March 10, 2020 – Mid-February marked the commencement of the coronavirus-induced market panic. A global sell-off in equities occurred as market participants began pricing in a global recession based on the rapid spread of COVID-19.

In February, the Canadian multi-factor long-short portfolio continued to outperform, adding 9.1% of alpha. The multi-factor long book was not immune from the sell-off, falling -6.3%, however the short book more than offset this decline as it fell -15.4%. Similar to January, price momentum was the top performing factor as top performing stocks held up during the market decline, falling only -1.0%, while the stocks with poor price momentum (i.e. the short price momentum portfolio) fell -18.7%. Trend, operating momentum and quality factors also added outperformance during the month, while the value factor was the lone detractor for the Canadian multi-factor portfolio.

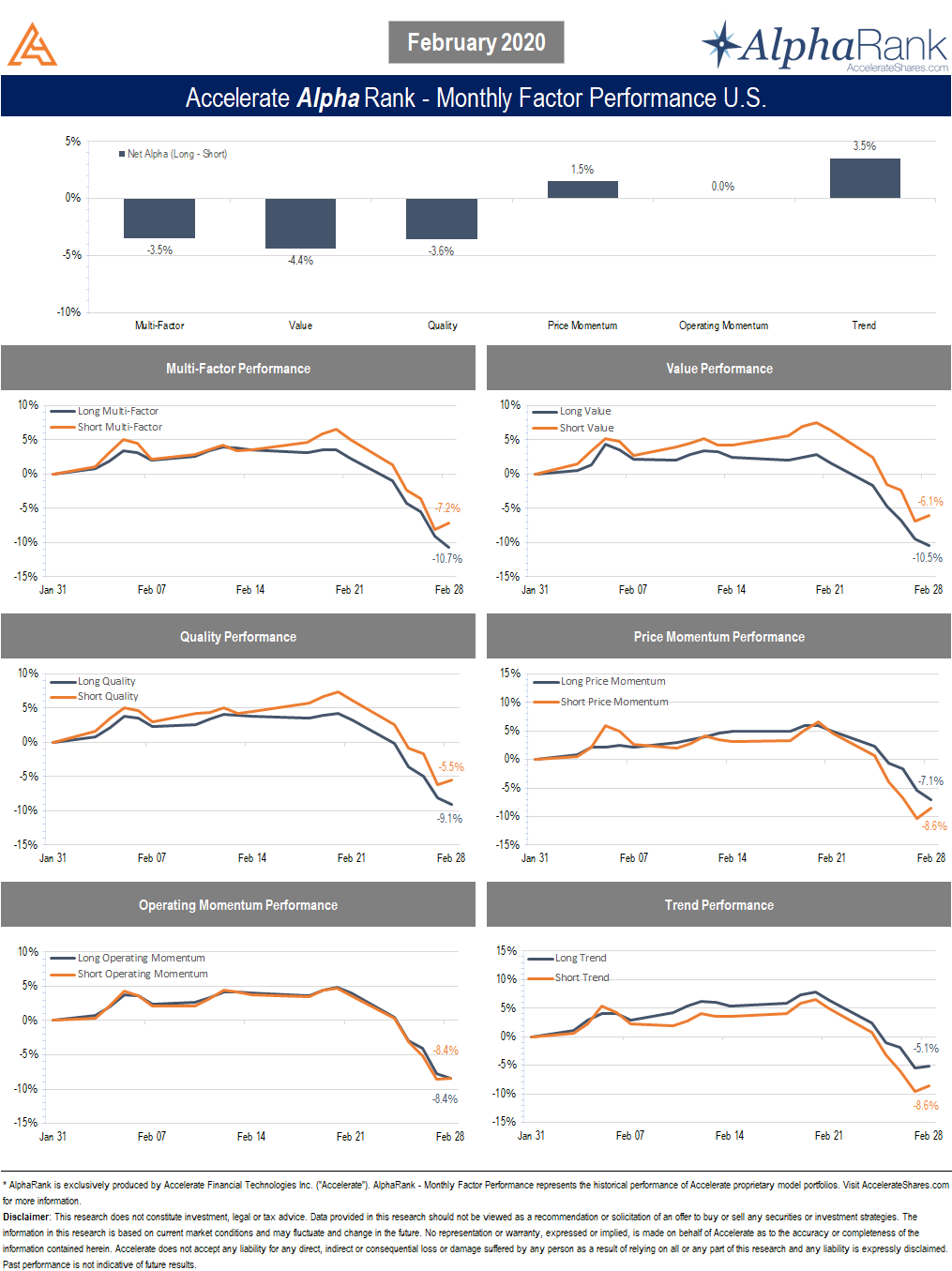

The U.S. multi-factor long-short portfolio underperformed in February, with the long portfolio dropping -10.7% and the short portfolio falling -7.2%, leading to a decline of -3.5% for the long-short portfolio. The price momentum and trend factors contributed positively, but were more than offset by the value and quality factors, which dropped -4.4% and -3.6% during the month respectively.

AlphaRank Factor Performance represents the daily historical performance of Accelerate’s proprietary model factor portfolios.