July 13, 2026 – When conflict in the Middle East broke out in the spring, equities plummeted, and the volatility (VIX) index leapt above 30 – a level denoting significant market stress.

Since then, as geopolitical strife has diminished somewhat, equity market volatility and stress have entered a summer lull.

Currently, with the VIX at 15, below its long-term average of 17 to 18, and the Fear & Greed Index at 49, firmly in the “neutral” camp, stress indicators are signalling an unusually calm market.

Source: CNN

That said, investor complacency may not be as widespread as the muted market stress indicators suggest. Despite the market’s apparent calm, considerable turbulence is building beneath the surface. Sector rotation and a debate around market leadership are brewing in an age-old battle between bulls and bears.

Allocators are leaving breadcrumbs signalling the occurrence of a “great rotation” in the equity market, with investors recently moving from artificial intelligence winners to other segments of the equity market, suggesting that the easiest returns from the initial AI infrastructure buildout may have already been captured, and that the burden of proof is shifting from AI spending growth to economic returns.

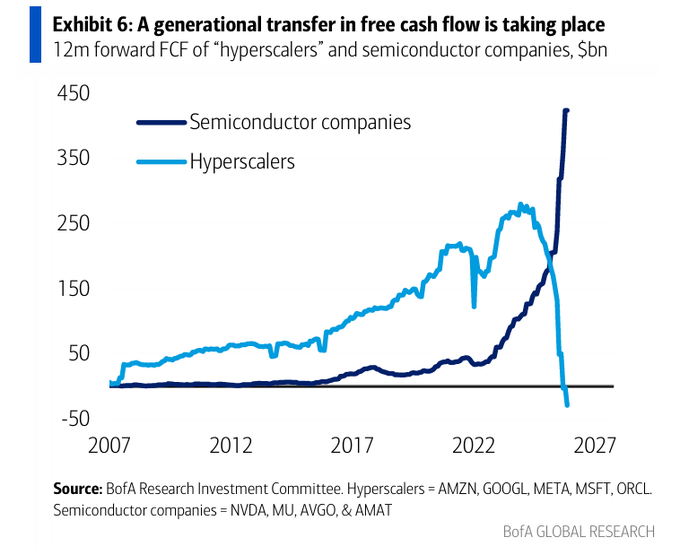

Over the past year, the “AI bottleneck” trade has led the stock market higher. The beneficiaries of seemingly endless spending on AI infrastructure, in particular semiconductor manufacturers, have seen their profits surge, and their stock prices have followed. This relentless data center spending, primarily headed by the so-called hyperscalers, has led to an unprecedented wealth transfer to semiconductor companies at the forefront of AI (memory and compute).

In our early candidate for chart of the year, BofA Research compared the annual free cash flow of the hyperscalers (Amazon, Alphabet, Meta, Microsoft, and Oracle) with that of the leading semiconductor companies (Nvidia, Micron, Broadcom, Applied Materials). As the free cash flow of the hyperscalers has plummeted due to skyrocketing capital expenditures on AI data centers, semiconductor companies’ free cash flow has surged.

One man’s capex is another man’s profit (although the accounting of this dynamic can lead to elevated index-level profitability, as capital equipment is depreciated over several years while the counterbalancing profit is booked up front).

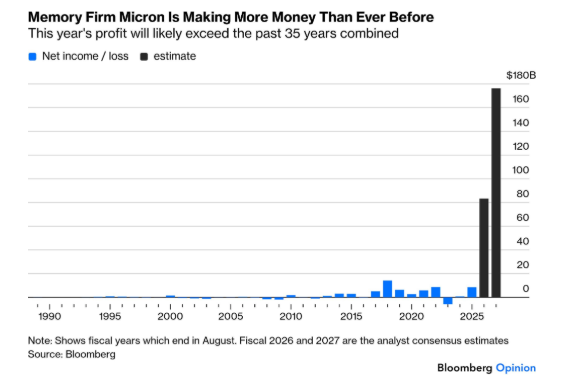

The poster child beneficiary of the capex extravaganza is Micron, an American manufacturer of computer memory and data storage products. Recently, memory has become the scarce bottleneck in AI systems. As AI workloads are becoming more memory-intensive with a focus on inference, demand for high-bandwidth memory has surged. This rapidly rising demand has been met with constrained supply, due to the oligopolistic nature of the memory business and long lead times for building additional capacity. Only a few companies can manufacture leading-edge HBM at scale: principally SK hynix, Samsung, and Micron.

