![]()

December 5, 2019 — The average homeowner will pay tens of thousands of dollars out of pocket for home insurance over their lifetime.

Every month, homeowners steadily lose money paying insurance premiums to protect their homes from negative events such as fire or flooding. From a financial perspective, this is a negative expected value investment for the insurance policyholder. The insurance only pays off if a low-probability negative event occurs, which doesn’t happen for the vast majority of the insured. If one were to look at the insurance policy as an investment, it appears to be a terrible performer. Investing in a security with a negative expected value for the chance at a low probability, the lottery-like payoff is a bad bet, but there’s a valid reason why homeowners pay for insurance, just as there’s an obvious reason why people play the lottery.

Looking at the trade from the other side, selling insurance is typically a decently profitable business for insurance companies. As policyholders on average lose money with a negative expected value investment, insurance underwriters taking the opposite side of the trade, on average, make money with a positive expected value.

Nonetheless, occasionally disaster strikes, and the insurance policy pays off for the homeowner, causing losses for the insurance company. The reason the business model works is that the vast majority of policies that don’t pay out more than make up for the disasters that happen.

Short Selling as Insurance

Many people caution against the short selling of stocks given the activity theoretically has limited upside with infinite downside. That being said, I’ve seen thousands of public company stocks go to zero while I haven’t yet witnessed one going to infinity. In 2018, 58 public companies filed for bankruptcy, while 71 filed in 2017. In 2008, 138 public companies filed for bankruptcy. When a company is insolvent, its stock tends to become worthless.

The other warning against short selling relies on the fact that the stock market tends to go up over time, historically 8% on average per year.

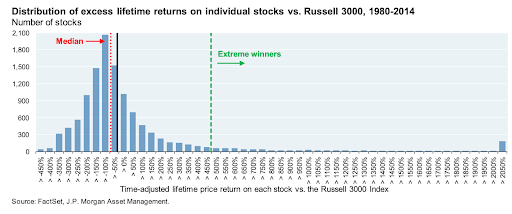

However, on a relative performance basis, the majority of stocks underperform the market. This means that the median stock underperforms the average over its lifetime, leaving substantial opportunities for short sellers.

Short selling of stocks can be seen along the same lines as an underwriter selling insurance. There are a plethora of what we refer to as junk stocks in the market, meaning those with the following attributes contained in our 5-factor model:

- Low quality;

- High valuation;

- Negative price momentum;

- Poor operating momentum; and

- Unfavourable share price trend

Junk stocks are typically high risk and some market participants gamble in these junk stocks given their high volatility and lottery-like payoffs. Unfortunately for these speculators, high-risk and more volatile stocks underperform on average. Given the negative expected values of junk stocks, they offer an insurance-like payoff to those speculators who are long. This means that the vast majority of the time, these junk stocks underperform. However, occasionally an insurance-like payoff comes through when a junk stock hits it big. Unfortunately for the speculators, the occasional big payoff doesn’t make up for the myriad of losers within the junk stock portfolio.

The same dynamics in the insurance market can be seen in the stock market. Homeowners buy insurance policies with negative expected values with a view of a large payoff one day should something bad happen, while the insurance underwriters earn profits from policyholders on average. Speculators buy highly volatile junk stocks with negative expected values with a view of a large payoff one day should something good happen, while the short sellers earn profits from speculators on average on a relative basis.

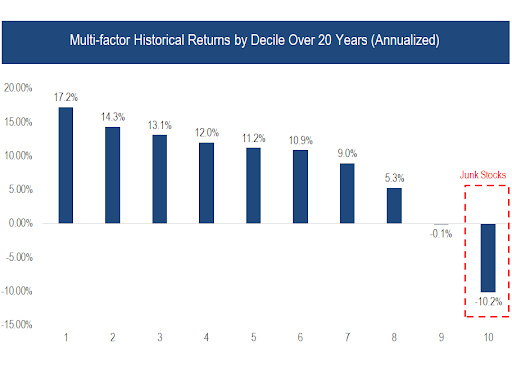

A 20-year simulation was run for approximately 4,000 liquid North American equities. Each month, these equities were segmented into decile portfolios according to the 5-factor model based on quality, value, price momentum, operating momentum and trend.

Source: Accelerate, Compustat, S&P Capital IQ

As seen in the graph above, we find the best and worst performance in the tails — the top and bottom decile multi-factor portfolios. We expect junk stocks, those in the bottom decile, to continue to have poor future share price performance.

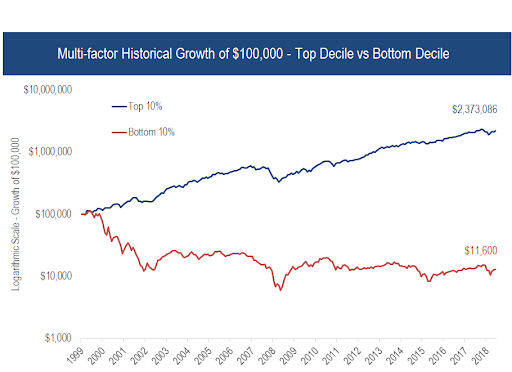

Source: Accelerate, Compustat, S&P Capital IQ

Over the past 20 years, a portfolio of bottom-ranked junk stocks based on quality, value, price momentum, operating momentum and trend would have lost nearly -90%. A portfolio of top-ranked stocks based on the 5 factors would have grown from $100,000 to over $2 million.

