March 16, 2025 – The Tariff Act of 1890, commonly known as the McKinley Tariff, was a piece of protectionist trade policy passed in 1890 during the administration of President Benjamin Harrison. Sponsored by Representative William McKinley (R-Ohio), who later became president, the Act aimed to protect American industries by raising tariffs on imported goods to nearly 50% on average. It sought to shield American manufacturers and farmers from foreign competition, reflecting the Republican Party’s strong protectionist stance at the time. The initiative was framed as a way to boost domestic industry and protect jobs.

The high tariffs increased the cost of imported goods, raising prices for American consumers. Domestic producers, protected from competition, also hiked prices, leading to widespread public discontent. Everyday items like clothing, household goods, and food became more expensive, hitting working-class families hardest at a time when wages were stagnant. As expected, foreign nations responded with their own tariffs on U.S. exports, particularly agricultural goods. Countries like Canada and European nations reduced imports of American farm products, hurting farmers who had initially supported the tariffs. This retaliation shrank export markets, negating some of the intended benefits for U.S. producers.

The McKinley Tariff was quickly proven an economic and political failure. It was extremely unpopular, leading to a massive defeat for Republicans in the 1890 midterm elections. In the 1892 presidential election, Democrat Grover Cleveland defeated President Benjamin Harrison, partly due to public anger over high tariffs. In 1894, the McKinley Tariff was repealed and replaced.

Fast forward 40 years. In 1930, the Smoot-Hawley Tariff Act was signed into law. This U.S. legislation raised tariffs on over 20,000 imported goods to record levels, aiming to protect American farmers and industries from foreign competition during the onset of the Great Depression. At the time, the U.S. was experiencing economic distress following the stock market crash of 1929. Farmers were struggling due to overproduction and falling prices, and lawmakers believed that raising tariffs would protect domestic industries and preserve American jobs.

At the time, over 1,000 economists signed a letter urging Hoover to veto the bill, warning it would harm the economy. In addition, many business leaders also opposed it, but Hoover signed it into law anyway.

Unsurprisingly, other countries responded by imposing tariffs on U.S. exports, reducing demand for American goods abroad. Countries like Canada, France, and the U.K. imposed counter-tariffs, significantly hurting U.S. agriculture and manufacturing. Ultimately, global trade plummeted nearly -66% between 1929 and 1934, worsening the Great Depression.

While the Act was meant to protect American businesses, it backfired as U.S. companies lost access to foreign markets. Farmers, in particular, were hit hard because agriculture depended heavily on exports. Rather than protecting jobs, it contributed to higher unemployment as export-dependent industries, such as agriculture and manufacturing, suffered significant losses.

As expected, the Smoot-Hawley Tariff Act was a spectacular economic failure, which deepened and prolonged the Great Depression rather than alleviated it. In 1934, President Franklin D. Roosevelt implemented the Reciprocal Trade Agreements Act of 1934, which lowered tariffs and promoted freer trade, marking a swift move away from protectionism.

The more things change, the more they stay the same.

Donald Trump was elected as the 47th U.S. President last fall under the mandate of economic growth and deregulation. Despite inheriting an economy performing remarkably well, along with the world’s top-performing and most influential stock market, things took a dramatic reversal just weeks after inauguration. Under the guise of creating an industrial renaissance in the U.S. and bringing back manufacturing jobs to the rustbelt, Trump quickly implemented a series of tariffs, which quickly escalated into rising trade disputes and a trade war with its key trading partners, notably Canada, Mexico, China, and the European Union. These conflicts, which were initiated by the U.S. imposing tariffs on imports unprovoked, led to a cycle of back-and-forth retaliatory measures.

One does not need a PhD in economics to know the expected result. The Tariff Act of 1890, the Smoot-Hawley Tariff Act of 1930, and all other implementations of tariffs resulted in economic pain, uncertainty, and volatility, while failing to fix the underlying economic issues they were meant to address.