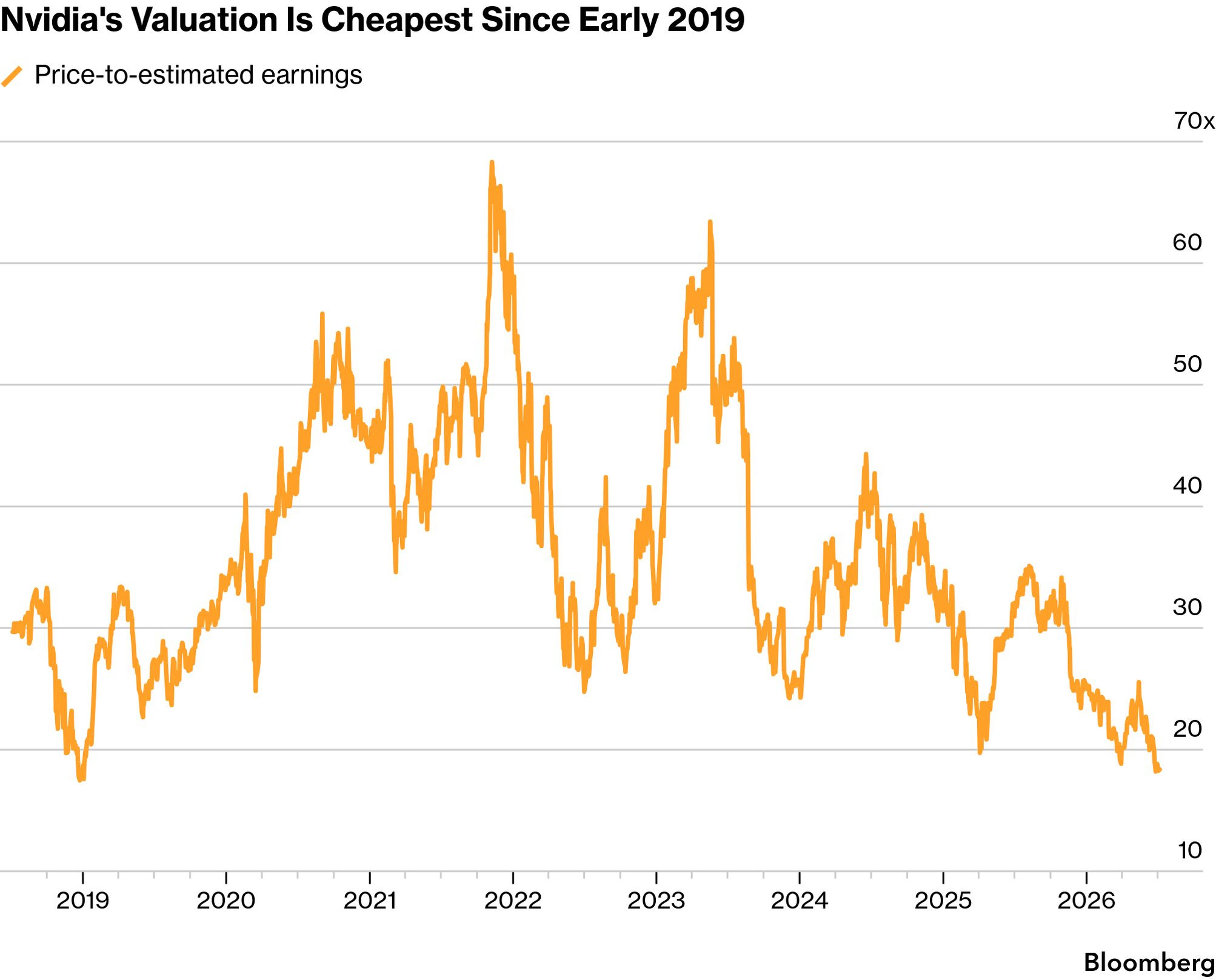

Nevertheless, after seeing their stock prices surge over the past year (memory companies) to several years (compute companies), recent underperformance has emerged as investors worry about the sustainability of AI infrastructure spending and the resulting potential cyclical peak profitability of the semiconductor sector. With relative stock weakness accompanying a potential shift in market leadership, combined with still surging profits, semiconductor valuation multiples have contracted meaningfully. Micron and SK hynix both trade at below 7x next year’s forecast earnings. Nvidia trades around 18x earnings, the first time it has traded at a below-market multiple since 2019 – years before ChatGPT was first released.

