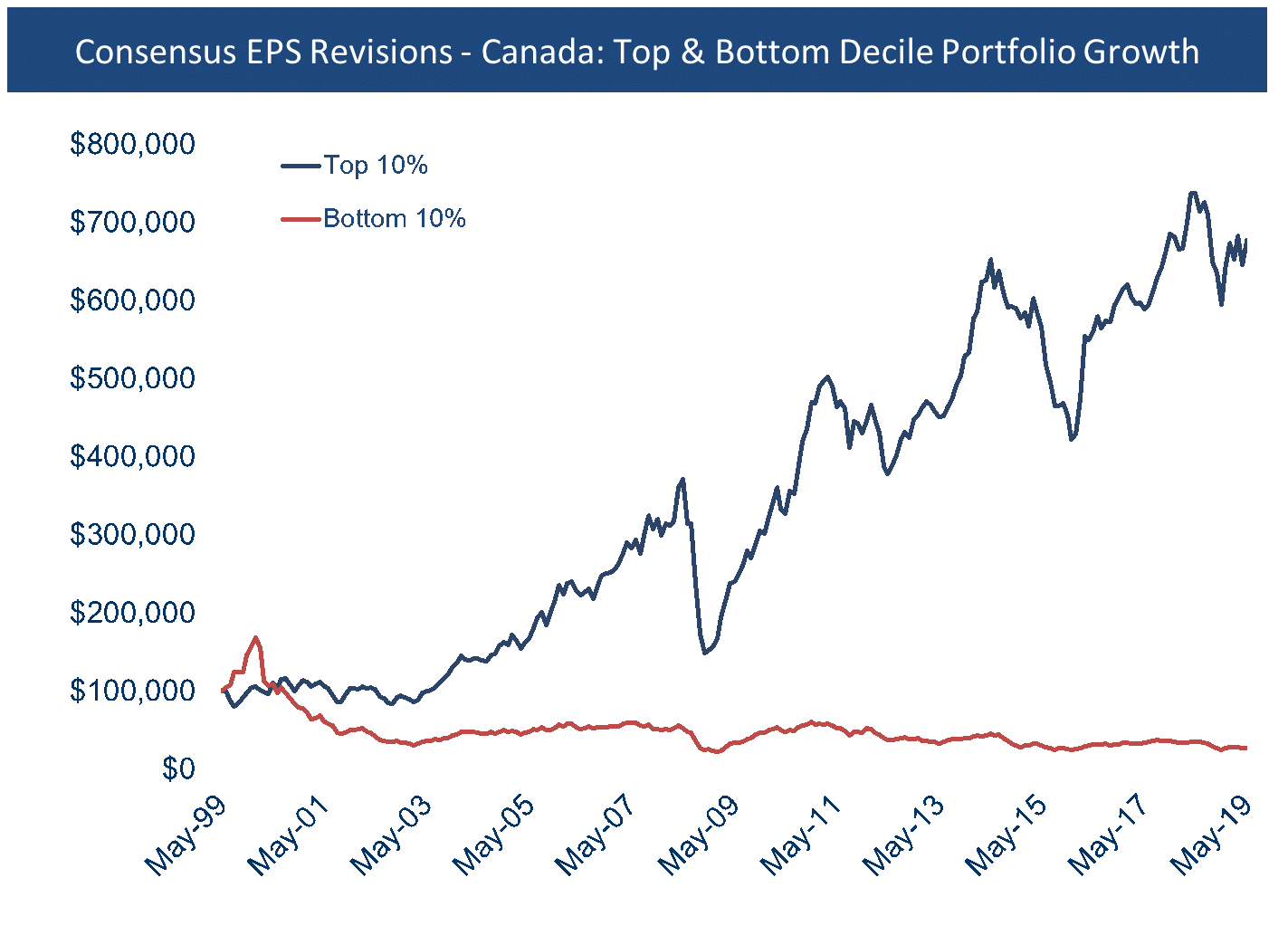

If one were to invest $100,000 in the top decile operating momentum portfolio in Canada, after twenty years it would have grown to almost $700,000. That same $100,000 invested in the bottom decile operating momentum portfolio would have shrunk to under $30,000, a loss of nearly -75%.

