November 24, 2025 – The biggest bull versus bear debate in years is playing out in the capital markets over the frenzied level of AI data center capital expenditures, and whether such spending will prove justified via an adequate return on capital.

The bulls believe that the AI-driven bull market is still in its early stages, with steadily rising revenue forecasts far into the future and smooth sailing ahead for demand for artificial intelligence services from consumers and industry.

The bears believe that tech bubble 2.0 is playing out, with market participants warning of ominous similarities to the internet infrastructure boom in the late 1990s, when capital was overinvested and thus incinerated, as market forecasts proved overly optimistic.

Meanwhile, even tech luminaries involved in the build out of the AI industry have issued warnings to investors. Amazon founder Jeff Bezos described the current AI investment boom as an “industrial bubble“. At the same time, Meta’s CEO Mark Zuckerberg and OpenAI’s CEO Sam Altman both warned of a potential bubble in the buildout of AI infrastructure. Google CEO Sundar Pichai noted “irrationality” in the current AI boom.

In contrast, AI’s primary beneficiary, Nvidia, begs to differ. Nvidia Chief Executive Jensen Huang addressed the debate last week, stating, “there’s been a lot of talk about an AI bubble. From our vantage point, we see something very different.”

In any event, it is rational to observe the AI industry’s massive investment and limited profits and question whether the AI race can continue at its current pace. Hundreds of billions of dollars have been spent, while sufficient revenue growth has not yet occurred to justify the capital investment. In addition, some investors, including the Big Short’s Michael Burry, are flagging potential accounting issues behind the graphics processing unit (GPU) chips powering the AI revolution, while others are questioning the circular nature of business deals between the leading players in the space.

More experienced market participants will remember how prevalent such vendor financing relationships were during the late 1990s tech and telecom bubble.

In contrast to the bear case, the AI and stock market bulls have solid data backing their cause.

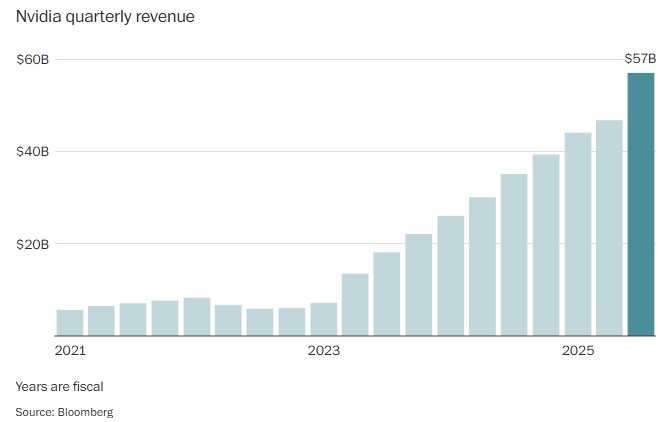

First, the undeniable leader of the AI revolution and the world’s most valuable public company, Nvidia, is generating unprecedented revenue growth at scale. The ringleader of the bulls has year-over-year revenue growth of 62%, rising to nearly $60 billion in sales last quarter.

In addition, this revenue growth has been accompanied by a prodigious amount of free cash flow generation. Nvidia’s free cash flow has grown from $3.8 billion in the year to January 2023 to an estimated $96.5 billion in the year ending this coming January. This unprecedented profit growth stands in stark contrast to the firms leading the internet bubble twenty-five years ago.

