![]()

March 12, 2019 – Growing up on the Canadian prairies, like most kids, I played hockey. I was a left-winger and had a penchant for scoring goals (what kid doesn’t?). For what I lacked in size and skill, I tried to make up in cherry-picking ability. I figured I could maximize the expected amount of goals I’d score if I only played offense aggressively, and never back-checked or played defensive hockey.

While this strategy helped my team put up goals, it certainly did not help prevent goals against. Thankfully, my line was stocked with talented defensemen who made up for my lack of defensive skills.

Like any competitive endeavour, the best strategies to win typically combine a balanced approach of both offensive and defensive play. Investing is no different.

Scoring with Factors

Factor investing, commonly known as “smart beta”, is a rules-based style of investing in which portfolio securities are selected based on certain characteristics associated with higher returns.

These characteristics, known as factors, are persistent drivers of risk and return that can be systematically utilized to select securities to create portfolios that may outperform.

The Momentum Factor

For example, the momentum factor, applied to equity investing, involves buying winning stocks and shorting losing stocks. One implementation of the momentum factor is the 52-week high anomaly. This momentum strategy, detailed in George and Hwang’s 2004 paper entitled “The 52-Week High and Momentum Investing”, involves going long stocks near their 52-week high while going short stocks far from their 52-week high.

Stocks near their 52-week highs outperform and stocks near their 52-week low underperform. In a nutshell, good stocks tend to continue to do well and bad stocks tend to continue to do poorly.

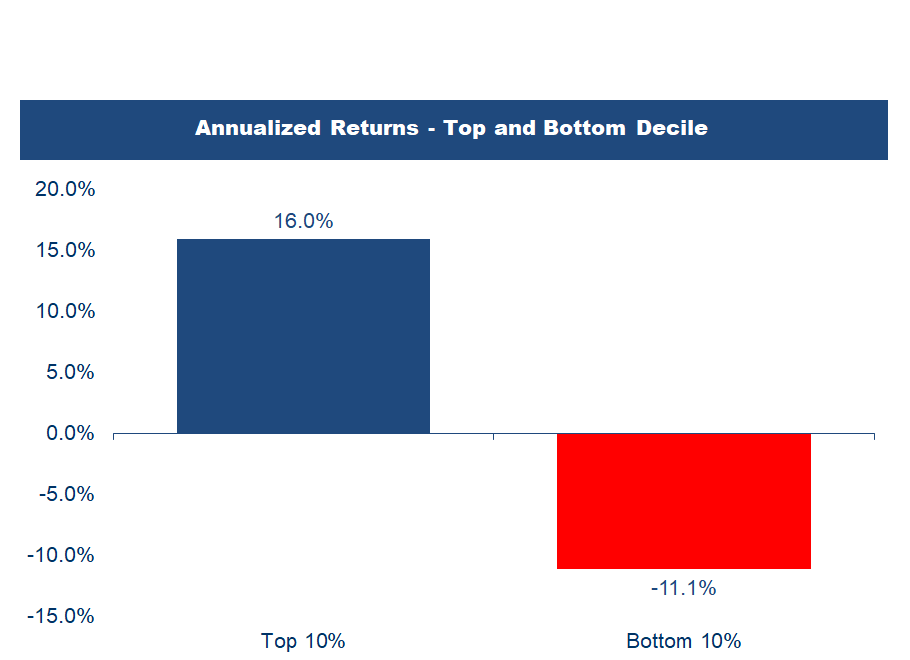

Running the 52-week high strategy on Canadian stocks over the past twenty years yields the following results:

Source: ClariFI S&P Capital IQ

Disclaimer: Past performance is not indicative of future results

The top decile portfolio returned 16.0% per year, while the bottom decile portfolio returned -11.1% per year.

