May 25, 2026 – “The only function of economic forecasting is to make astrology look respectable,” quipped legendary economist John Kenneth Galbraith.

Galbraith’s line is a sharp jab aimed at the difficulty and false precision inherent to economic forecasts. He compares economic forecasting to astrology because both can appear sophisticated, but both are often unreliable when used to predict specific future outcomes.

Nonetheless, even astrology can be useful, particularly for its entertainment value.

Accordingly, while economic forecasts have their own entertainment value (many consumers of analyst reports view them as marketing material), there is a valuable signal amid the noise.

Sell-side analyst reports dominate investors’ email inboxes. It is estimated that approximately 3,000 to 6,000 sell-side research notes are produced each business day across major institutional platforms, with volume highest during earnings season. These materials include full reports, earnings previews and reviews, estimate-change notes, initiations, upgrades and downgrades, industry notes, and quick morning comments.

As expected, most of the information contained within the thousands of analyst reports released daily does not add value. Primarily, these reports summarize recent news and events, and can be firmly placed in the “entertainment value” bucket.

However, amid all the noise in analyst reports is a very useful signal for investors: earnings revisions.

Earnings revisions measure whether the analyst’s forward consensus earnings expectations are moving up or down. Common implementations include the percentage change in consensus EPS estimates over the past one to three months, the breadth of revisions (the share of analysts raising versus cutting estimates), and the magnitude of revisions scaled by price, earnings, or forecast dispersion. Multi-factor versions often combine forecast revision magnitude, breadth, earnings surprise, and sometimes analyst recommendation changes.

Earnings revisions are one of the better-supported “information momentum” or “operating momentum” signals in quantitative equity research. The basic finding is that stocks with improving analyst earnings expectations tend to outperform stocks with deteriorating expectations, even after controlling for other effects such as price momentum, value, and size.

The research rationale is straightforward. Analyst estimate changes are public signals that incorporate new company information, but stock prices appear to adjust gradually rather than instantly. This dynamic connects earnings revisions to the broader literature on post-earnings-announcement drift, where stocks continue to move in the direction of earnings news for weeks or months after the announcement.

The earnings revision factor (often called the analyst forecast revision factor or post-earnings forecast revision drift) is one of the most robust and heavily researched fundamental anomalies in quantitative finance. The factor measures the tendency of a stock’s price to drift in the direction of recent revisions to sell-side analyst earnings expectations.

The phenomenon of stocks drifting higher or lower after analyst revisions was first formally documented in 1979 by Givoly and Lakonishok in their seminal paper, “The Information Content of Financial Analysts’ Forecasts of Earnings: Some Evidence on Semi-Strong Efficiency“, published in the Journal of Accounting and Economics. In the analysis,Givoly and Lakonishok found that revisions in consensus analyst earnings forecasts contain highly significant informational value. Notably, the authors found that the market does not absorb analyst forecast revisions immediately. Instead, stock prices continue to move in the direction of the revision for months after the revision occurs: “Holding a stock during four months surrounding an upward revision of over 5% results, on average, in an abnormal return of 4.7%, representing a 195% improvement over a buy-and-hold policy.”

In 1996, Chan, Jegadeesh, and Lakonishok published the paper, “Momentum Strategies“. In the study, they showed that analysts revise their expectations gradually rather than all at once. Consequently, a portfolio sorted by consensus earnings revisions yielded highly predictable, statistically significant returns over a 6-month time horizon, entirely independent of past price performance: “Ranking stocks by a moving average of past revisions in consensus estimates of earnings produces spreads of 7.7 percent over the next six months.”

The 2004 paper “Analyzing the Analysts: When Do Recommendations Add Value?” by Jegadeesh, Kim, Krische, and Lee, is a classic study in quantitative and behavioural finance. The authors concluded that analysts do add genuine value to the market, but not because of their absolute stock-picking levels. In contrast, they found that the quarterly change in analyst consensus recommendations is an incredibly powerful and robust predictor of future returns: “The explanatory power of the change in the consensus analyst recommendation is more robust than that of the level of the recommendation. Changes in recommendations over the prior quarter predict future returns when used separately and when used in conjunction with other predictive signals.”

The primary objective of isolating the earnings revision factor in quantitative portfolios is to exploit the underreaction of market participants. Across the decades of literature, the performance dichotomy between positive and negative revision securities remains remarkably persistent:

- Stocks that experience upward consensus earnings revisions consistently generate positive abnormal returns (alpha) over the subsequent 3 to 12 months. Because investors generally suffer from an anchoring bias, they fail to fully price in how good the positive revision actually is. As a result, the stock continues to experience a slow, upward price drift as the market gradually accepts the higher earnings reality.