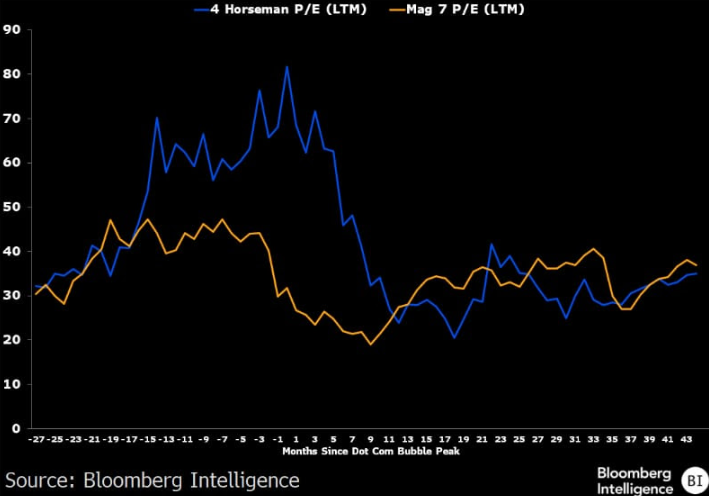

Second, bulls contrast the lofty valuations of the four leading internet firms during the 1990s tech bubble to those of the magnificent 7 stocks leading today’s market. At the peak of the bubble in the spring of 2000, leading firms’ earnings multiple reached more than 80x. In contrast, Mag7 stocks trade at less than 40x earnings currently.

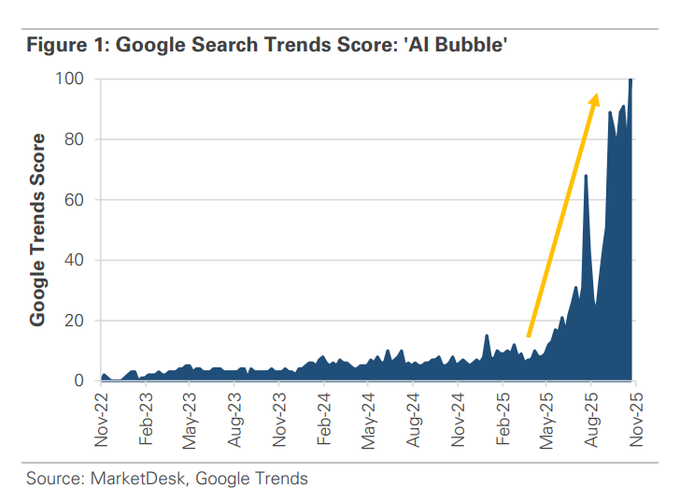

Despite the data supporting the bull thesis, the market’s concern regarding an AI bubble has steadily grown. Google searches for the term “AI Bubble” have surged since the spring.

Whether one is bullish or bearish, it is undeniable that sentiment has shifted recently. Three notable developments support this shift.

First, Nvidia’s blowout quarterly results announced last week were met with tepid investor enthusiasm. In fact, despite topping consensus estimates for many consecutive quarters with nearly unprecedented earnings growth, Nvidia hasn’t wowed the market with a post-earnings-day share price bump since May 2024.

Source: Bloomberg, Accelerate

Imagine what would happen to the stock if Nvidia were to merely meet the Street’s lofty expectations, let alone miss expectations. Remember, Nvidia is 8% of the S&P 500, and AI-adjacent stocks represent more than a third of the popular equity index. The implications are significant.

Next, the reflexive nature of the AI infrastructure buildout is changing rapidly. While Nvidia’s recent quarterly performance was truly exceptional, reflecting voracious demand for its GPUs through October, the market’s sentiment toward AI-related capex has turned fairly dramatically since then.

Two major recent examples highlight this dynamic:

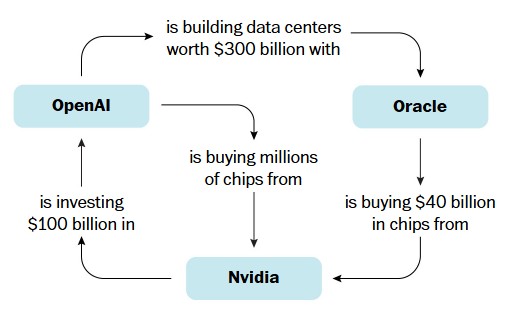

- Oracle’s $300 billion data center agreement with OpenAI announced in September was initially lauded by investors, generating more than $250 billion in shareholder value via in increase in its market capitalization, in what appeared to be a highly accretive deal. However, since then, investor support of data center investment has cooled dramatically, and the OpenAI deal has now cost Oracle shareholders $60 billion of lost value. Hyperscalers may think twice regarding data center investments if they are dilutive to shareholder value, and management teams may face increasing shareholder pressure to scale back AI infrastructure capex if their share prices are underperforming.

