March 4, 2026 – Portfolio management pioneer and trailblazer of the endowment-style asset allocation approach, David Swensen, once referred to private equity as “a superior form of capitalism.”

His praise of private equity was based on the notion that aligning ownership and control within the same group led to superior economic performance. In private equity, the investors and managers hold controlling equity stakes and maintain full operational control, with fully aligned incentives. In contrast, public companies have disparate ownership, which can lead to the principal-agent problem, in which the corporate executives who operate the business may have different motives than the organization’s shareholders.

Private equity, as we know it today, grew out of the leveraged buyout (LBO) model that emerged in the 1970s. One of the key architects of the LBO model was Jerome Kohlberg Jr., who later co-founded Kohlberg Kravis Roberts with Henry Kravis and George Roberts in 1976.

Early LBO deals focused on family-owned businesses, corporate carve-outs, and underperforming divisions. Debt financing (putting the “L” in LBO), which accounted for the vast majority of the financing required for these transactions, was primarily provided by banks and insurance companies.

Once the business model established a track record of success, leveraged buyout activity boomed in the 1980s with the emergence of the high-yield (junk) bond market, pioneered by Michael Milken at Drexel Burnham Lambert.

After the leveraged buyout boom ended when Drexel Burnham collapsed in 1990 and the junk bond market seized up, LBO firms began pivoting to operational improvements rather than focusing solely on low valuations and substantial amounts of leverage.

By the 2000s, the asset class became popular with institutional investors, aided by the success of Swensen’s endowment model, and was rebranded as private equity. Moreover, the industry’s reliance on the high-yield bond market to finance leveraged buyouts transitioned to the broadly syndicated loan and private credit markets.

Private equity now manages trillions of dollars, and the traditional LBO is just one piece of a much larger alternative asset ecosystem. The asset class now accounts for a material slice of the typical institutional investment portfolio.

As the asset class evolved over the past two decades, private equity software buyouts became increasingly popular. Software buyouts grew from just 2% of PE deals in 2000 to nearly 30% of buyouts today.

From a fundamental perspective, software was the perfect business model for private equity buyouts for several reasons:

- Recurring revenue (Software-as-a-service, or SaaS, subscriptions)

- High gross margins

- Low capital intensity

- Predictable cash flow, which supports leverage

- Fragmented markets, supporting roll-up playbooks

The old model of acquiring cheap, asset-heavy industrial businesses was replaced with buying asset-light SaaS businesses with predictable recurring revenue. Moreover, credit markets were drawn to the software industry because its consistent and predictable cash flows made debt financing attractive. In fact, private credit firm Blue Owl recently revealed that of the 300+ software buyouts that it has provided debt financing for since its inception, only one has defaulted.

Private equity and software seemed a match made in heaven. The union worked wonders for the past couple of decades, with software private equity firms showcasing industry-leading fund returns. However, recently, cracks have started to form in its foundation due to the emergence of artificial intelligence.

The thesis that AI will kill software is one of the central debates in tech and investing right now. The bearish thesis is based on the potential of barriers to entry collapsing, commoditization, and the erosion of traditional SaaS moats.

For decades, software development required large engineering teams, long development cycles, and meaningful capital investment. Now, AI dramatically changes that equation. Code generation tools allow a single engineer, to quickly build applications that previously required entire teams. Development cycles have potentially compressed from months to mere hours. OpenAI’s Codex and Anthropic’s Claude Code have progressed at lightning speed and have become so good that top software developers admit to no longer needing to code themselves, instead using prompts with AI coding agents.

When the cost of production collapses, barriers to entry collapse with it. If anyone can “vibe-code” an app quickly, competition proliferates and margins inevitably compress.

Another argument is that AI could replace the interface layer that many software companies rely upon. Much of enterprise software exists to provide users with an interface to interact with data or workflows. AI agents could remove the need for these interfaces altogether. Instead of navigating dashboards, a user could just ask an AI agent to perform a task.