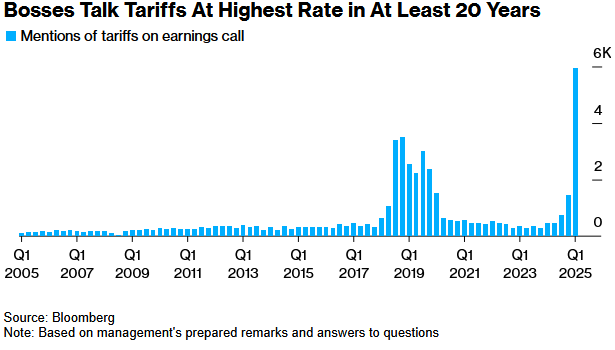

In terms of adverse economic effects, the first and most rapid is business uncertainty. The mentions of tariffs by business executives on earnings calls have risen to a record high.

With respect to executives’ views on tariffs, they are nearly universally negative (unless one runs a U.S.-based steel mill).

As retaliatory measures by trade partners are implemented, economic uncertainty rises. Affected countries have rapidly imposed counter-tariffs on U.S. exports, harming American industries such as agriculture and manufacturing.

Soon, we will see inflation creep in, as high import duties lead to increasing prices for consumer and industrial goods. Rising prices, economic uncertainty, and expanding trade disputes contribute to a slowdown in global economic growth.

Nevertheless, I was told there would be winning.

While Trump was elected on a mandate of economic growth and deregulation, the early result of his administration was economic consternation caused by a massive increase in regulations via tariffs.

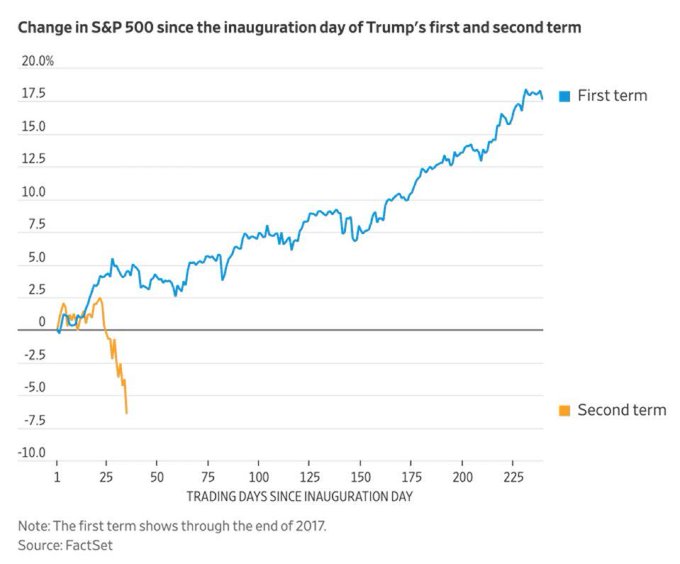

The stock market reacted as expected. Its correction was swift, with the S&P 500 falling -10% in just 20 days, representing the 5th fastest market correction since 1950.

Meanwhile, economists are ratcheting up the odds of a U.S. recession as markets continue to fall.

Source: CNN

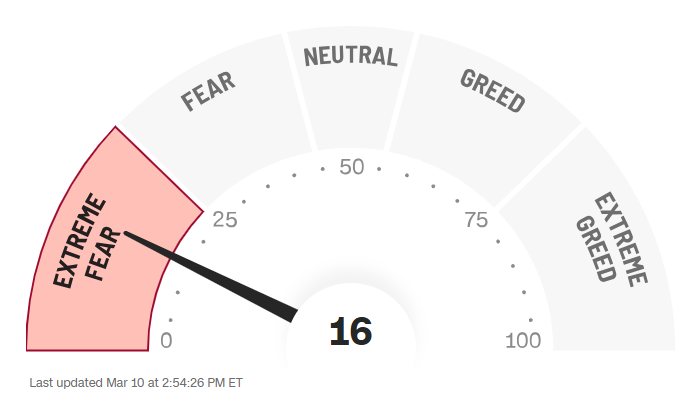

Both Fed Funds futures, now pricing in three rate cuts this year, and the Fear & Greed Index, now at an “extreme fear” rating, are signalling a near-term recession. All of this is mostly preventable, if someone just kept Trump away from posting on social media (he has announced much of his tariff plans via his social media platform, Truth Social).

