June 1, 2026 – The great SPAC boom kicked off in the spring of 2020 as markets bounced back from the record-quick Covid bear market. Due to the pandemic-led global recession, governments and central banks around the world unleashed an unprecedented combination of fiscal and monetary policy that got the economic animal spirits flowing. Investors of all stripes were keen to put money into the market.

At the time, special purpose acquisition companies went from a niche backwater asset class in which most investors paid no attention to front-page news with surging share prices amid blockbuster, multi-billion dollar deal announcements.

A thundering bull market in speculative sectors had emerged, driven by a massive increase in retail investor participation. Electric vehicles, battery technology, quantum, space, fintech and other high-growth stories attracted hordes of speculators, who pushed these highly risky plays skyward. Historically, skeptics have referred to these unprofitable, highly-valued early-stage companies as “story stocks”.

Story stocks are companies whose investment appeal is driven more by a compelling narrative than by current business fundamentals such as earnings or cash flow. Examples include companies tied to themes like EVs, AI, space, or crypto. They tend to trade at extreme valuation multiples because investors price in years of future potential upfront. Story stocks can produce spectacular gains when the narrative works, but they can be brutal when reality fails to live up to the dream.

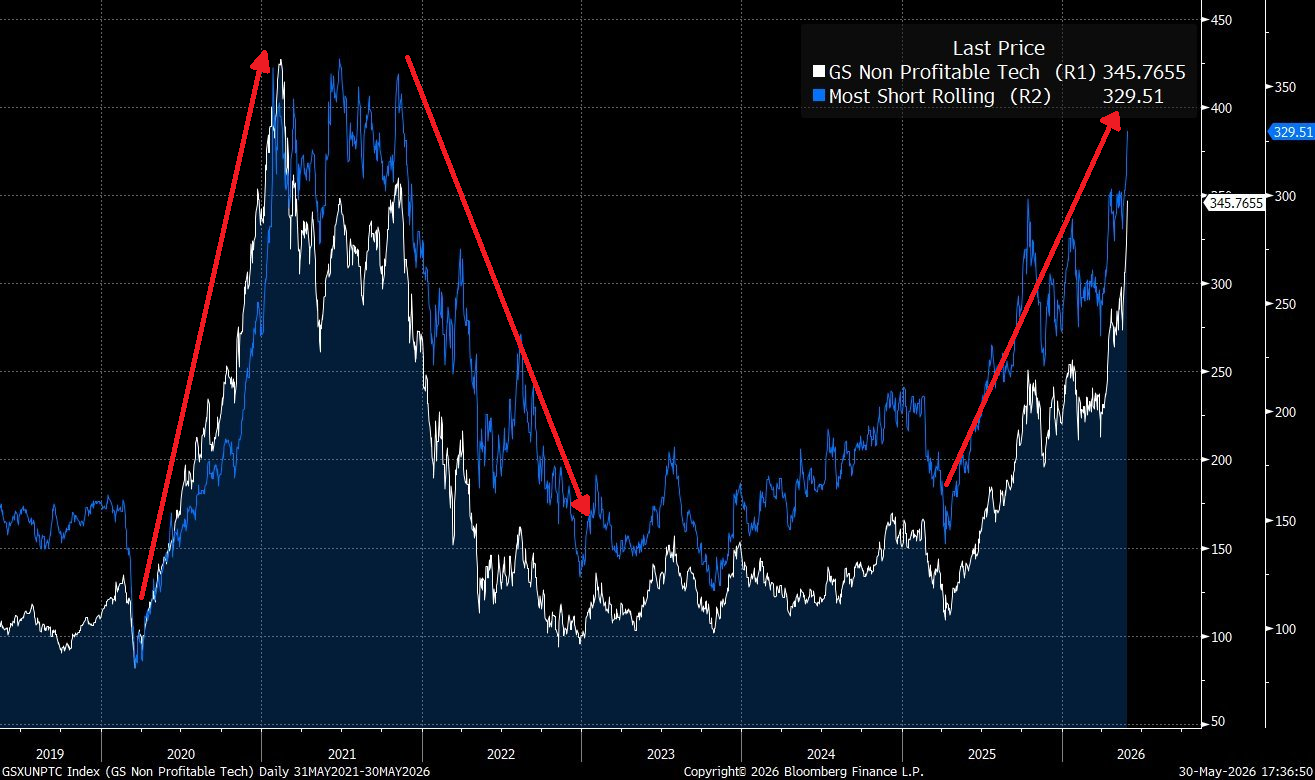

Between the March 2020 nadir and the February 2021 peak in speculative growth and story stocks, two indices that best represented these baskets of retail bets, the GS Non Profitable Tech basket and the GS Most Shorted Stocks basket, both surged nearly 400%.