While the equity market remains unusually calm above the surface, a fight for market leadership is brewing below. If bullish AI spending forecasts come to fruition, with some expecting data center capex to continue to grow through 2030, semiconductor stocks could regain their market leadership. If the hyperscalers show any sign of easing off the gas pedal on AI-related capital expenditures, expect additional weakness in the AI bottleneck trade, with the result a passing of the leadership baton to unloved segments of the market.

As for now, the battle for market leadership in the Great Rotation continues.

Accelerate manages five alternative investment solutions, each with a specific mandate:

- Accelerate Arbitrage Fund (TSX: ARB): Merger Arbitrage

- Accelerate Absolute Return Fund (TSX: HDGE): Absolute Return

- Accelerate OneChoice Alternative Multi-Asset Fund (TSX: ONEC): Multi-Asset

- Accelerate Canadian Long Short Equity Fund (TSX: ATSX): Long Short Equity

- Accelerate Diversified Credit Income Fund (TSX: INCM): Private Credit

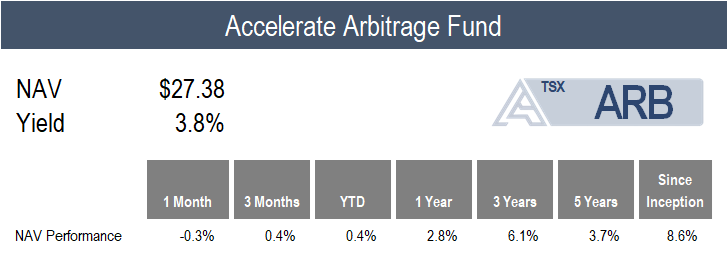

ARB declined -0.3% in June compared to the benchmark S&P Merger Arbitrage Total Return Index’s 0.2% gain.

The Fund added four merger arbitrage investments during the month (two U.S., two Canadian) and participated in thirteen SPAC IPOs.

Currently, ARB is 167.9% long and -3.6% short (171.5% gross exposure), with 70% allocated to SPAC arbitrage and 30% to merger arbitrage (with 11% in LBOs and 19% in strategic M&A).

![]()

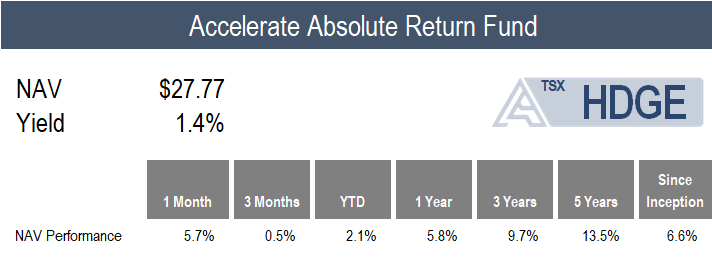

HDGE gained 5.7% in June, buoyed by positive long short factor performance across the board.

After the challenging environment for short selling in May, market neutral factor portfolios bounced back in June, led by the value and quality portfolios. In the U.S. equity market, the long short quality portfolio led the pack with a 10.7% gain, followed by the value portfolio, which generated alpha of 9.5%. All other major factor portfolios were positive for the month.

Top Fund contributors include short positions in Firefly Aerospace and Cleveland-Cliffs, as well as a long position in Lam Research. Top Fund detractors include short positions in Newell Brands and Varonis Systems, along with a long position in Kinross Gold.

![]()

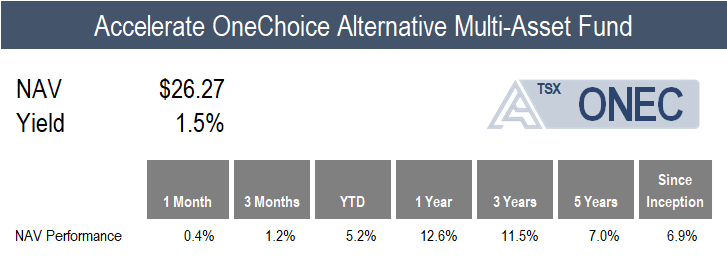

ONEC increased by 0.4% in a mixed month for alternative asset classes.