While many of us (including yours truly) expected his initial tariff threats to be just saber-rattling, most market participants are surprised the trade war has gone this far. The 2025 tariffs will likely fail to produce the intended benefits, just as various implementations of tariffs have consistently failed throughout history.

Ultimately, cooler heads will likely prevail at some point. The key concern for investors is how much economic damage will be sustained, and how far risk assets will decline, until the trade wars subside. Ultimately, it is determined by one man, who has proven to be quite unpredictable. Nevertheless, for the time being, the current market dislocation may create some compelling opportunities for allocators to put capital to work. Stay vigilant.

Accelerate manages five alternative investment solutions, each with a specific mandate:

- Accelerate Arbitrage Fund (TSX: ARB): Merger Arbitrage

- Accelerate Absolute Return Fund (TSX: HDGE): Absolute Return

- Accelerate OneChoice Alternative Portfolio ETF (TSX: ONEC): Multi-Asset

- Accelerate Canadian Long Short Equity Fund (TSX: ATSX): Long Short Equity

- Accelerate Diversified Credit Income Fund (TSX: INCM): Private Credit

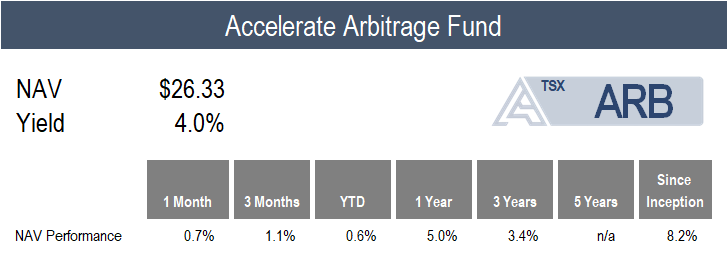

ARB gained 0.7% in February on the back of an active deal environment.

A handful of mergers closed throughout the month, crystalizing gains for the Fund, while active spreads remained stable amidst market volatility. Completed transactions include Quikrete’s merger with Summit Materials, Blackstone’s buyout of Retail Opportunity Investments, Silver Lake and GIC’s take-private of Zuora, Stryker’s acquisition of Inari Medical, Platinum Equity’s buyout of Héroux-Devtek, and National Bank’s merger with Canadian Western Bank. To capitalize on a market inefficiency and generate higher risk-adjusted returns, the Fund invested in the subscription receipts issued by National Bank to fund the Canadian Western Bank deal instead of buying the underlying stock outright. Historically, subscription receipt arbitrage is underfollowed, and almost always offers superior risk-adjusted returns compared to the underlying merger arbitrage spread.

The Fund added 6 new merger arbitrage investments in February (3 in the U.S. and 3 in Canada), while adding 4 to the watchlist to add to the portfolio once the spread widens to meet the Fund’s requisite hurdle rate out of 15 M&A deals announced in North America.

Currently, the Fund is allocated 50% to merger arbitrage (32% strategic and 18% private equity buyouts) and 50% SPAC arbitrage. The Fund is 125.8% long and -8.9% short, representing 134.7% gross exposure.

![]()

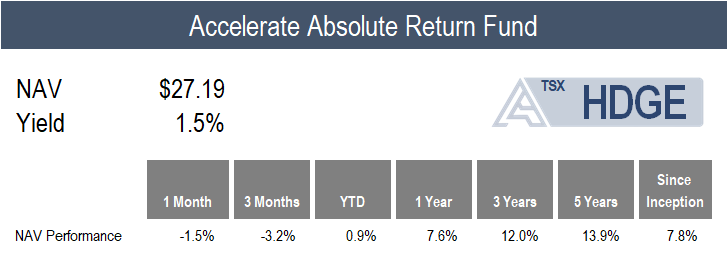

HDGE returned -1.5% in a mixed month for systematic long short equity in North America.