- Stocks that experience downward consensus earnings revisions systematically underperform the market benchmark. Quantitative research notes that a negative revision is rarely an isolated event. When there is one bad forecast, more tend to follow. Management and analysts often release bad news incrementally. Moreover, investors tend to anchor to past higher prices and are slow to sell, leading to a long, grinding downward drift in the stock price.

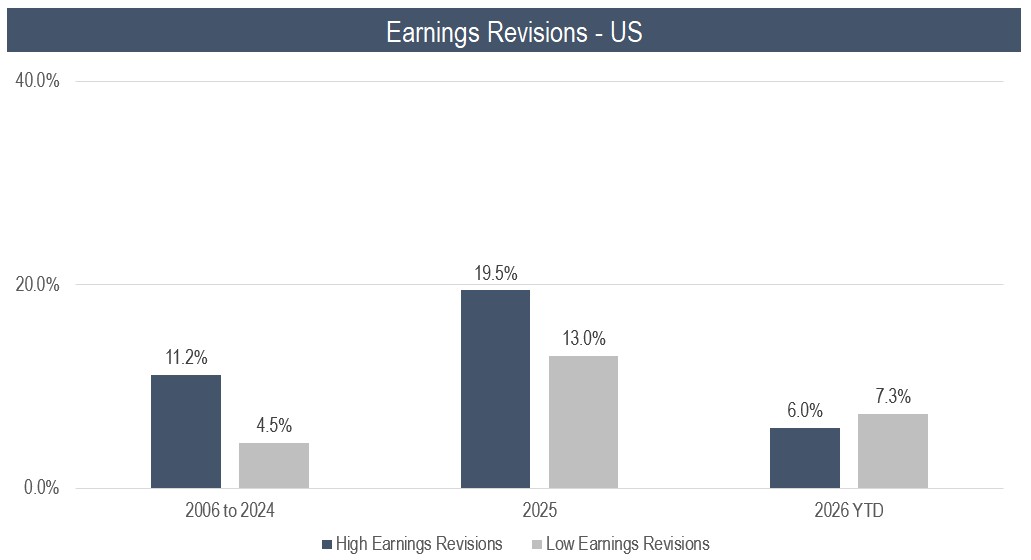

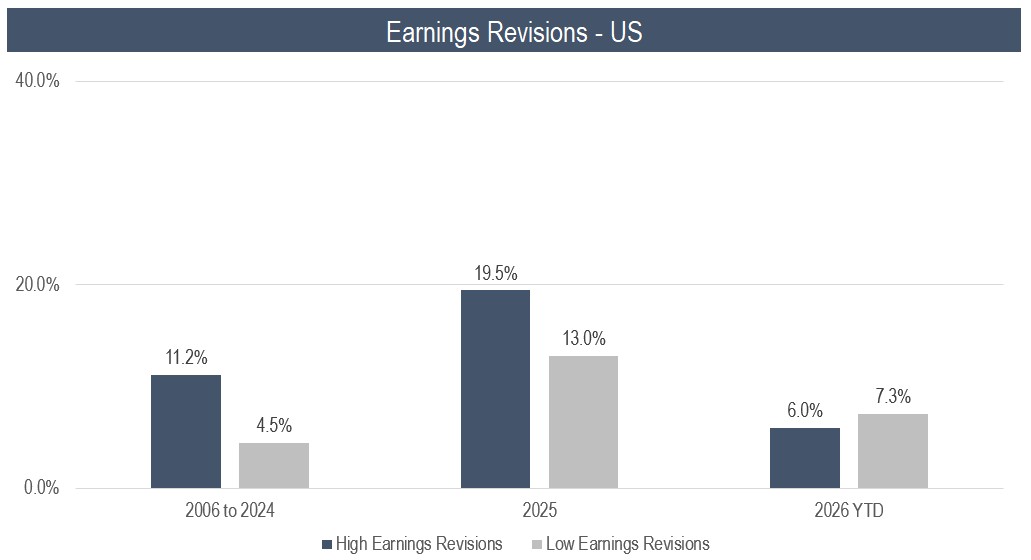

Accelerate backtested the earnings revision factor going back to 2006, grouping portfolios of stocks into quintiles based on the levels of their earnings revisions. The portfolios were rebalanced on a monthly basis.