Positive contributors to the Fund’s return include allocations to absolute return, infrastructure, real estate, and private credit, which gained 5.7%, 4.7%, 2.5%, and 2.3%, respectively.

On the negative side of the ledger, leveraged loans, long short equity, merger arbitrage, and managed futures all declined by less than -1.0%. In addition, the Fund’s allocations to risk parity, commodities, and gold all fell, with monthly performance of -1.8%, -3.4%, and -11.5%, respectively.

![]()

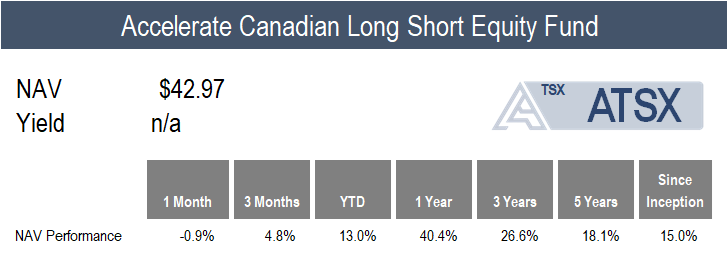

ATSX declined -0.9% in June, compared to the benchmark S&P/TSX 60’s 1.7% gain.

Multi-factor long short performance in Canada was mixed last month, with positive returns from the value and quality portfolios, partially offset by declines in the price momentum, operating momentum, and trend portfolios.

Top Fund contributors include short positions in Novagold Resources, Perpetua Resources, and Nexgen Energy. Top Fund detractors include long positions in Kinross Gold and B2Gold, along with a short position in Interfor.

![]()

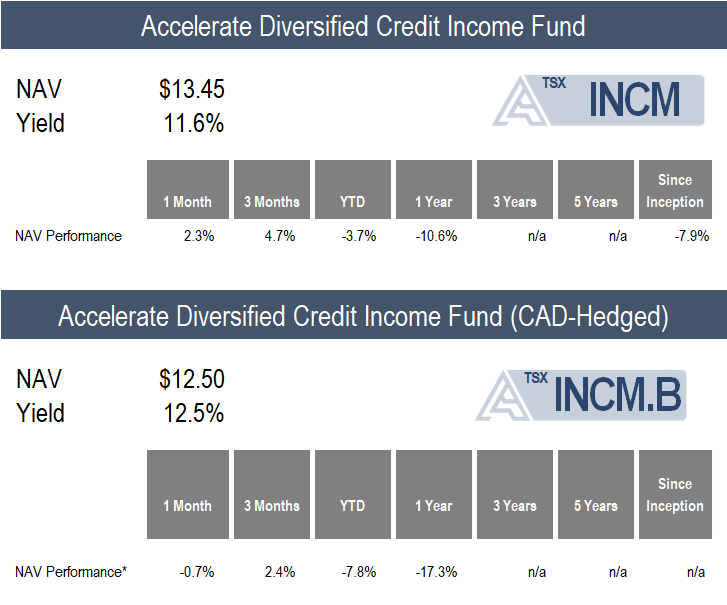

INCM gained 2.3% in June (-0.7% on a CAD-hedged basis) as the median publicly-traded BDC saw its NAV discount widen from -22.6% to -26.4%

We will get a check-up on the state of private credit as BDCs report second-quarter results over the next few weeks, with Ares Capital Corporation kicking off Q2 reporting on July 29th, followed by others throughout the first half of August.

Currently, INCM is allocated to 20 private credit portfolios (through listed BDCs), totalling more than 5,000 loans and investments, of which 86.7% are senior secured and 92.5% are floating rate. The current yield on the INCM portfolio is 12.2%, and it trades at a -22.1% discount to its net asset value. INCM’s exposure to software loans is 16.8% of its portfolio.

![]()

Have questions about Accelerate’s investment strategies? Click below to book a call with me:

-Julian

Disclaimer: This distribution does not constitute investment, legal or tax advice. Data provided in this distribution should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. Please read the relevant prospectus before investing. For a summary of the risks of an investment in the Accelerate ETFs, please see the specific risks set out in the prospectus. ETFs are not guaranteed and the information in this distribution is based on current market conditions and may fluctuate and change in the future. Past performance is not indicative of future results. Decisions regarding tax, investments, and all other financial matters should be made solely with the guidance of a qualified professional. Visit www.AccelerateShares.com for more information.