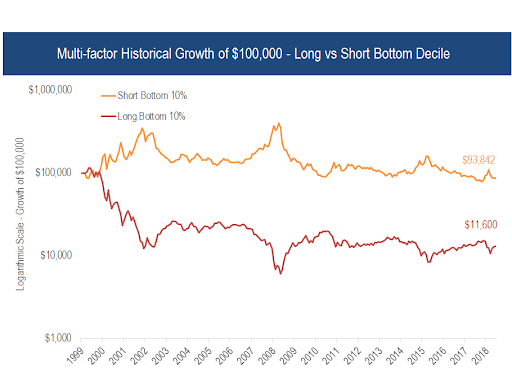

Source: Accelerate, Compustat, S&P Capital IQ

However, as shown in the graph above, shorting the portfolio of junk stocks is not so easy. A short portfolio of junk stocks, shown in orange in the above graph, does not provide the exact opposite return profile of going long, given aspects such as compounding and rebalancing. The long portfolio of junk stocks returned -9.5% annualized, while the short portfolio of junk stocks lost less than -0.5% per year. If interest income from cash generated by the short portfolio were to be included, the net result would be a positive return for the short junk stock portfolio.

Nonetheless, running this short portfolio of junk stocks provides an insurance like-benefit when running in parallel with a long portfolio of top-decile stocks. Namely, the main benefits of including the short junk stock portfolio in the strategy includes:

- Mitigated volatility given the short junk stock portfolio generally provides positive returns during times of market stress when the long portfolio may be declining in value; and

- Increased potential to leverage the long top-decile portfolio to generate further outperformance without increasing market exposure.

The Long and Short of it

Given that the market tends to go up roughly 8% per year on average over the long-term, short-selling on its own is a tough slog because you’re swimming against the tide.

In my opinion, the best way to implement a long-short multi-factor strategy is to run a partial short book of junk stocks, say 50% of net asset value, and using some of that exposure to slightly leverage the long portfolio of top-ranked stocks, say 110% long. This results in leveraged exposure to the stocks offering the highest future returns while mitigating market risk in addition to generating further outperformance through the expected underperformance of junk stocks.

Short Selling in 2019

2019 has been a banner year for long-only investors. The S&P 500, Dow Jones and Nasdaq are currently hitting all-time highs, with all three on track to gain more than 20% this year.

Given these dynamics, it is a difficult environment for a short seller. A highly accommodative Federal Reserve, who is doling out rate cuts in addition to $60 billion per month of quantitative easing, has caused many speculative securities and junk stocks to flourish. 2019 is shaping up to have the largest amount of unprofitable initial public offerings on record.

In the face of these challenges, we have had some great shorts this year. Several junk stocks in which we were short, including CannTrust Holdings and McDermott International, dropped more than -80%, buoying our short portfolio.

Unfortunately, occasionally that one lottery ticket-like junk stock pays off hugely for speculators, and short sellers take a big hit. In our case, that stock was ChemoCentryx. This stock ranked poorly on all of our predictive metrics — low quality with a high valuation, negative price momentum, poor operating momentum and an unfavourable share price trend. Regardless, none of these metrics mattered when ChemoCentryx announced positive phase 3 trial results and its stock rallied 280% instantly.

Yes, I was short a stock that nearly quadrupled overnight. Now I know how Ben Askren felt when he got KO’d in 5 seconds by Jorge Masvidal at UFC 239.

That one hurt.

The Case for Short Selling Within a Portfolio

Despite the occasional face-ripping rally or painful short squeeze, both of which have happened this year, short selling still holds a valid place in a diversified portfolio. Good long term performance can be had from a short portfolio of junk stocks despite the occasional setbacks.

This is not an argument for negative net exposure to stocks. Short selling should only be used within the context of a larger long portfolio.

Just as underwriters hope to at least break even on their insurance underwriting, hedge funds hope to break even on their shorts, or at least short securities that are underperforming their longs, with the goal of generating alpha irrespective of market direction.

Even if it doesn’t generate positive returns over the long term, short selling serves two main purposes within a portfolio:

- It reduces portfolio volatility by providing a hedge, or a portion of a portfolio that will outperform when the market is declining. This leads to lower volatility and mitigated downside risk

- It allows hedge funds to leverage their longs with the goal of adding outperformance through increased exposure to their best ideas without a commensurate increase in market exposure.

The other benefit of short selling is that it generates cash from the proceeds of the sales, which can be used to generate interest income. If the interest rate on cash is higher than the average borrow cost of a short portfolio, then this produces a positive return stream and a tail-wind for hedge funds.

Just how the insurance market functions properly, with underwriters earning profits on average over time despite the occasional costly disaster claim, short selling has merit with a diversified portfolio and is expected to add value over time despite the occasional painful hit from the short book.

-Julian