In the U.S. equity market, the top quintile of stocks with the highest positive earnings revisions generated an 11.2% annualized return. In comparison, the bottom quintile (those generally experiencing negative earnings revisions) produced a 4.5% annualized return. The top quintile of stocks with positive earnings revisions outperformed the bottom by 6.7% per year. Last year, the performance differential was 6.5%. However, the factor does not work every year. Thus far in 2026, the top quintile of earnings revisions has underperformed the bottom quintile by -1.3%.

The data presents similar results for Canadian equities. Since 2006, the top quintile of stocks in Canada that have experienced the highest positive earnings revisions generated a 12.4% annualized return, while the bottom quintile (those generally experiencing negative earnings revisions) produced a 6.0% annualized return. The top quintile of stocks with positive earnings revisions outperformed the bottom by 4.8% in 2025. Year-to-date, the top quintile of earnings revisions is outperforming the bottom by 5.6%.

Accordingly, from a portfolio manager’s standpoint, the data show that earnings revision factor investing, particularly from a long-short perspective, can be an attractive investment strategy. Earnings revisions work because analysts update earnings expectations gradually and investors underreact to changes in forward fundamentals. That said, realistically, earnings revisions can work best as part of a broader composite signal. The best use of the earnings revision factor is not as a standalone “buy upgraded stocks” rule, but as a component of a broader multi-factor model that combines revisions with earnings quality, valuation, price momentum, and others. To help facilitate idea generation, we highlight one top-decile stock that is forecasted to outperform and one bottom-decile stock that is predicted to underperform based on Accelerate’s multi-factor composite model in this month’s AlphaRank Top Stocks.