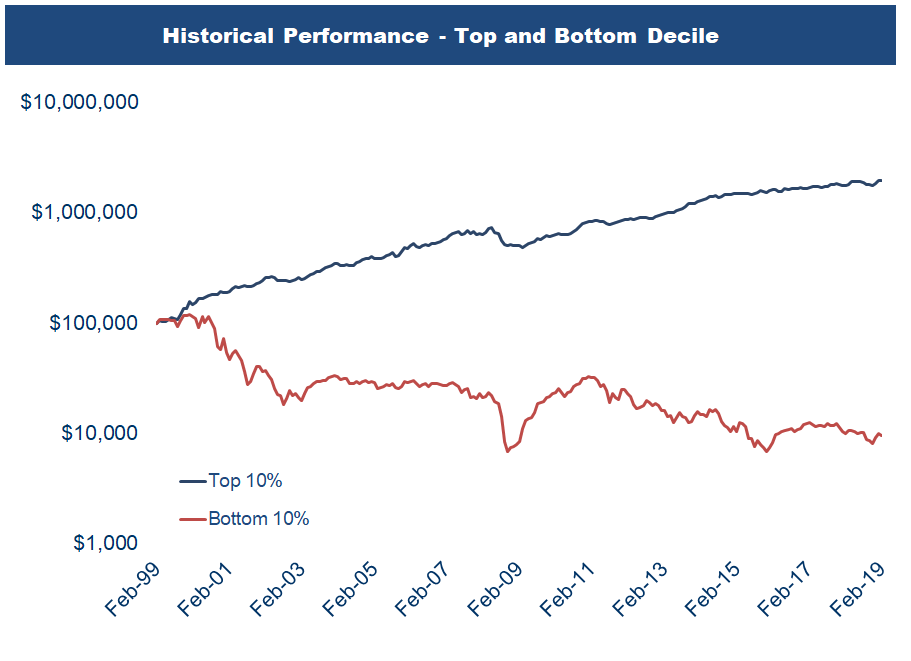

A $100,000 investment into the top decile portfolio, rebalanced on a monthly basis, results in a portfolio worth approximately $2 million after 20 years.

A $100,000 investment into the bottom decile portfolio, rebalanced on a monthly basis, results in a portfolio worth approximately $10,000 after 20 years (a -90% loss).

As you can see, the top decile portfolio massively outperforms while the bottom 10% portfolio significantly underperforms.

Source: ClariFI S&P Capital IQ

Disclaimer: Past performance is not indicative of future results

An enterprising investor can harvest the underperforming bottom decile portfolio by shorting it. This allows the investor not only to gain from the short portfolio, but also hedge out the market risk associated with the long portfolio and earn returns on a hedged basis.

Factor Investing: Hockey Stick Growth

Factor-based investment strategies can be readily programmed and implemented within an ETF. Factor strategies effectively quantify what many human portfolio management teams do, but use inexpensive computing power instead of teams of analysts and portfolio managers. Because of this, factor strategies can be implemented cost-effectively.

Aside from the cost savings, historically, factor strategies have outperformed traditional actively managed mutual funds.

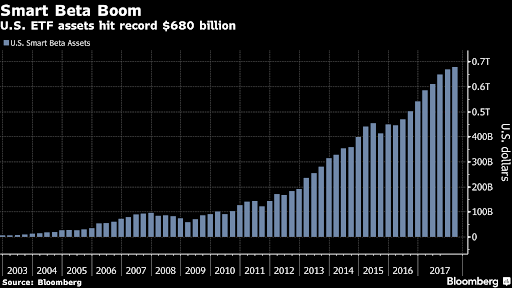

Given the potential cost savings and outperformance of factor strategies, it’s no wonder asset growth has been robust. U.S. smart beta ETF strategies are expected to exceed $1 trillion in assets by 2020.

Smart Beta: A Half-Assed Implementation

Although used synonymously, smart beta, as implemented through ETFs, is not actually factor investing. True factor investing involves both going long the top quantile securities within that factor, while also going short the bottom quantile securities within said factor. This is done to produce true alpha, or outperformance. A robust factor should show the top quantile outperforming the mean, along with the bottom quantile underperforming the mean.

Smart beta ETFs are literally implementing factor strategies half-assed. They are implementing the long top quantile portion of the strategy, but leaving out the short bottom quantile and missing half the strategy, which misses half of the potential outperformance. They are all offense and no defense. The short portfolio tends to show strong gains when the market declines, which can help cushion losses from the long portion of the portfolio.

The Long and Short of It

Academic research, which is where factor strategies are derived from, demonstrates that factor strategies have the best performance when executed using a long-short approach.

Much like a hockey team with a good combination of offense and defense, factor strategies have the best chance of outperforming throughout various market environments with a balanced combination of both long and short portfolios.

Don’t be a cherry-picker. Play some defense.