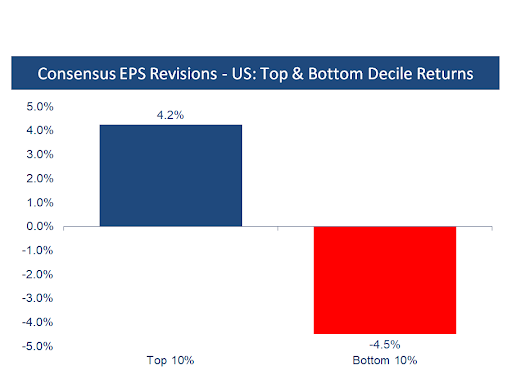

The Consensus EPS Revisions factor performance was not as significant in the U.S. as in Canada, but the long portfolio of top decile operating momentum stocks still has positive performance and vastly outperformed the negative-returning bottom decile portfolio, as seen below.

Source: Accelerate, Compustat, S&P CapitalIQ

Source: Accelerate, Compustat, S&P CapitalIQ

Over the past two decades, the portfolio holding the top 10% of U.S. stocks with the highest upward EPS revisions returned 4.2% per year, while the bottom 10% of stocks, those with the most negative EPS revisions, declined by -4.5% per year.

Source: Accelerate, Compustat, S&P CapitalIQ

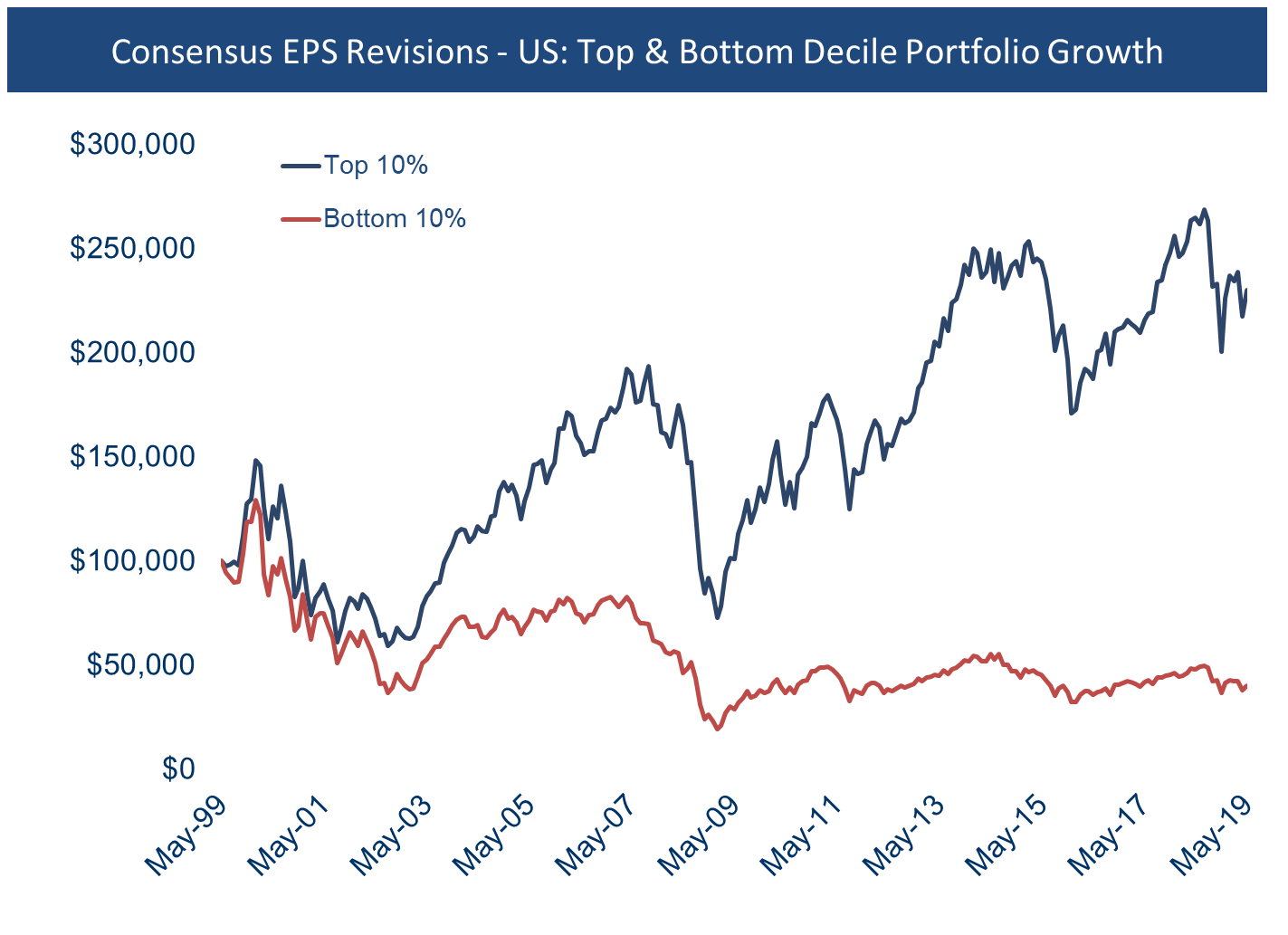

A $100,000 investment in the top 10% of U.S. stocks as measured by increasing EPS revisions would have more than doubled over twenty years while a $100,000 investment in the bottom 10% of U.S. stocks with the most negative EPS revisions would have declined to less than $40,000.

When a Stock Rallies Post Earnings

The “beat and raise”, finance parlance for when a company exceeds analyst expectations of quarterly performance and also raises guidance for near-term future performance, is typically accompanied by a stock price rally.

Earnings Abnormal Returns refers to the abnormal positive (negative) share price performance that occurs when a company’s quarterly financial performance exceeds (falls short of) expectations.

The data show that companies whose shares rally after reporting their quarterly financial results (ie. positive abnormal share price returns) typically keep going up while companies whose shares fall after releasing their quarterly reports tend to keep falling. Companies that “beat and raise” tend to continue to do so.