Some market prognosticators argue that AI agents could eliminate entire categories of software. Many enterprise tools exist primarily to coordinate tasks between people. For example, customer support systems organize ticket handling and project management platforms coordinate tasks across teams. AI agents could potentially automate many of these functions directly.

The growth of AI utilization may also undermine the traditional SaaS per-seat pricing model. If AI dramatically increases worker productivity, organizations may require fewer employees to accomplish the same output. See Block’s recent announcement to cut 40% of its workforce, representing 4,000 jobs. If one employee supported by a team of AI agents can perform the work of several people, the number of software licenses required could fall accordingly.

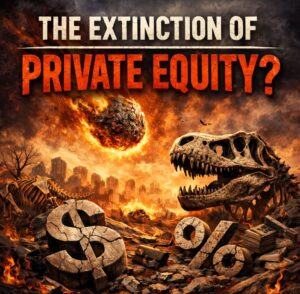

Given the rapidly emerging risks and heightened fear that AI will displace SaaS applications, any security related to this theme has been punished by the market. Software equities have fallen by more than -30% over the past four months.

Furthermore, given the software-heavy contingent within private equity portfolios, with some PE funds 100% exposed to software investments, investors can assume that PE fund returns are deeply in the red (if they were marked-to-market). Secondary prices of private credit funds, which have approximately 20% software loan exposure on average, have tumbled, dropping double-digits over the past several months as software concerns mount, despite their fundamental loan performance remaining somewhat robust.

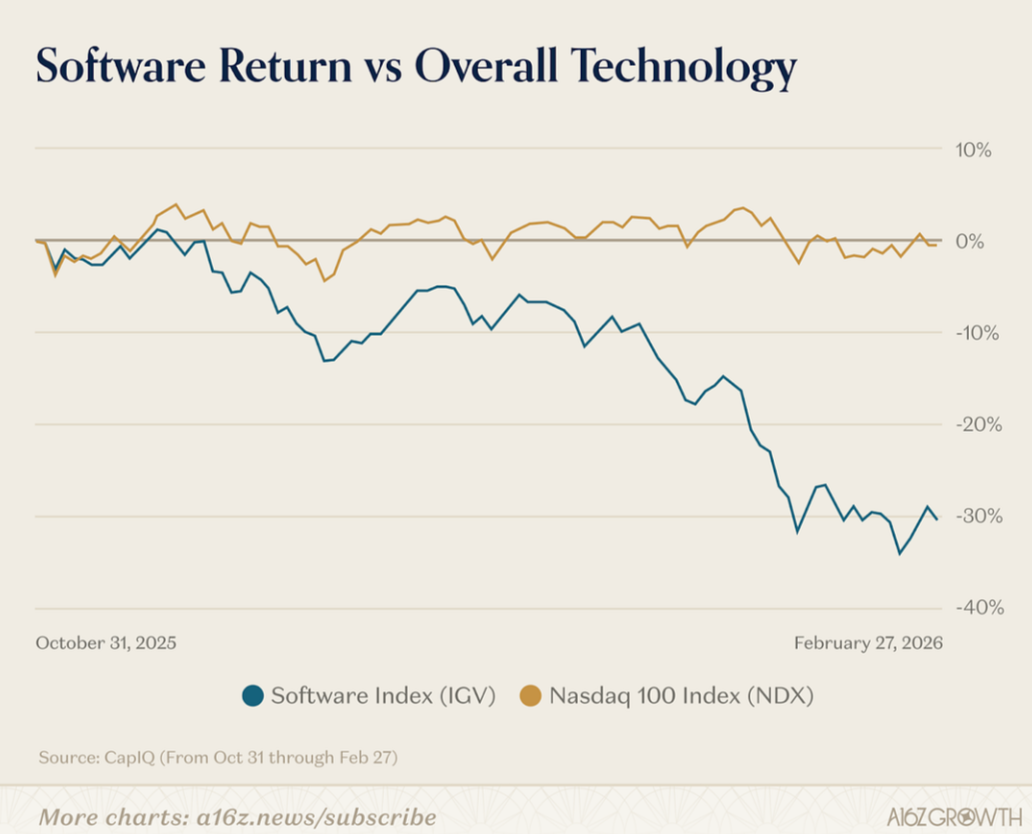

These two bearish dynamics make for a tough slog for the large alternative investment platforms, whose shares have plummeted this year as the AI killing software thesis proliferates. Given the sheer size and breadth of the exposure, the destruction of the software business model could represent an extinction-level event for the private equity industry.

