December 12, 2019—The Canadian multi-factor portfolio eked out positive 1.6% net alpha in the month of November with the value and quality portfolios leading the way.

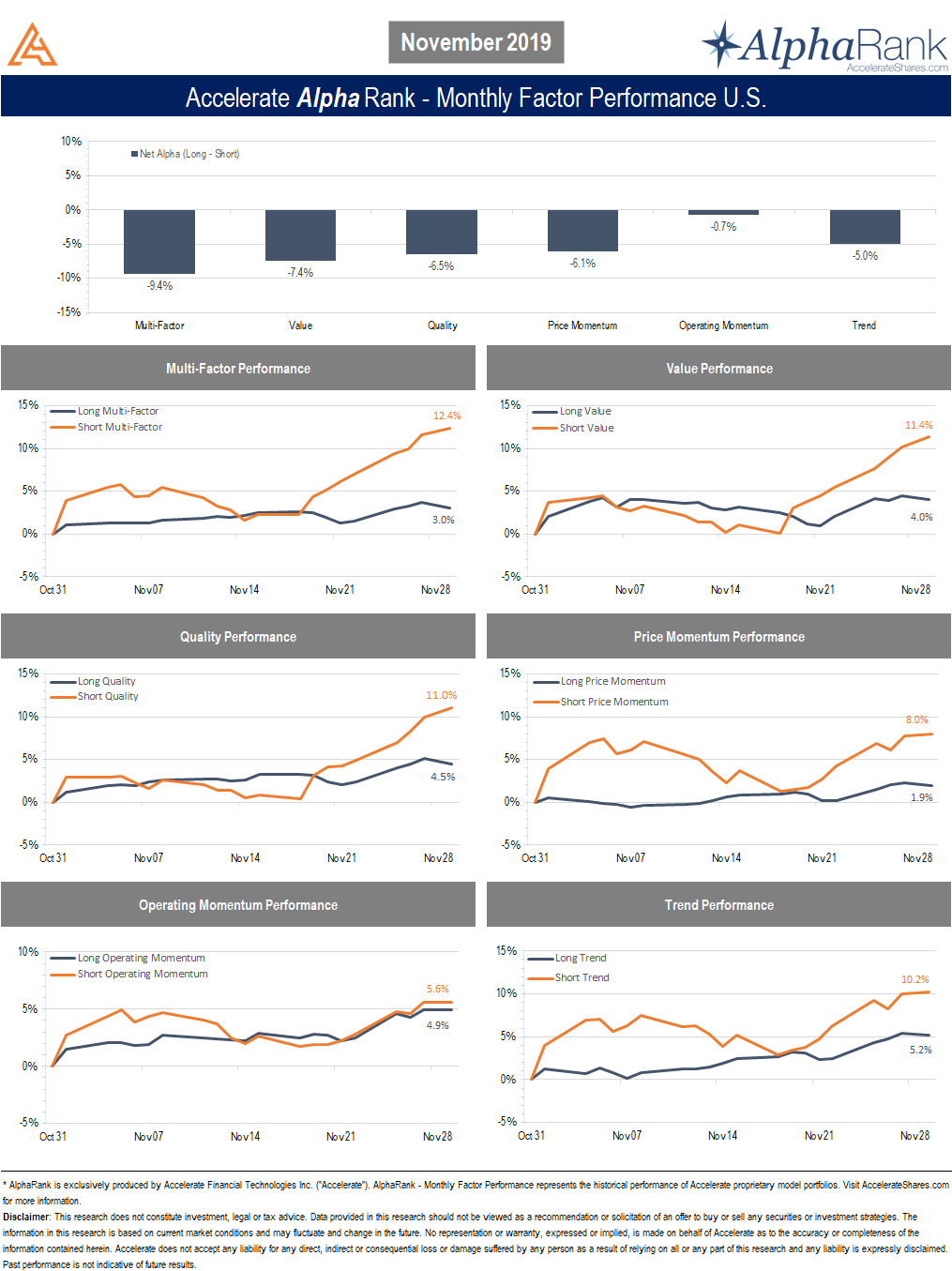

The U.S. multi-factor portfolio dropped -9.4% in November, a rough month for factor investing in the U.S. as all long-short factors posted negative performance. The dreary results were driven exclusively by the short portfolios, which experienced substantial rallies.

AlphaRank Factor Performance represents the daily historical performance of Accelerate’s proprietary model factor portfolios for the previous month.