Once the boom turned to bust (as it usually does for stocks not supported by fundamentals), the indices of speculative, unprofitable technology and heavily shorted stocks crashed by nearly -80% by the end of 2022.

Source: Accelerate, Bloomberg

At that point in time, investors had dug a grave for SPACs, assuming they died off in the bear market that year.

Cycles change, but human nature does not. Speculation is timeless.

Just five years later, the speculative juices are flowing once again. Degenerate gambling in the riskiest story stocks has made a huge comeback. A (presumably) new army of speculators has driven the GS Unprofitable Tech basket up nearly 200% since last spring. This cycle’s story stocks make up some of the same sectors as the previous – quantum, nuclear, AI, space, and others.

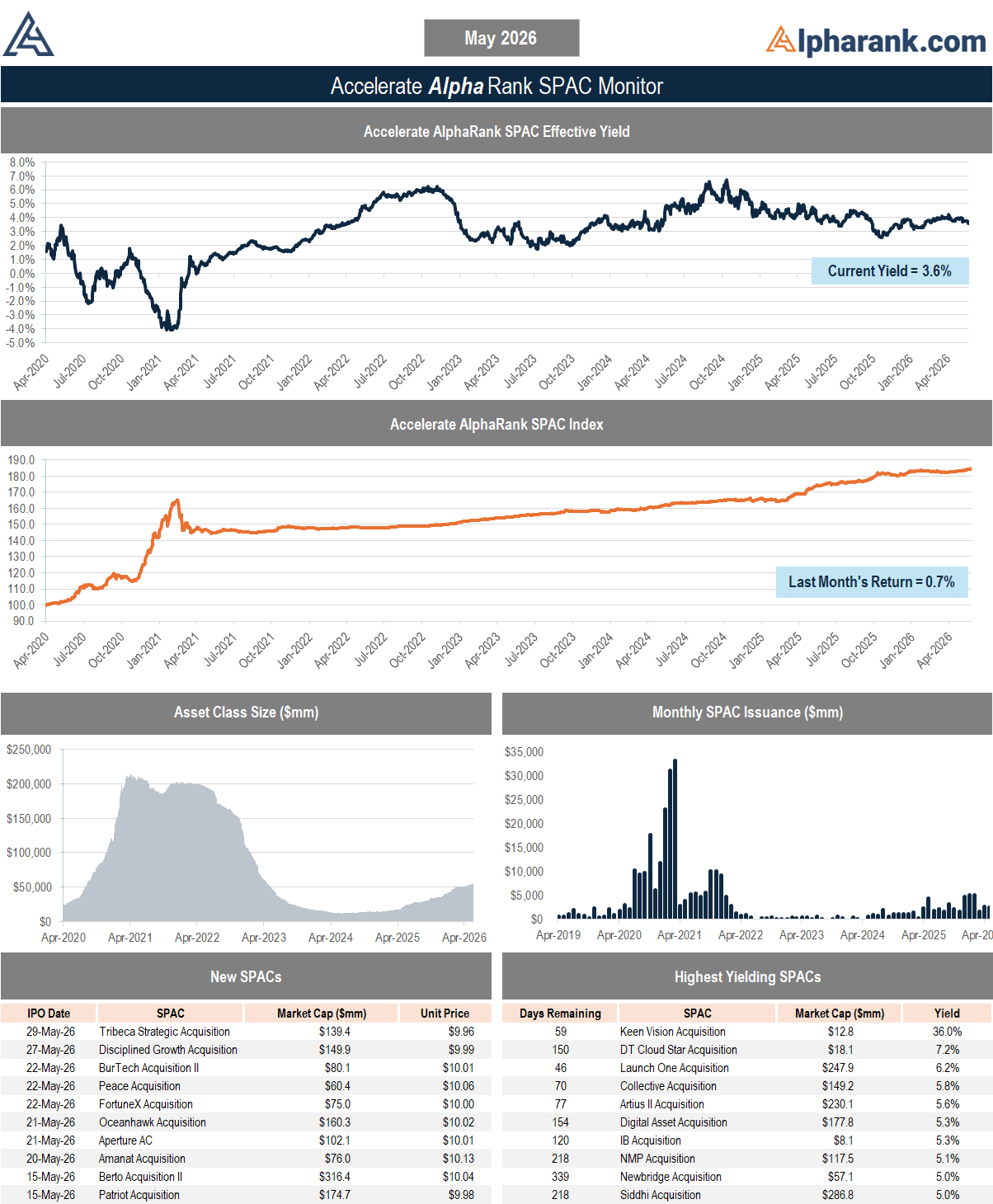

One market segment that failed to get the message of a new speculative bull market is SPACs.