Source: Accelerate, Compustat, S&P CapitalIQ

Source: Accelerate, Compustat, S&P CapitalIQ

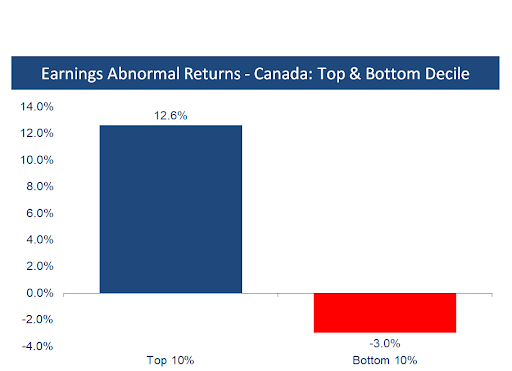

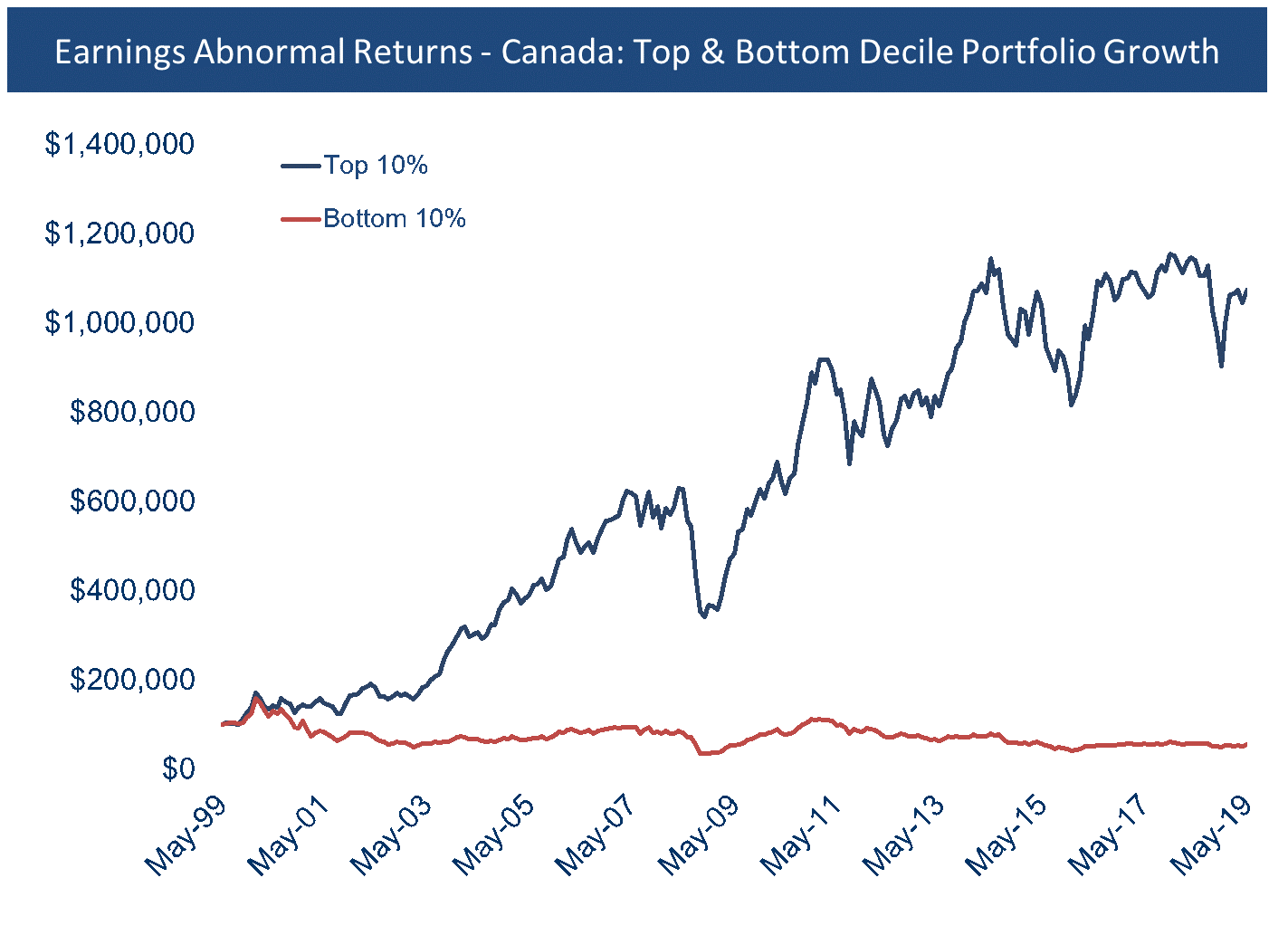

Over the twenty year simulation, the portfolio of Canadian stocks ranking in the top decile of Earnings Abnormal Returns compounded at 12.6% per year while the portfolio of bottom decile stocks with the most negative abnormal returns around their quarterly results lost -3.0% per year.

Source: Accelerate, Compustat, S&P CapitalIQ

A $100,000 investment in the portfolio of top decile ranked stocks by Earnings Abnormal Returns would have grown to approximately $1,000,000 over twenty years. A $100,000 investment two decades ago into the bottom 10% of stocks ranked by Earnings Abnormal Returns would have declined to less than $60,000.

The performance of the operating momentum factor as measured by Earnings Abnormal Returns in the U.S. was not as pronounced as in Canada, however, the U.S. portfolios did exhibit substantial alpha, or performance spread, between the top 10% and bottom the 10% ranked stocks.