- Despite announcing exceptional third quarter results, Meta has lost $400 billion in market cap since announcing its third quarter results three weeks ago, primarily due to increased AI-related spending. Meta is a social media company, and a tremendous one at that. It doesn’t need AI. Several years ago, it was spending like a drunken sailor on its metaverse initiative, costing shareholders tens of billions of destroyed capital. Shareholders were rewarded to the tune of more than $500 billion of increased market value for the company once this unsuccessful initiative was shelved. A similar value creation dynamic could play out for Meta if it ceases its insatiable GPU buying spree in support of its artificial intelligence gambit.

Reading the tea leaves, investor sentiment toward highly capital intensive data center (i.e. GPU) capital expenditures has recently turned from red hot to ice cold, and from seemingly accretive to shareholder value to dilutive. If management teams reduce their spending plans to account for potential shareholder pressure stemming from stock price underperformance, this could alter the outlook for GPU and data center demand markedly, with massive implications for the capital market writ large.

On the other hand, if AI-related investor sentiment turns back to positive and the market once again rewards AI infrastructure spending with booming stock prices, then the great AI bull market will continue.

For now, the bull-bear debate regarding an AI bubble is unresolved. However, amid rising uncertainty regarding future AI infrastructure spending and its implications, investors may benefit from taking a hedged approach in their equity allocation in order to enhance downside protection. To help facilitate idea generation, we highlight one top-decile stock that is forecasted to outperform and one bottom-decile stock that is predicted to underperform in this month’s AlphaRank Top Stocks.

OUTPERFORM: Power Corporation of Canada (TSX: POW) is a diversified financial services business focused on insurance, wealth management and investment management. Its diversified portfolio of holdings and business lines provides stability and consistency. Despite strong recent business performance and share price performance, along with intelligent capital allocation (growth initiatives, dividend, and share repurchases), it still trades at a discount to its net asset value, providing underlying support for the stock. With a beta of 0.6, it is a defensive stock that should be a strong relative performer in a weak or choppy market. With positive stock price momentum, along with an AlphaRank score of 92.0/100, we expect POW shares to continue to outperform. Disclosure: Long POW shares in the Accelerate Canadian Long Short Equity Fund (TSX: ATSX).

UNDERPERFORM: Strategy Inc (NASDAQ: MSTR) is a bitcoin treasury company. MSTR currently trades at an MNAV of 1.2x, meaning that it trades at a 20% premium to the value of its bitcoin holdings. MSTR’s business model is reliant on the greater fool theory – finding additional speculators to buy the stock at a premium to its NAV so it can issue more shares. The bloom has come off the rose for digital asset treasury companies and MSTR, with rapidly increasing competition in the digital asset treasury space, combined with declining sentiment, leading to NAV premiums evaporating and the business model starting to fall apart. We expect MSTR to trade to a discount to its net asset value in the future, and therefore holders are better off selling MSTR and owning a bitcoin ETF instead (if they want to maintain BTC exposure). With a beta of 3 and an AlphaRank score of 19.4/100, stocks like MSTR should be avoided.

A further discussion regarding POW and MSTR, along with the current market environment, can be found on our BNN Bloomberg appearance last week: Hot Picks – Defensive stock ideas for investors wary of a frothy market.