While the SPAC market has grown five-fold since its summer 2024 bottom of just $11 billion (however, the current $55 billion aggregate SPAC market cap is still down -75% from the early 2021 peak of $214 billion), it has not gotten the message of this surge in market speculation and face-ripping rally in story stocks.

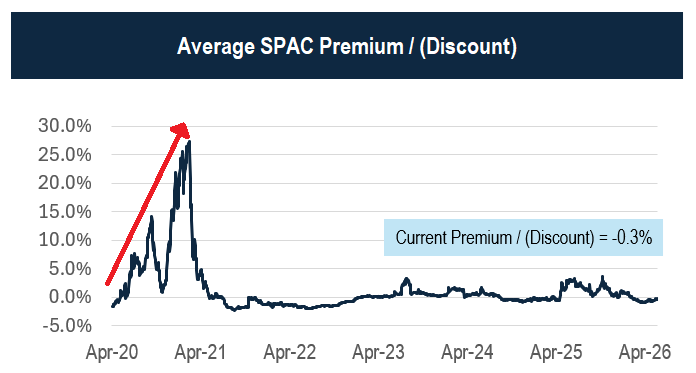

During the last bull market in high-growth stocks five years ago, SPAC shares surged and reached an average NAV premium (average trading price above their cash in trust) of nearly 30%.

Now, as SPACs have failed to participate in the current rally, they remain stuck in the mud, trading at a discount to NAV on average.

Source: Accelerate

Whether SPACs have been forever forgotten, or their rally skyward in sympathy with other story stocks is a delayed inevitability, there remain several blank check companies that have announced mergers in the sweet spot of attractive market stories:

- Bleichroeder Acquisition II (BBCQ) announced a $2.0 billion merger with quantum computing company Pasqal on March 4th, 2026. Since then, BBCQ shares have ticked up just 6.8% while its peers have surged by 61.0%.

- Axiom Intelligence Acquisition 1 (AXIN) announced a $3.6 billion merger with quantum computing company Terra Quantum on May 26th, 2026. Since then, some of its peers have rallied by more than 10%, while AXIN gained just 1.7%.

- Real Asset Acquisition (RAAQ) announced a $1.8 billion merger with quantum computing company IQM on February 23rd, 2026. Since then, its peers have gained 78.1% compared to RAAQ’s 10.2%.

- Archimedes Tech SPAC Partners II (ATII) announced a $1.3 billion merger with semiconductor equipment and advanced materials company Forge Nano on April 20th, 2026. Since then, its sector peers have gained an average of 24.9% while ATII has increased by 7.3%.

- D. Boral ARC Acquisition I (BCAR) announced a $0.5 billion merger with AI compute infrastructure platform Exascale Labs on January 12th, 2026. Since the deal was announced, its peers have rallied by 56.3% while BCAR has gained 9.4%.

We have already seen that dynamic re-emerge across quantum computing, space, nuclear, AI-adjacent infrastructure, and other story stocks, where narratives have reignited and share prices have responded. Yet SPAC mergers, despite offering many of the same ingredients that fuel speculative enthusiasm, growth potential, disruption, scarcity, and a clean public-market vehicle, have been left behind. That disconnect may not last.

If risk appetite continues to broaden, SPACs could represent a coiled spring: compressed by years of disappointment, ignored by many investors, but increasingly positioned to snap back as the market once again embraces the promise of what could be.

