![]()

July 9, 2019 – They say that May showers bring June flowers and with value’s underperformance in May, investors were hoping that June would bring a subsequent turnaround in value performance.

Unfortunately for value investors, that was not the case as value suffered another month of poor performance.

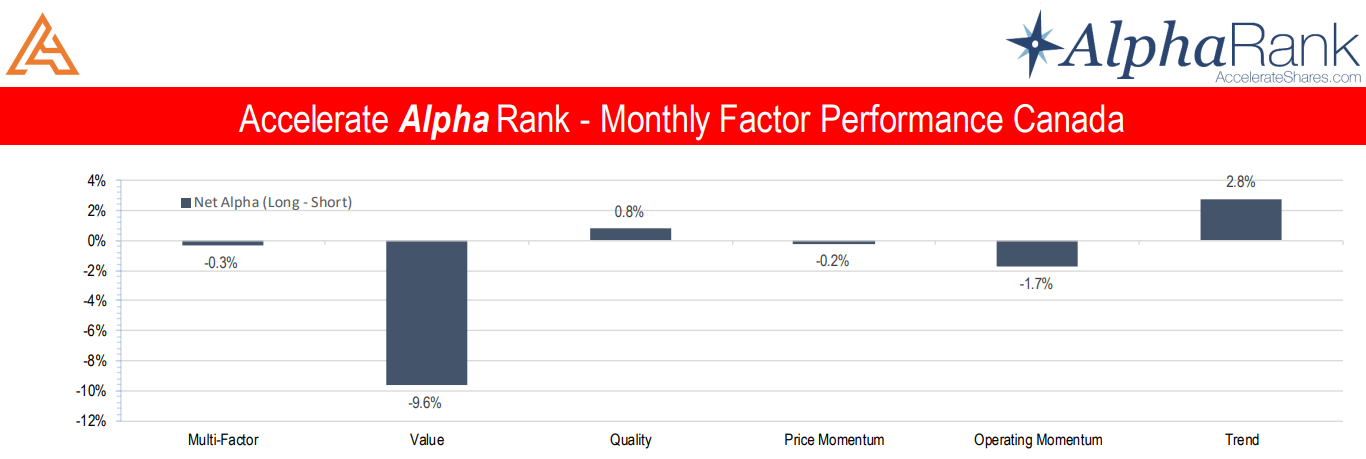

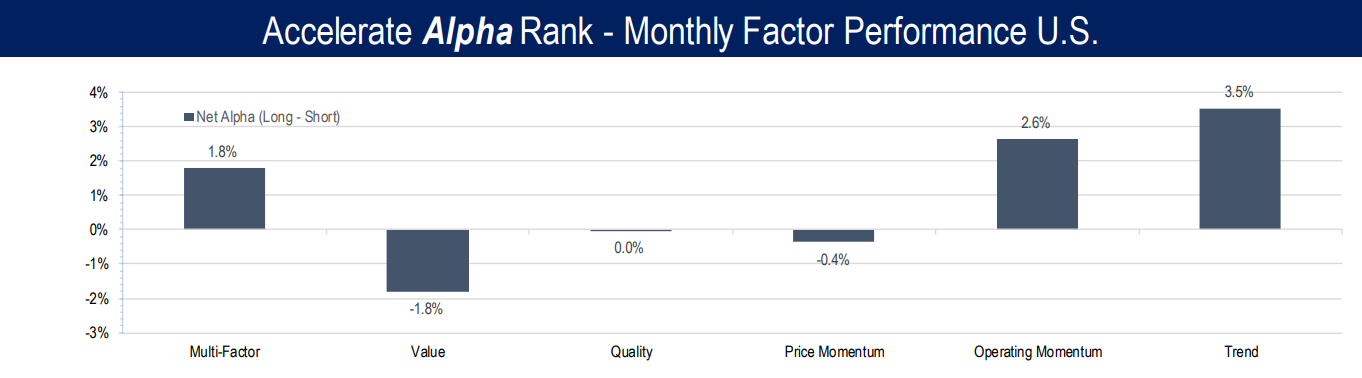

Despite the underperformance of value, Accelerate’s multi-factor market neutral portfolio did manage to generate alpha in the month of June, booking +1.8% of long-short outperformance in the U.S. offset by -0.3% underperformance in Canada.

As markets rallied back in June, including a 7% total return for the S&P 500 and a 2.5% total return for the S&P/TSX Composite, the multi-factor portfolio generated alpha from the long side.

As markets rallied back in June, including a 7% total return for the S&P 500 and a 2.5% total return for the S&P/TSX Composite, the multi-factor portfolio generated alpha from the long side.

The Canadian multi-factor long-short portfolio generated a -0.3% return in June, driven by a 5.9% return from the long multi-factor portfolio, offset by a 6.2% return from the short multi-factor portfolio.

The U.S. long multi-factor portfolio returned 7.4% while the short portfolio returned 5.6% for net multi-factor alpha of 1.8%.

The outperformance generated by the multi-factor portfolios was driven by the trend factor and to a lesser extent the operating momentum factor.