That said, there is a valid counter to the bear case for software. Fundamentally, private-equity owned software companies are still growing revenue and EBITDA by double-digits on average as of the fourth quarter. Currently, the bearish thesis is only a narrative, as it has yet to materialize in SaaS company results.

Whenever the cost of software development has fallen in the past, the total amount of software in the world has increased rather than decreased. Lower development costs historically expanded demand. The emergence of website builders did not reduce the number of websites – it caused an explosion of them. AI could produce the same effect for enterprise software. As building applications becomes cheaper and easier, organizations may create thousands of customized tools tailored to their specific workflows. The result could be dramatically greater overall demand for software. Moreover, any technological leap, such as the invention of the internal combustion engine, has led to far more jobs being created than are lost. A historical technological innovation such as AI destroying jobs would run counter to any previous productivity-enhancing revolution.

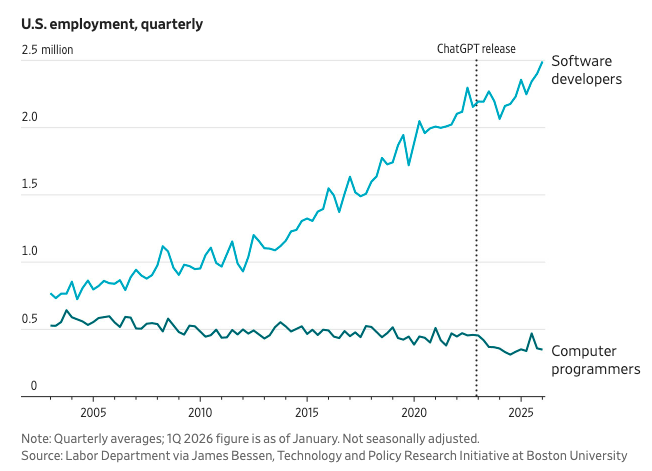

One datapoint that refutes the challenge to employment posed by AI: the ranks of software developers are up 5% in January from a year earlier. The number of software development jobs has increased by several hundred thousand since ChatGPT was released. Also, business spending on software leapt 11% in Q4 from a year earlier, the fastest in nearly three years.

Another counterargument focuses on distribution and trust. Software companies are not merely collections of code. They also possess customer relationships, enterprise salesforces, support organizations, and global infrastructure. Even if someone can replicate the functionality of a platform like Salesforce, they must still convince enterprises to trust it with mission-critical data and workflows. Large organizations value reliability, security, compliance, and long-term vendor stability. These attributes create advantages for incumbents that are not easily replicated by small teams and startups building AI-assisted products.

The typical SaaS company spends 10-20% of its revenue on research and development and 30-50% on sales and marketing. Getting an enterprise to buy your software solution is not so easy, and vibecoded apps won’t magically find their way into large organizations. Mission-critical software is often associated with extremely high switching costs.

Finally, AI may ultimately function as a feature rather than a replacement. Many existing SaaS platforms are already embedding AI capabilities directly into their products. As Nvidia’s Jensen Huang recently questioned, “Would you use a hammer or invent a new hammer?” Why waste your time rebuilding great software that works perfectly when you could be utilizing AI to dramatically grow your business?

In this bull case, AI becomes the next technological wave within software rather than a substitute for software itself.

The most likely outcome lies somewhere in the middle. AI will likely destroy some weak software companies that rely on narrow features and lack durable advantages, a mission-critical position, or proprietary data. SaaS businesses with dominant platforms, proprietary data, large customer bases, and deep customer integrations may become even stronger as they incorporate AI capabilities into their ecosystems.