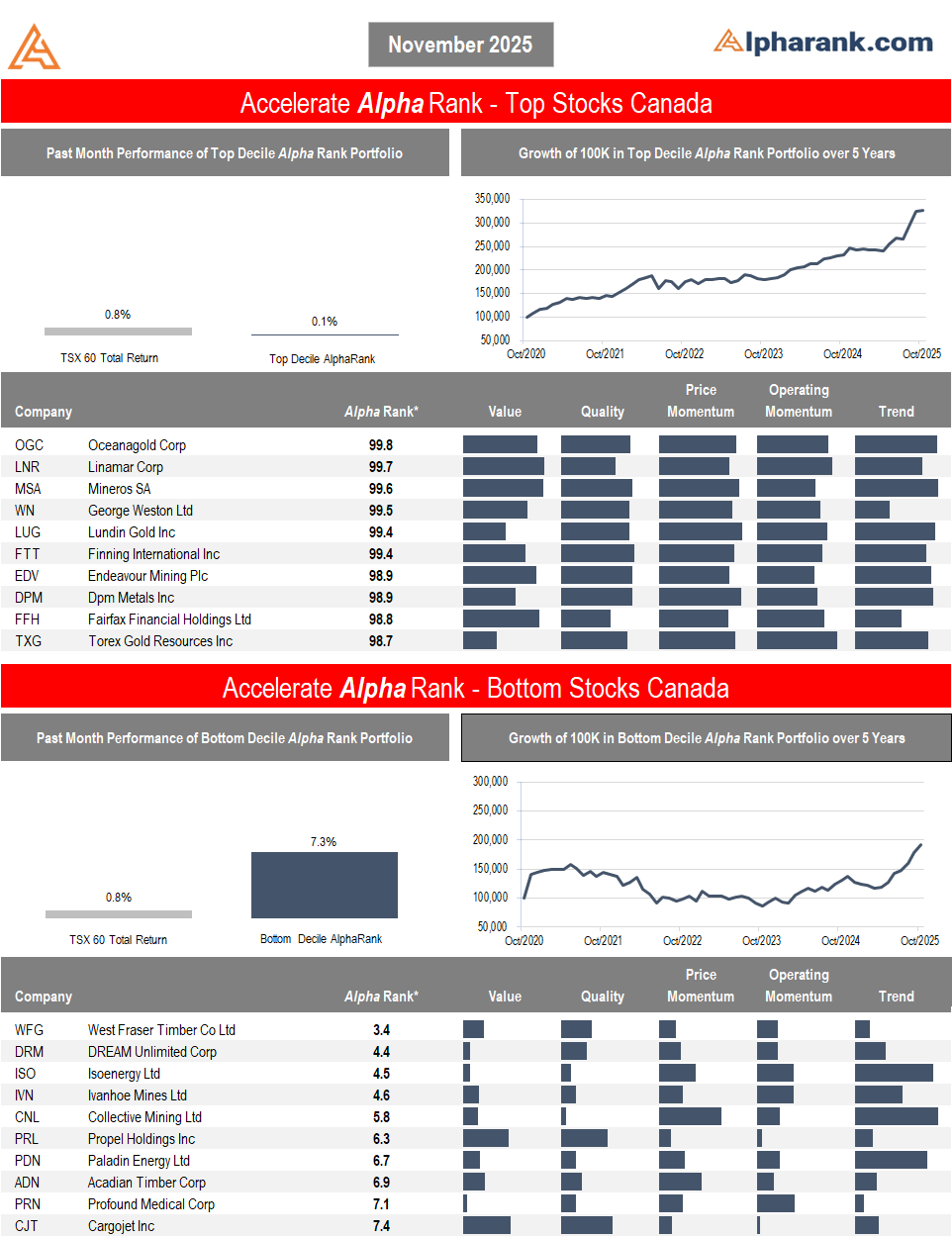

The AlphaRank Top and Bottom stock portfolios exhibited negative relative performance last month:

- In Canada, the top-ranked AlphaRank portfolio of stocks returned 0.1%, underperforming the benchmark’s 0.8% return, while the bottom-ranked portfolio of Canadian equities gained 7.3%. The long-short portfolio (top minus bottom ranked stocks) decreased by -7.2%, as the bottom-ranked stocks significantly outperformed the top-ranked securities. Over the past five years, the top decile AlphaRank portfolio has gained approximately 230%, while the bottom-ranked portfolio has risen less than 100%.

