May 1, 2026 – The world of finance is littered with three letter acronyms.

To add to the plethora of those regularly discussed in this memo (to be fair, it is about M&A and SPACs), CVR is one that should be in investors’ lexicons.

We previously provided a primer on Contingent Value Rights (CVRs) in our November 2025 memo, CVRs: Unlocking Hidden Upside in M&A Deals. We wrote:

A Contingent Value Right (CVR) is a contractual instrument often issued in connection with mergers and acquisitions (M&A) that gives the target company’s shareholders the right to receive additional future payments if certain specified events or milestones are achieved after the deal closes. It is used to bridge the bid-ask price gap, in which the acquiror may not be willing to pay full value upfront due to uncertainty regarding the ultimate value of an asset, such as the result of a clinical trial, lawsuit, or business milestone.

A CVR ties part of the purchase price, typically a small portion of the total deal consideration, to the future performance of that uncertain factor. It is a contractual right that is issued to the target company shareholders upon consummation of a merger, in addition to the cash or stock consideration. Typically, CVRs are non-transferable, meaning they are not listed as exchange-traded securities. Therefore, once an M&A deal featuring a CVR closes, the target shareholder is left holding an illiquid, lottery-like ticket.

Basically, a CVR is a security issued as part of the consideration in an M&A deal that enables a holder to receive more money months or years later if the upside materializes.

It is worthwhile revisiting the concept as the use of CVRs in mergers and acquisitions has continued to surge. Furthermore, not only is the issuance of CVRs used in deals increasing, but their use across sectors is widening. Historically, CVRs were utilized as a way to bridge the value gap in biotech transactions by reflecting the future potential of an unapproved drug in the deal target’s pipeline. Nowadays, while use of the structure remains popular in biotech transactions, it has expanded into other sectors, including mining and technology. Not to mention transcending borders – nearly half of Canadian public M&A deals last month featured a CVR.

In April, seven public M&A transactions were announced in Canada. While the big kuhana, Shell’s $22.0 billion acquisition of ARC Resources (the largest Canadian oil patch deal on record) did not feature a CVR, four others did:

- G Mining Ventures’ $3.0 billion merger with G2 Goldfields features a CVR worth up to $200 million, depending on future potential gold reserves on the acquired properties.

- Agnico Eagle Mines’ $2.9 billion acquisition of Rupert Resources includes a CVR potentially worth more than $700 million, again based on future potential mineral reserves.

- Francisco Partners’ $765.1 million buyout of Blackline Safety comes with a CVR worth up to $44 million, depending on future annualized recurring revenue (saving you here from another 3-letter acronym, ARR).

The American merger market continued the same trend of lofty CVR issuance. In April, of the fourteen public M&A deals announced in the U.S., two included CVRs in their structures. Ligand Pharmaceuticals’ $739.0 million merger with XOMA Royalty and Garda Therapeutics’ $125 million acquisition of Assertio Holdings both featured CVRs of undetermined potential value.

Including the three transactions that used CVRs announced in March, 8% of announced but not yet closed North American public mergers include a Contingent Value Right in the consideration offered to target shareholders.

While it is essential that investors are aware of CVRs and how they work given their increasing popularity, valuing them is another story. Ascribing a valuation to the typical merger consideration, either cash or shares, is simple. However, CVRs and their lottery-like payoff are highly speculative and valuing them can be more art than science.

To cut to the chase – Accelerate maintains a database of all CVRs issued since 2013. Of the 84 issued over that time, we have payout data on 26, which have, on average, distributed 52 cents on the dollar (within a wide range of 0% to 100%, of course) to CVR holders. As expected, the market typically values CVRs well below the 52% average payout (before accounting for the time value of money).

As CVRs become an increasingly common feature of merger considerations, investors who can properly assess their structure, risks, and potential payoff will be better positioned to recognize value where the market may see only uncertainty.