In terms of U.S. multifactor performance, most long short factor portfolios generated alpha last month. Undervalued stocks outperformed overvalued, high quality stocks outperformed low quality, stocks with positive momentum outperformed those with negative momentum, and stocks beating expectations outperformed those missing expectations. However, in a declining tape, all top decile long and bottom decile short portfolios fell, although the shorts fell more than the longs. As HDGE is positioned 110% long and 50% short, although the short positions were “working”, they did not fall enough to fully offset the declines in the long portfolio.

Top Fund contributors to February’s return include short positions in PBF Energy, CryoPort, and Bloomin’ Brands. Conversely, top detractors include short positions in Corsair Gaming, Lions Gate Entertainment, and Brookdale Senior Living.

![]()

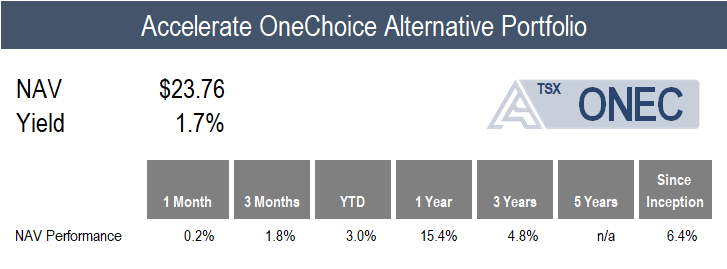

ONEC gained 0.2% last month, bringing its year-to-date appreciation to 3.0%.

The Fund’s well-diversified, multi-asset approach shines during uncertain times. We know the investment approach is working when the underlying allocations generate a set of dispersed and uncorrelated return streams, with some “working” and others “not working”. When assembled into a multi-asset portfolio, this approach should generate a low-volatility return stream that generates relatively consistent performance, given the underlying uncorrelated asset returns.

This approach was exemplified last month, as the Fund’s various allocations produced relatively dispersed returns. Although some were negative, they were slightly offset by the positive performers.

The top performers in the Fund’s allocation include risk parity, real estate, and infrastructure, which returned 2.8%, 1.9%, and 1.8%, respectively. Also contributing positively include ONEC’s allocations to merger arbitrage, gold, and leveraged loans, which all returned less than 1.0%.

On the negative side of monthly performance include various hedge fund allocations, including managed futures, absolute return, and long short equity, which declined by -2.2%, -1.5%, and -1.0%, respectively. In addition, the private credit and commodity allocations declined by -1.0% or less.

![]()

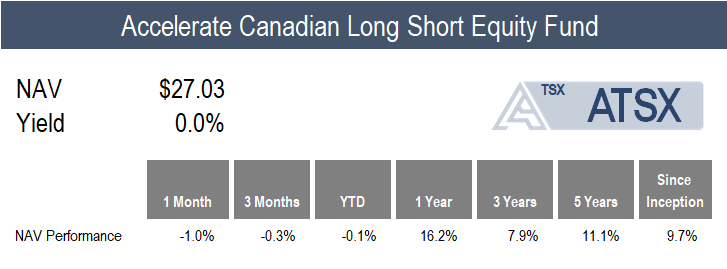

ATSX declined by -1.0% for the month compared to the benchmark TSX 60’s -0.4% dip.

Systematic long short equity in Canada underperformed last month, as bottom decile shorts outperformed top decile longs in the long-short value, price momentum, operating momentum, and trend portfolios. Quality was the only factor that generated alpha, however, while low quality stocks fell -3.3%, high quality stocks fell -1.8%, which did not help long-biased portfolios much.