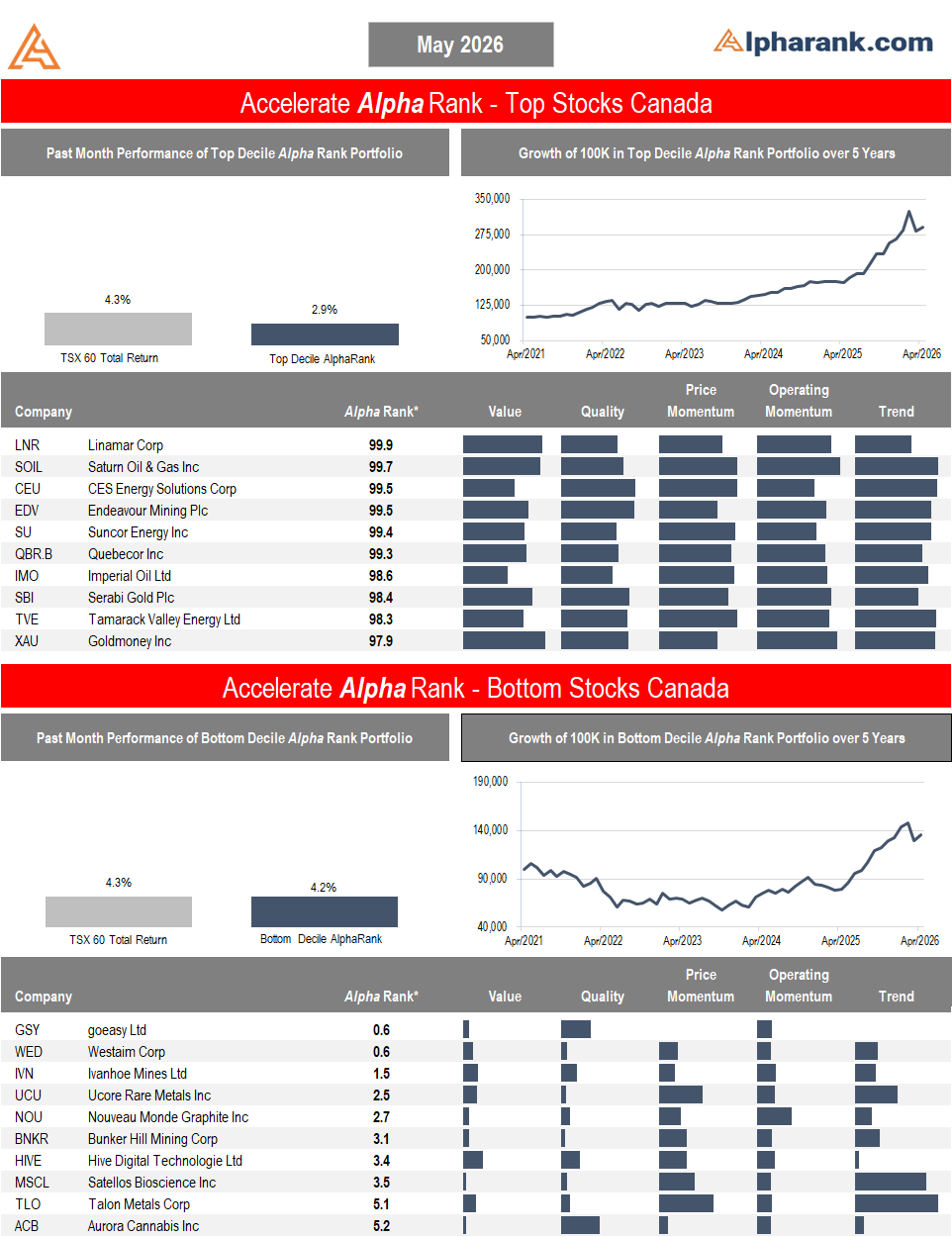

OUTPERFORM: Monarch Casino & Resort Inc (NASDAQ: MCRI) is a small-cap regional casino and hotel operator. The business is simpler than most gaming companies. It is not a sprawling national operator. It owns and operates two high-quality destination casino resorts, earns revenue from casino gaming, food and beverage, and hotel operations, and emphasizes hands-on management, customer service, and cost efficiency. Monarch is a high-quality, conservatively financed regional gaming compounder. Trading at a below-market multiple of 10x EBITDA, with a return on capital of 35.3%, MCRI presents a compelling combination of value and quality. Moreover, a recent quarterly earnings beat adds to the bull case. With positive share price momentum, along with an AlphaRank score of 100/100, we expect MCRI shares to continue to outperform. Disclosure: Long MCRI in the Accelerate Absolute Return Fund (TSX: HDGE).

UNDERPERFORM: Bakkt Inc (NYSE: BKKT) is a digital-asset infrastructure company. It has been through a major strategic transition. Its legacy loyalty business is effectively gone from continuing operations, and the business is now heavily dependent on crypto transaction activity. BKKT is operating at a loss and is experiencing a significant revenue decline. The balance sheet has been supported by continued equity issuance and shareholder dilution. BKKT is a loss-making, highly volatile crypto infrastructure company with collapsing revenue after the loss of major clients, thin gross economics, ongoing operating cash burn, heavy reliance on equity financing, meaningful dilution risk, and going-concern-style disclosure language around the need to materially expand revenue. With an AlphaRank score of 0.1/100, we expect BKKT shares to continue to underperform.

The AlphaRank Top and Bottom stock portfolios exhibited challenged relative performance last month:

- In Canada, the top-ranked AlphaRank portfolio of stocks increased by 2.9%, underperforming the benchmark’s 4.3% gain, while the bottom-ranked portfolio of Canadian equities rose by 4.2%. The long-short portfolio (top minus bottom-ranked stocks) dropped by -1.3%, as the top-ranked stocks underperformed the bottom-ranked securities. Over the past five years, the top decile AlphaRank portfolio has gained 190%, while the bottom-ranked portfolio has risen by 35%.

- In the U.S., the top-decile-ranked equities rose by 8.3%, underperforming the S&P 500’s 10.5% return. Meanwhile, the bottom-ranked stocks surged by 15.2%, resulting in a -6.9% return for the top decile minus the bottom decile long-short portfolio. Over the past five years, the top-ranked U.S. equities have gained nearly 100%, while the bottom-ranked portfolio has declined by -43%.

AlphaRank Top Stocks represents Accelerate’s predictive equity ranking powered by proven drivers of return. Stocks with the highest AlphaRank are projected to outperform, while stocks with the lowest AlphaRank are anticipated to underperform. AlphaRank assigns a numeric value to each security, ranging from 0 (bottom-ranked) to 100 (top-ranked), based on selected predictive factors. All Canadian and U.S. stocks priced above $1.50 per share and with a market capitalization exceeding $100 million are evaluated. In both the Accelerate Absolute Return Fund (TSX: HDGE) and the Accelerate Canadian Long Short Equity Fund (TSX: ATSX), Accelerate funds may be long many top-ranked stocks and short many bottom-ranked stocks. See AccelerateShares.com for more information.