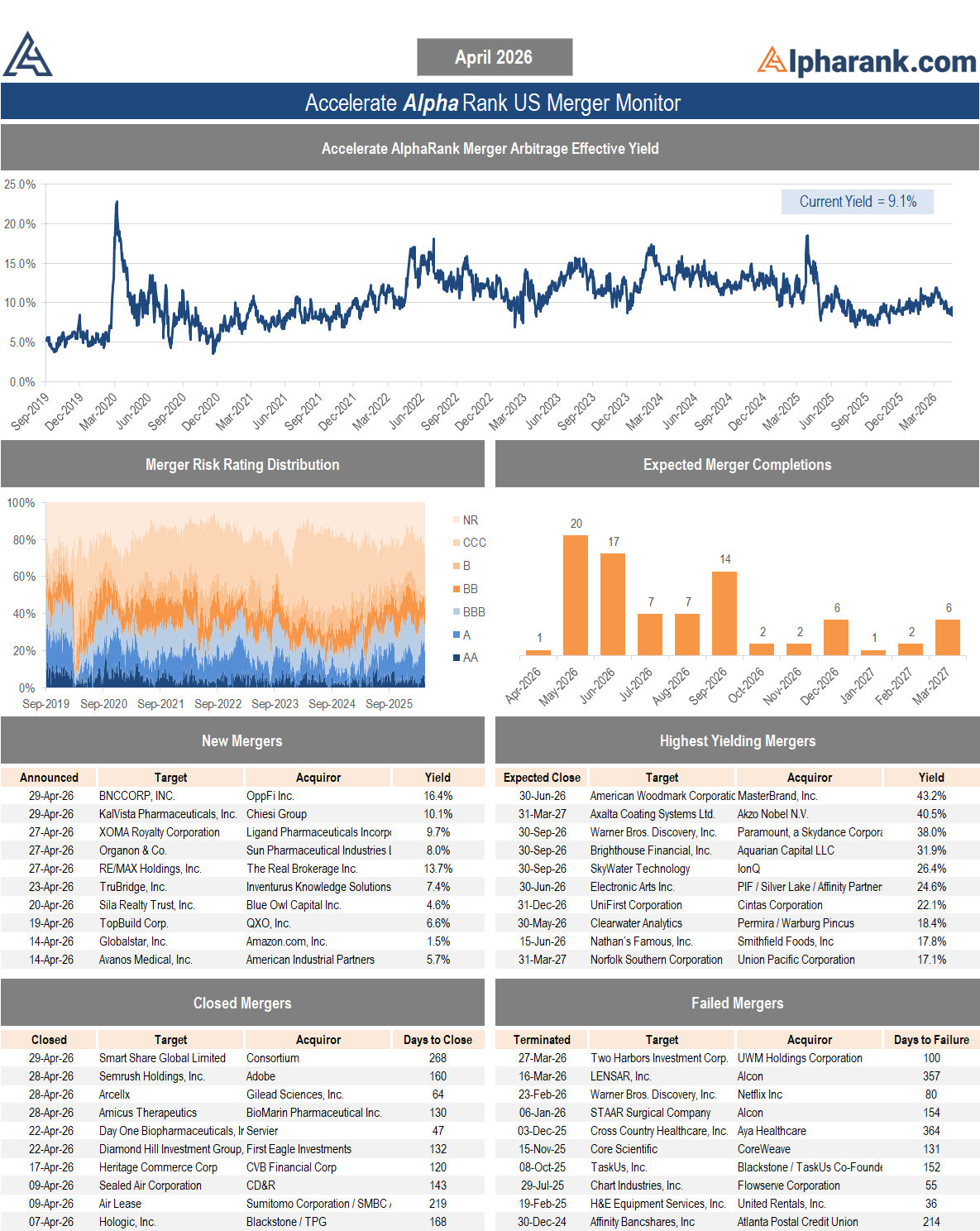

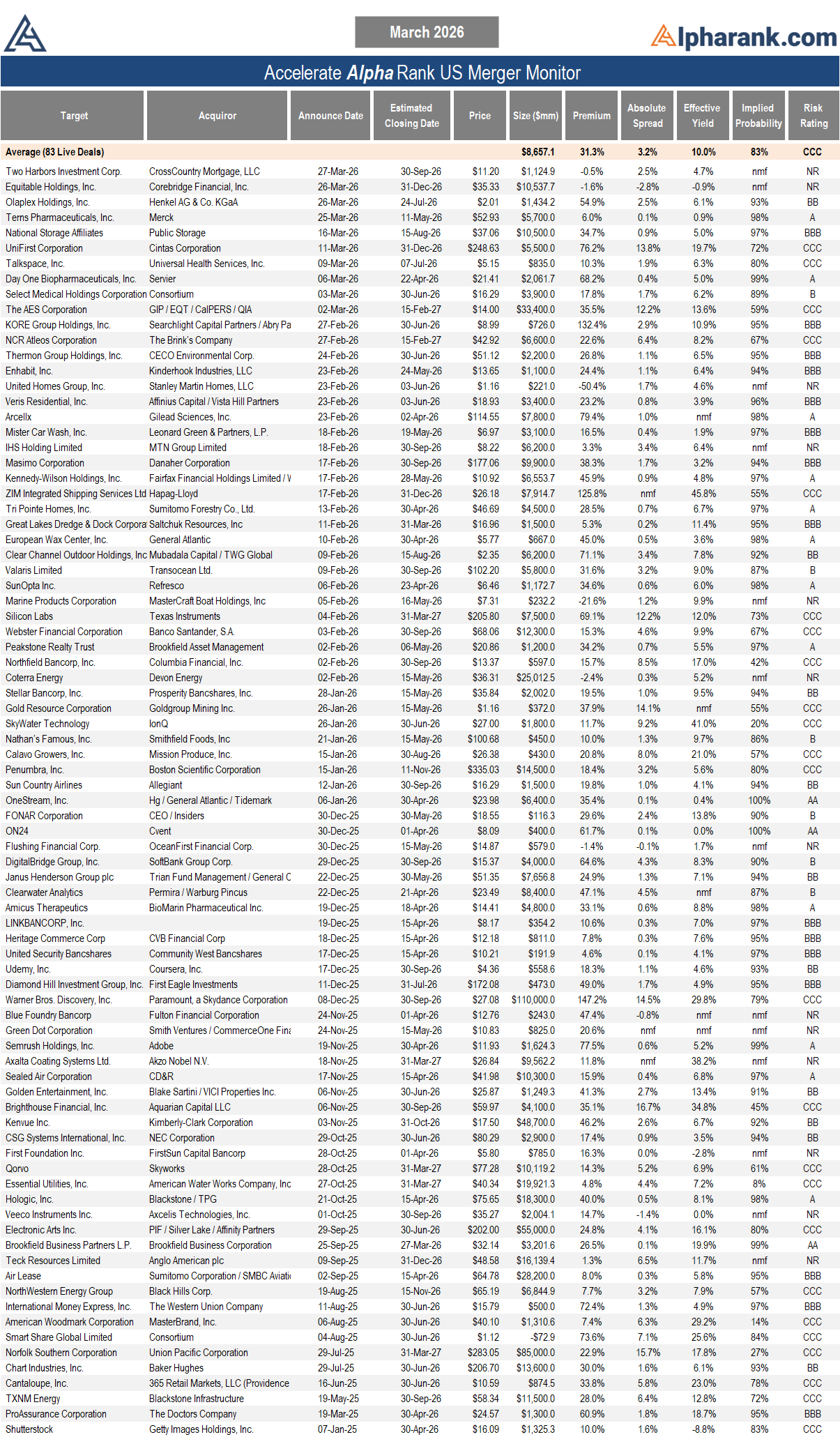

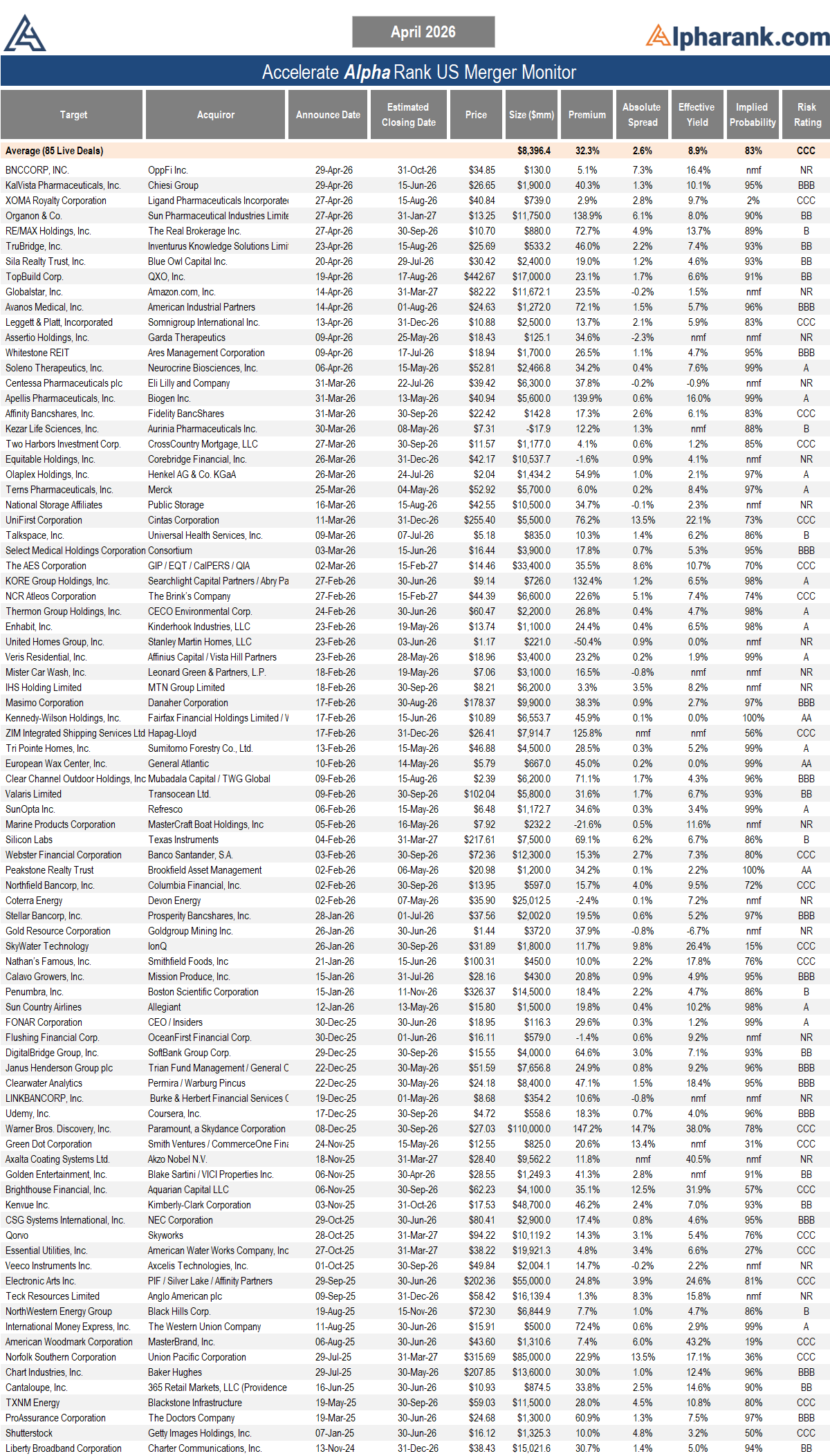

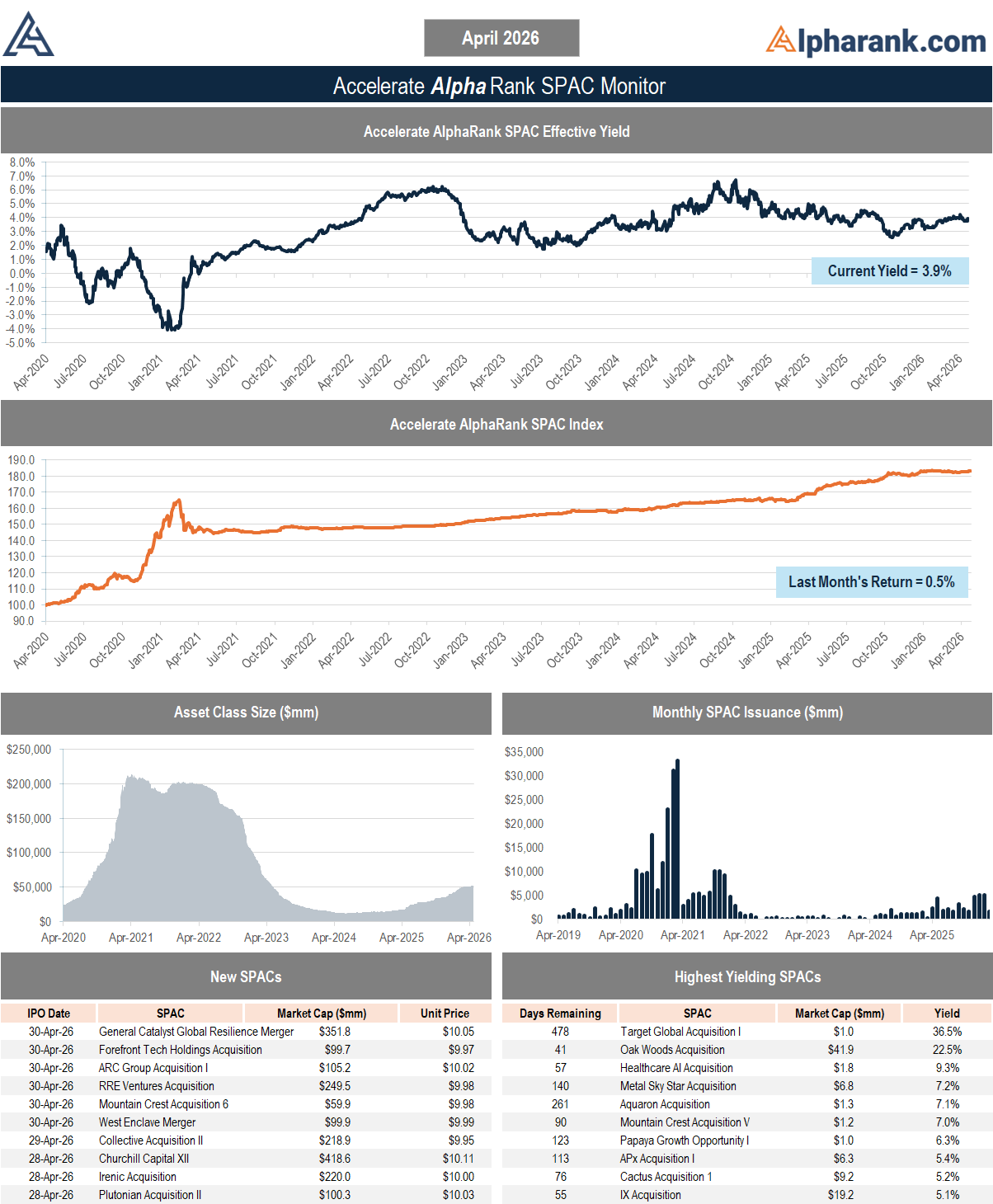

The AlphaRank.com Merger Monitor below represents Accelerate’s proprietary analytics database on all announced liquid U.S. mergers. The AlphaRank Merger Arbitrage Effective Yield represents the average annualized returns of all outstanding merger arbitrage spreads and is typically viewed as an alternative to fixed income yield.

Each individual merger is assigned a risk rating:

- AA – a merger arbitrage rated ‘AA’ has the highest rating assigned by AlphaRank. The merger has the highest probability of closing.

- A – a merger arbitrage rated ‘A’ differs from the highest-rated mergers only by a small degree. The merger has a very high probability of closing.

- BBB – a merger arbitrage rated ‘BBB’ is of investment grade and has a high probability of closing.

- BB – a merger arbitrage rated ‘BB’ is somewhat speculative in nature and has a greater than 90% probability of closing.

- B – a merger arbitrage rated ‘B’ is speculative in nature and has a greater than 85% probability of closing.

- CCC – a merger arbitrage rated ‘CCC’ is very speculative in nature. The merger is subject to certain conditions that may not be satisfied.

- NR – a merger-rated NR is trading either at a premium to the implied consideration or a discount to the unaffected price.

The AlphaRank merger analytics database is utilized in running the Accelerate Arbitrage Fund (TSX: ARB), which may have positions in some of the securities mentioned.

* AlphaRank is exclusively produced by Accelerate Financial Technologies Inc. (“Accelerate”). Visit Alpharank.com for more information. Disclaimer: This research does not constitute investment, legal or tax advice. Data provided in this research should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this research is based on current market conditions and may fluctuate and change in the future. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Accelerate may have positions in securities mentioned. Past performance is not indicative of future results.