Top contributors to the Fund in February include long positions in Dundee Precious Metals and Great-West Lifeco, along with a short position in NexGen Energy. Top detractors include short positions in Innergex Renewable, SSR Mining, and Northland Power.

![]()

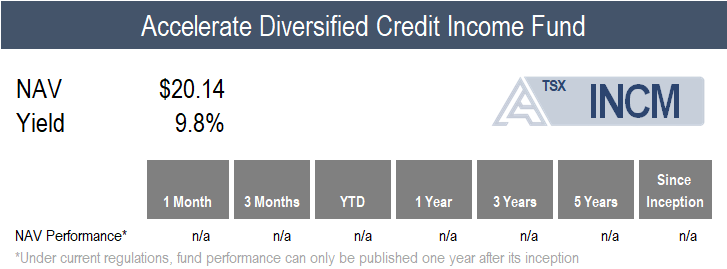

INCM declined -1.0% last month as private credit NAV discounts began re-emerging with the bout of market volatility.

The liquid private credit market mostly completed its Q4 reporting by the end of February. We discussed the results in the latest Accelerate Liquid Private Credit Monitor:

Credit conditions remain benign, despite significant macro uncertainty. Private credit spreads have stabilized over the past three quarters, settling in at 500bps – 550bps for core middle market loans (with upper middle market unitranche loans at 475bps – 500bps). Direct lenders noted that spread compression has been more pronounced in the broadly syndicated loan market than in the private credit market. Private markets continue to perform well, with no signs of a slowdown.

While spreads have tightened and base rates have declined over the past 18 months, the average BDC portfolio yield in Q4 was still high at 11.8%. The direct lending market remains one of the most resilient asset classes, and private credit spreads compared to public markets continue to be attractive.

Many BDCs have been transitioning their loan books to first lien and unitranche loans, and fewer unsecured loans, preferring safety of principal by migrating their capital to the top of the capital structure.

In terms of results, Ares Capital (NASDAQ: ARCC) and Blackstone Secured Lending (NYSE: BXSL) led the private credit market with exceptional fourth quarter results… There were strong fourth quarter results from Nuveen Churchill Direct Lending (NYSE: NCDL), Pennantpark Floating Rate Capital (NYSE: PFLT), Morgan Stanley Direct Lending Fund (NYSE: MSDL), and Kayne Anderson BDC (NYSE: KBDC). In terms of challenged loan books, Oaktree Specialty Lending (NASDAQ: OCSL) has experienced some difficulties, while BlackRock TCP Capital (NASDAQ: TCPC) has struggled immensely, having more loan write-downs than any other BDC. Unfortunately, TCPC was a lender to several private equity-owned companies that ran into trouble last year, including Securus, McAfee, Pluralsight, Thrasio, Razor, Astra, and Khoros. Management of both OCSL and TCPC implemented initiatives to right the ship, such as fee reductions and the reduction of lending activity in challenged sectors. Meanwhile, both of these BDCs trade at double-digit discounts to their net asset values.

While credit quality remains good, and BDC performance remains relatively solid, this month’s trade war-related market volatility has caused listed BDCs to trade down and yields to rise.

Currently, INCM is allocated to 20 private credit funds, representing over 4,000 loans, of which 87.0% are secured and 93.7% are floating rate. The Fund portfolio yields 11.6% and trades at an aggregate -4.6% discount to NAV, with 90% of the private credit funds held trading at a discount to NAV in the secondary market.

![]()

Have questions about Accelerate’s investment strategies? Click below to book a call with me:

-Julian

Disclaimer: This distribution does not constitute investment, legal or tax advice. Data provided in this distribution should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this distribution is based on current market conditions and may fluctuate and change in the future. No representation or warranty, expressed or implied, is made on behalf of Accelerate Financial Technologies Inc. (“Accelerate”) as to the accuracy or completeness of the information contained herein. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Past performance is not indicative of future results. Visit www.AccelerateShares.com for more information.