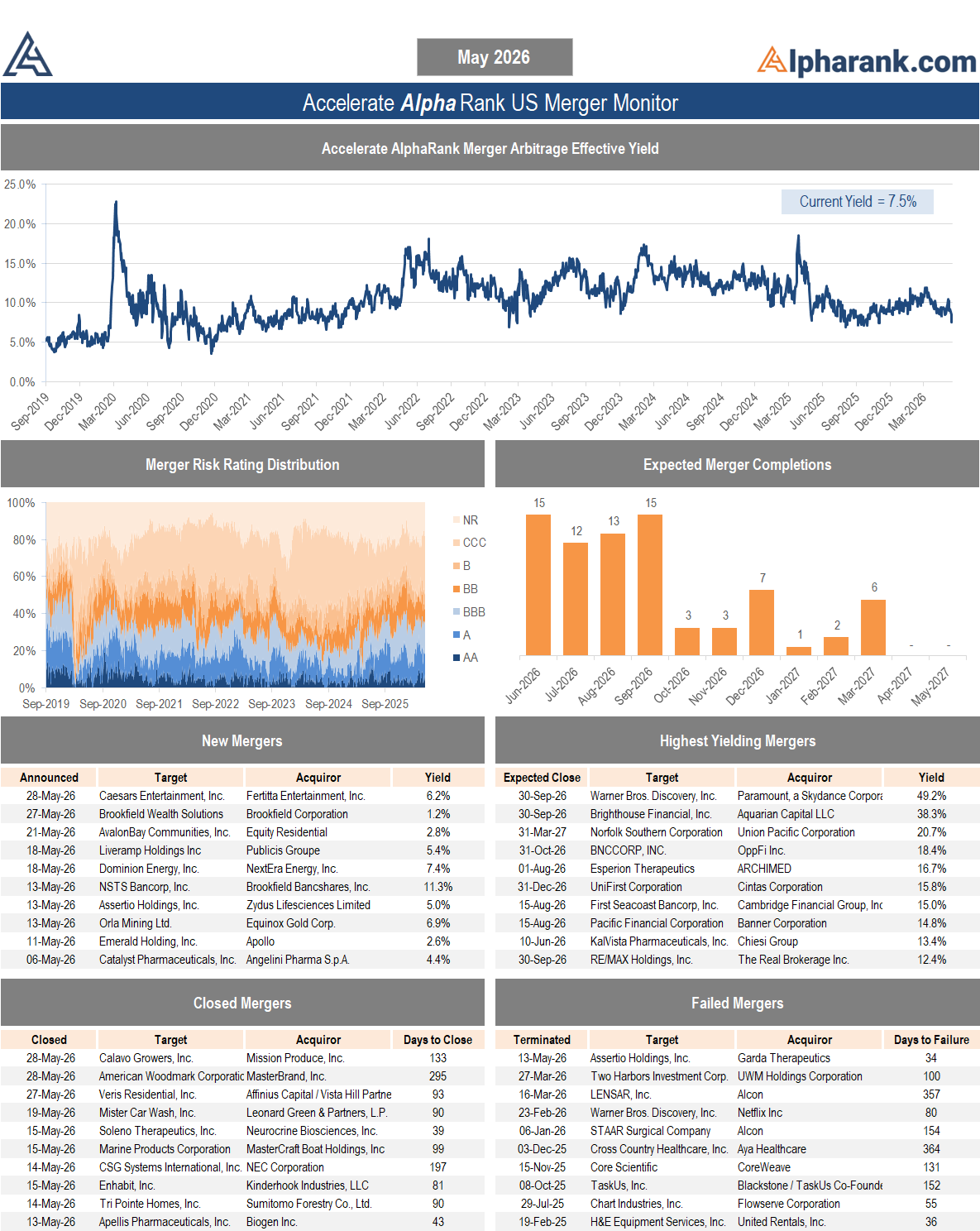

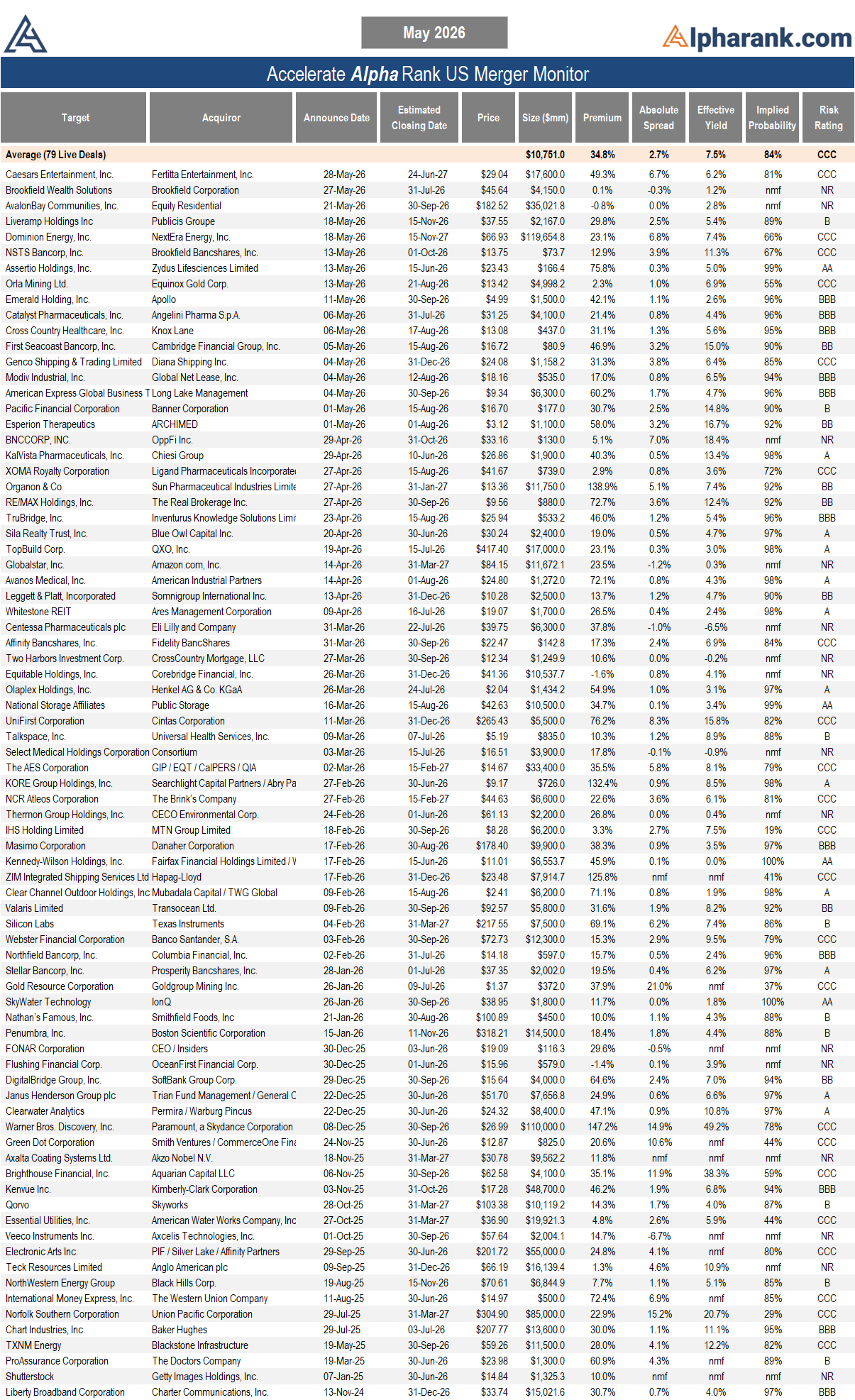

The AlphaRank.com Merger Monitor below represents Accelerate’s proprietary analytics database on all announced liquid U.S. mergers. The AlphaRank Merger Arbitrage Effective Yield represents the average annualized returns of all outstanding merger arbitrage spreads and is typically viewed as an alternative to fixed income yield.

Each individual merger is assigned a risk rating:

- AA – a merger arbitrage rated ‘AA’ has the highest rating assigned by AlphaRank. The merger has the highest probability of closing.

- A – a merger arbitrage rated ‘A’ differs from the highest-rated mergers only by a small degree. The merger has a very high probability of closing.

- BBB – a merger arbitrage rated ‘BBB’ is of investment grade and has a high probability of closing.

- BB – a merger arbitrage rated ‘BB’ is somewhat speculative in nature and has a greater than 90% probability of closing.

- B – a merger arbitrage rated ‘B’ is speculative in nature and has a greater than 85% probability of closing.

- CCC – a merger arbitrage rated ‘CCC’ is very speculative in nature. The merger is subject to certain conditions that may not be satisfied.

- NR – a merger-rated NR is trading either at a premium to the implied consideration or a discount to the unaffected price.

The AlphaRank merger analytics database is utilized in running the Accelerate Arbitrage Fund (TSX: ARB), which may have positions in some of the securities mentioned.

* AlphaRank is exclusively produced by Accelerate Financial Technologies Inc. (“Accelerate”). Visit Alpharank.com for more information. Disclaimer: This research does not constitute investment, legal or tax advice. Data provided in this research should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this research is based on current market conditions and may fluctuate and change in the future. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Accelerate may have positions in securities mentioned. Past performance is not indicative of future results.