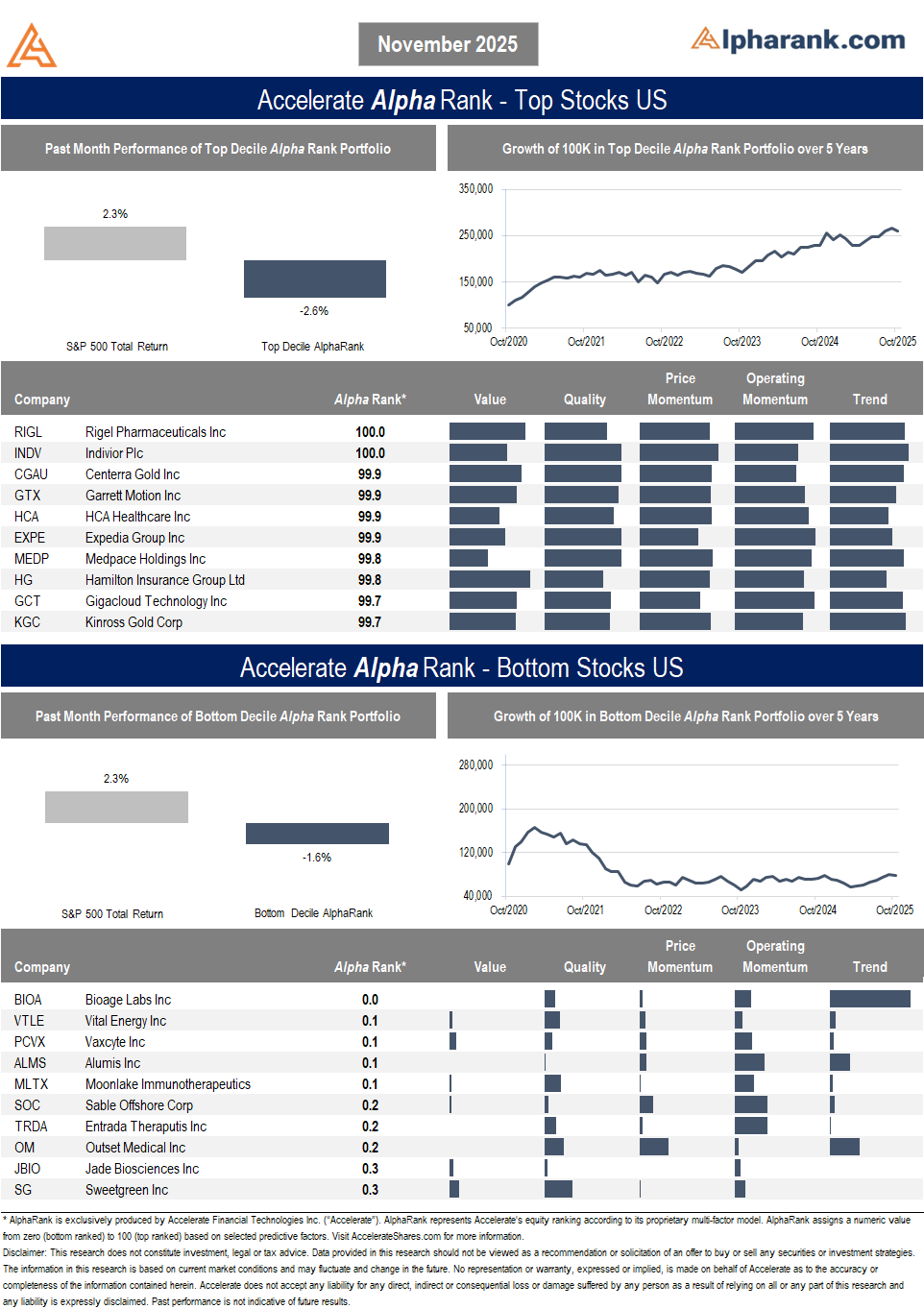

- In the U.S., the top-decile-ranked equities decline by -2.6%, underperforming the S&P 500’s 2.3% return. Meanwhile, the bottom-ranked stocks fell by -1.6%, resulting in a -1.0% return for the top decile minus the bottom decile long-short portfolio. Over the past five years, the top-ranked U.S. equities have gained more than 150%, while the bottom-ranked portfolio has declined by more than -20%.

AlphaRank Top Stocks represents Accelerate’s predictive equity ranking powered by proven drivers of return. Stocks with the highest AlphaRank are expected to outperform, while stocks with the lowest AlphaRank are anticipated to underperform. AlphaRank assigns a numeric value to each security, ranging from 0 (bottom-ranked) to 100 (top-ranked), based on selected predictive factors. All Canadian and U.S. stocks priced above $1.50 per share and with a market capitalization exceeding $100 million are evaluated. In both the Accelerate Absolute Return Fund (TSX: HDGE) and the Accelerate Canadian Long Short Equity Fund (TSX: ATSX), Accelerate funds may be long many top-ranked stocks and short many bottom-ranked stocks. See AccelerateShares.com for more information.