Ergo, AI may make many software companies much more valuable.

The private equity industry seems to agree, as it continues to double-down on leveraged buyouts even as the perceived risk of AI disruption to its investments proliferates.

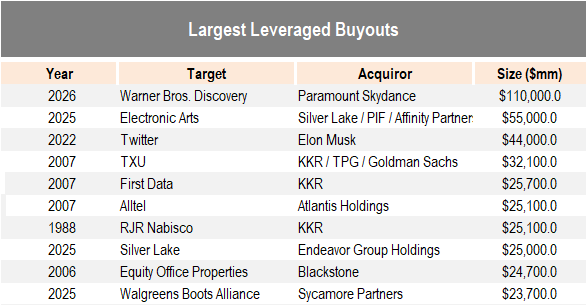

For example, last September, a consortium of private capital providers, including PIF, Silver Lake, and Affinity Partners, announced the largest LBO of all time with the $55 billion buyout of video game company Electronic Arts. Recently, AI tools such as Google’s Genie 3 have released models that allow users to generate playable video game environments from text prompts or images, potentially threatening the viability of video game studios.

Furthermore, just over two months later, Paramount Skydance announced a far larger LBO – the $110 billion buyout of Warner Bros Discovery. The deal is double the size of the previous record largest LBO announced mere months prior. As for the disruption risk there, some of the AI-generated movies that users create through ByteDance’s Seedance 2.0 model have some Hollywood executives in a panic.

Source: Accelerate

It is not just software that faces AI disruption risk, but video games and movies, among a myriad of other industries. In any event, these fears have not slowed down the private equity industry. In February, six buyouts of U.S. public companies were announced, totalling more than $17 billion in enterprise value.

Moreover, software-focused private equity firm Thoma Bravo closed the $12.3 billion buyout of human capital management technology company Dayforce last month, after closing its $1.4 billion acquisition of SaaS company PROS Holdings in December and the $2.0 billion LBO of customer experience automation company Verint in November. The private equity industry continues to be active, seemingly unabated by the fears expressed in the public markets.

While the growls of the software bears seem to grow louder each day, thus far, it is more bark than bite. The private equity titans and LBO mavens are staying busy acquiring SaaS, movie, and video game businesses despite the looming threat of AI disruption. Perhaps they are betting on the bull case – that ultimately, AI will be a growth-enabler, not a destroyer, of these industries. As is often the case, time will tell who is right.