Source: Accelerate, Compustat, S&P CapitalIQ

Source: Accelerate, Compustat, S&P CapitalIQ

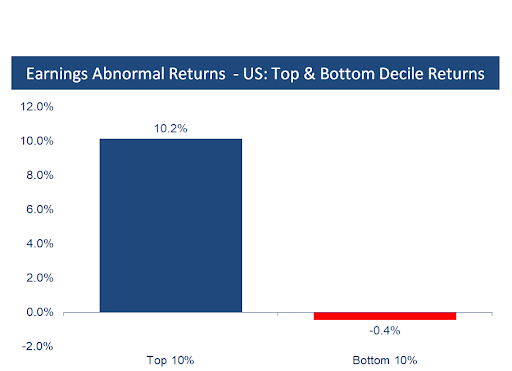

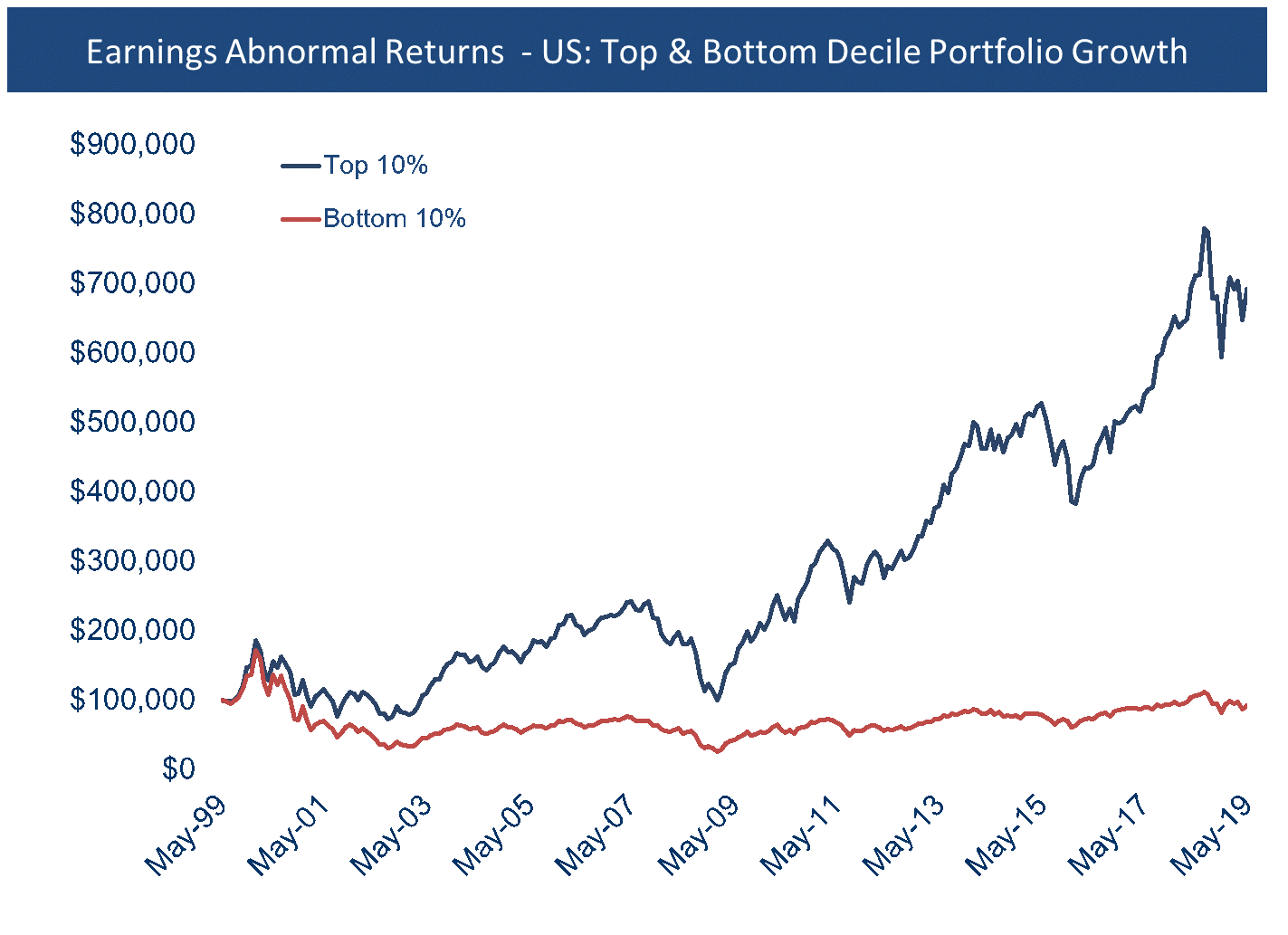

The top decile ranking of U.S. stocks with good operating momentum gained 10.2% annualized over the past twenty years. Comparatively, the bottom decile of U.S stocks, or those with the worst operating momentum as measured by Earnings Abnormal Returns, lost -0.4% per year.

Source: Accelerate, Compustat, S&P CapitalIQ

An investment of $100,000 in that top decile of U.S. stock based on Earnings Abnormal Returns operating momentum would have grown to nearly $700,000 compared to the same investment in the bottom decile of U.S. stocks, which would have shrunk to about $92,000.

Operating Momentum – Alpha On the Short Side

Over the same time period of the simulations, the past twenty years, the S&P / TSX Composite had an annualized total return of 6.9% while the S&P 500 total return was 5.8% per year.

All of the long top decile portfolios based on operating momentum beat the market, except Consensus EPS Revisions in the U.S.

However, the most interesting aspect of the data is not how much the top 10% ranked stock portfolios beat the market on average, but how much the bottom 10% ranked stock portfolios underperformed. This indicates that an enterprising investor could generate substantial alpha, or outperformance, by short selling these bottom ranked operating momentum stocks. This is a key insight that smart beta (long-only) investors miss.

Is The Hot Hand Phenomenon a Fallacy? I Think Not

While long believed to be a fallacy, the hot hand in basketball is now thought of to exist given more recent advanced statistical studies based on additional empirical evidence.

Just as the data supports the hot hand phenomenon in basketball, empirical evidence shows that the hot hand phenomenon exists in stocks, as manifested through a company’s operating momentum. Some key operating momentum characteristics include Consensus EPS Revisions and Earnings Abnormal Returns.

When a public company has a hot hand and its performance continues to exceed expectations, its stock should be bought. Conversely, when a stock is cold with poor operating momentum, it should be sold or even shorted.

Invest with a hot hand and take operating momentum into account.

-Julian