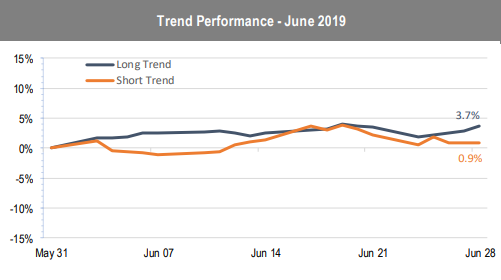

In Canada, the long trend portfolio generated a 3.7% gain while the short trend portfolio returned 0.9%, resulting in net alpha of 2.8%.

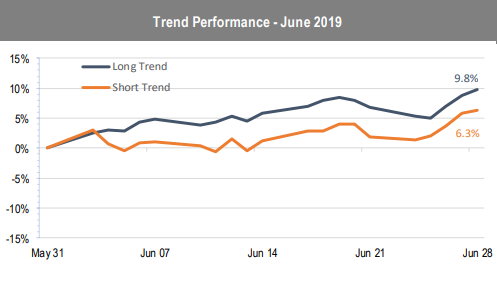

Trend in the U.S. was the best performing long-short factor in June. The 3.5% alpha generated in the trend factor was driven by a 9.8% gain from the long trend portfolio, offset by a 6.3% return in the short trend portfolio.

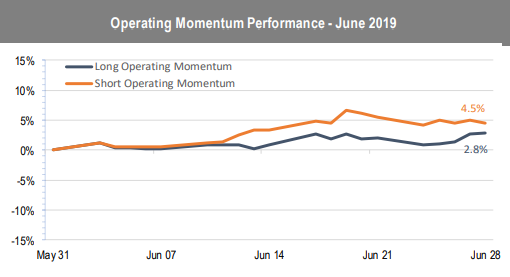

Operating momentum in Canada underperformed with a net -1.7% loss in June. The long operating momentum portfolio gained 2.8%, underperforming the short operating momentum portfolio’s return of 4.5%.

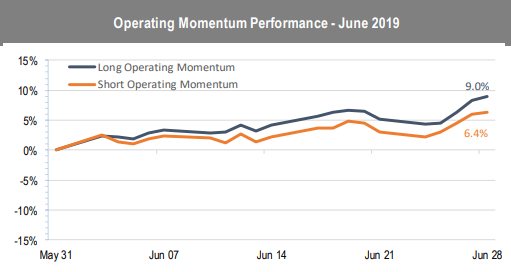

In the U.S, the long operating momentum portfolio gained 9.0% while the short operating momentum portfolio returned 6.4%, resulting in net alpha of 2.6%.

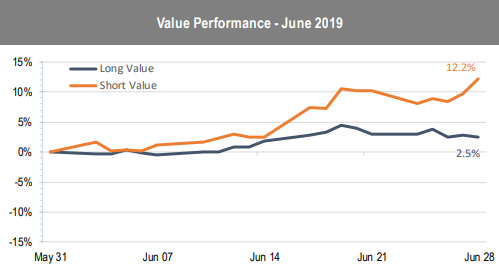

The long-short Canadian value portfolio suffered dearly in June, with the short portfolio ripping a stunning 12.2%. The short value portfolio, or the top 10% of the most highly-valued Canadian stocks, went up the most, which is the opposite of what is it expected. To add insult to injury, the long value portfolio, or a basket of the cheapest 10% of stocks, advanced only 2.5%. This divergence led to a -9.6% loss for the Canadian long-short value portfolio.

The long-short Canadian value portfolio suffered dearly in June, with the short portfolio ripping a stunning 12.2%. The short value portfolio, or the top 10% of the most highly-valued Canadian stocks, went up the most, which is the opposite of what is it expected. To add insult to injury, the long value portfolio, or a basket of the cheapest 10% of stocks, advanced only 2.5%. This divergence led to a -9.6% loss for the Canadian long-short value portfolio.

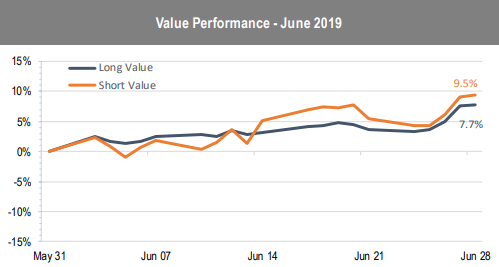

While value in the U.S. wasn’t nearly as bad as Canada, it still underperformed with a -1.8% loss driven by a 7.7% gain for the long U.S. value portfolio which was more than offset by a 9.5% return in the short value portfolio.

For the month of June, both long-short quality and price momentum portfolios were basically flat as their underlying long and short portfolios roughly matched the market return.

May showers did, in fact, bring June flowers for long-only investors as market indices bounced back, but Accelerate’s long-short multi-factor portfolio still managed to generate outperformance, driven by trend and operating momentum in the U.S. and trend in Canada.

Download the AlphaRank Factor Performance– June 2019 here.