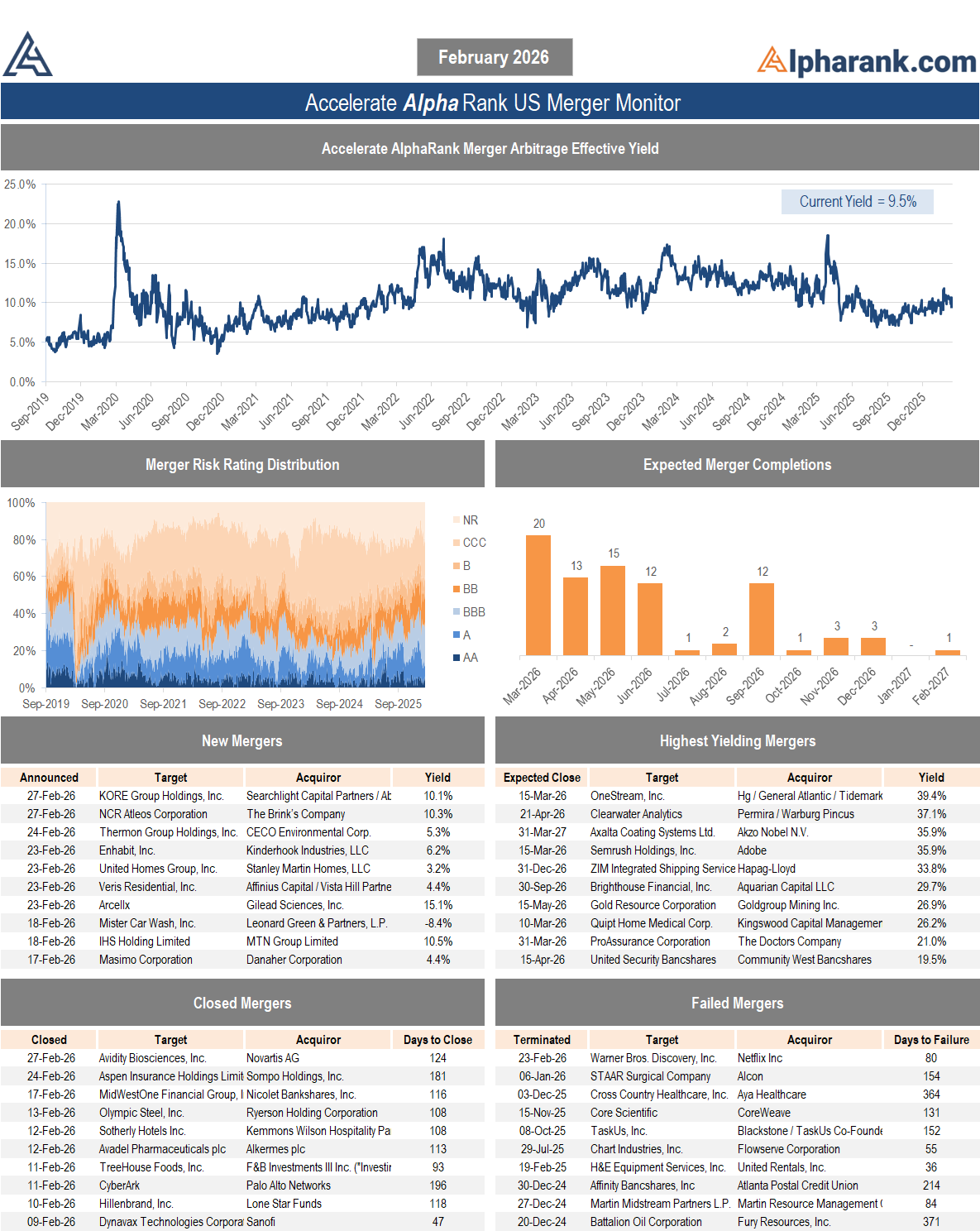

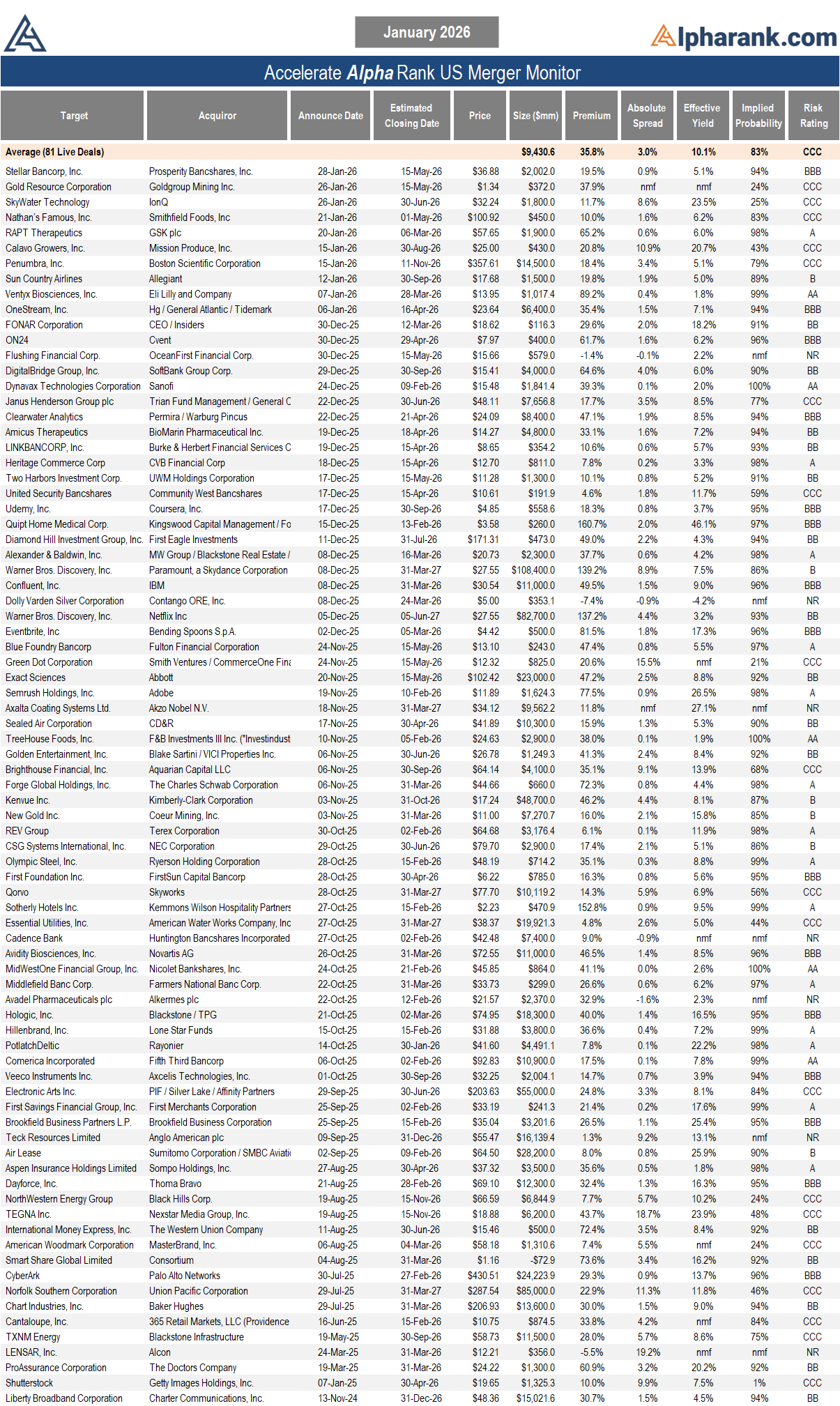

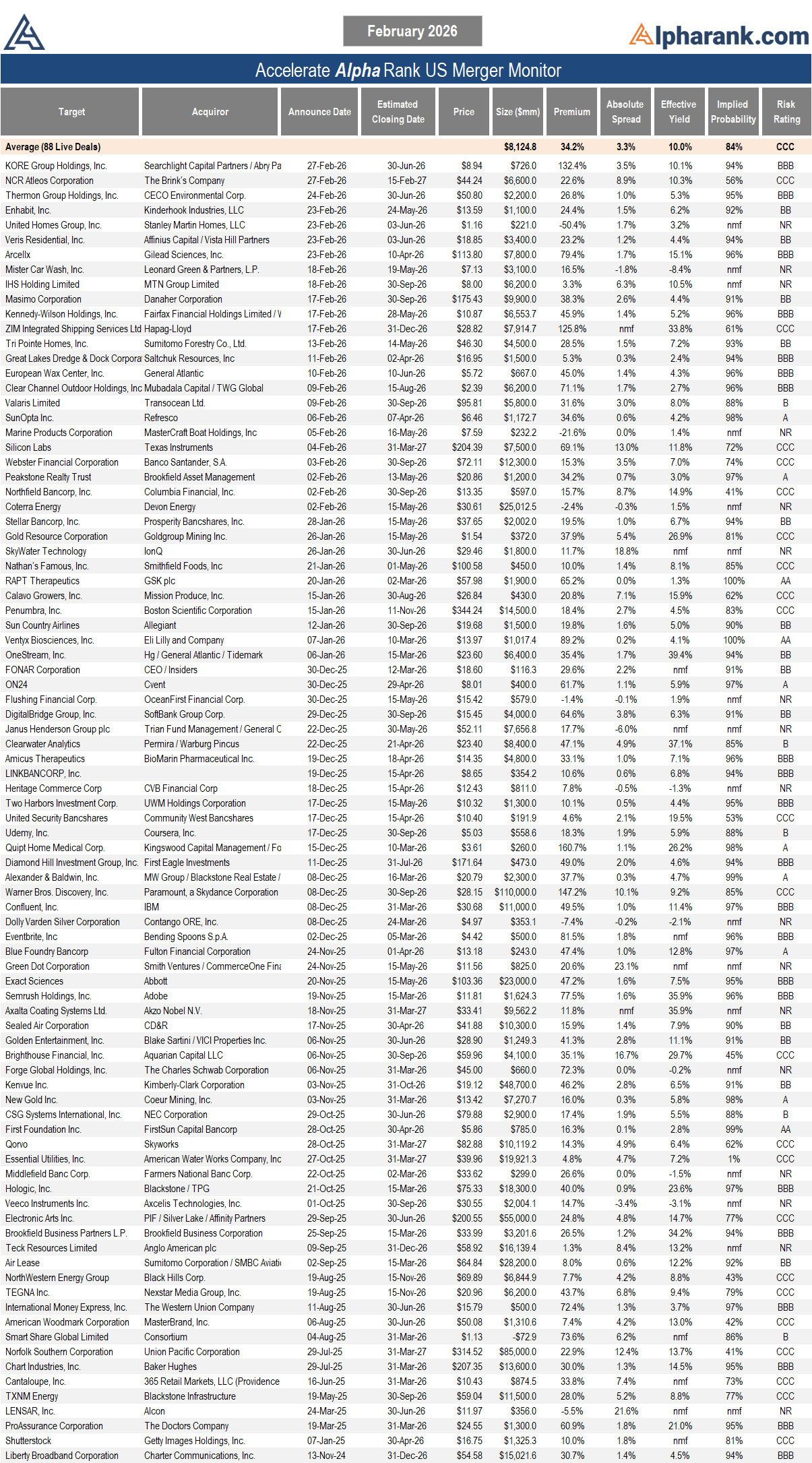

The AlphaRank.com Merger Monitor below represents Accelerate’s proprietary analytics database on all announced liquid U.S. mergers. The AlphaRank Merger Arbitrage Effective Yield represents the average annualized returns of all outstanding merger arbitrage spreads and is typically viewed as an alternative to fixed income yield.

Each individual merger is assigned a risk rating:

- AA – a merger arbitrage rated ‘AA’ has the highest rating assigned by AlphaRank. The merger has the highest probability of closing.

- A – a merger arbitrage rated ‘A’ differs from the highest-rated mergers only by a small degree. The merger has a very high probability of closing.

- BBB – a merger arbitrage rated ‘BBB’ is of investment grade and has a high probability of closing.

- BB – a merger arbitrage rated ‘BB’ is somewhat speculative in nature and has a greater than 90% probability of closing.

- B – a merger arbitrage rated ‘B’ is speculative in nature and has a greater than 85% probability of closing.

- CCC – a merger arbitrage rated ‘CCC’ is very speculative in nature. The merger is subject to certain conditions that may not be satisfied.

- NR – a merger-rated NR is trading either at a premium to the implied consideration or a discount to the unaffected price.

The AlphaRank merger analytics database is utilized in running the Accelerate Arbitrage Fund (TSX: ARB), which may have positions in some of the securities mentioned.

* AlphaRank is exclusively produced by Accelerate Financial Technologies Inc. (“Accelerate”). Visit Alpharank.com for more information. Disclaimer: This research does not constitute investment, legal or tax advice. Data provided in this research should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this research is based on current market conditions and may fluctuate and change in the future. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Accelerate may have positions in securities mentioned. Past performance is not indicative of future results.