May 17, 2026 – In 1960, an English rock band formed in Liverpool. They called themselves The Beatles.

Within a few years, The Beatles became a global phenomenon. In fact, there was a name for this explosion of mass hysteria around the Beatles – Beatlemania.

In the early Beatlemania years, the noise around the band reached absurd levels: screaming fans, police escorts, media frenzy, and chaotic concerts where the music itself was sometimes barely audible. Not to mention the bad haircuts and the resulting moral panic among older generations.

Despite all of the exogenous reasons to dislike The Beatles, they were exceptionally successful for one reason: people loved their music. Ultimately, the fundamentals of their music outweighed all the noise and controversy surrounding their popularity.

Currently, a similar dynamic is playing out in the stock market.

The list of reasons to be bearish on the equity market is lengthy:

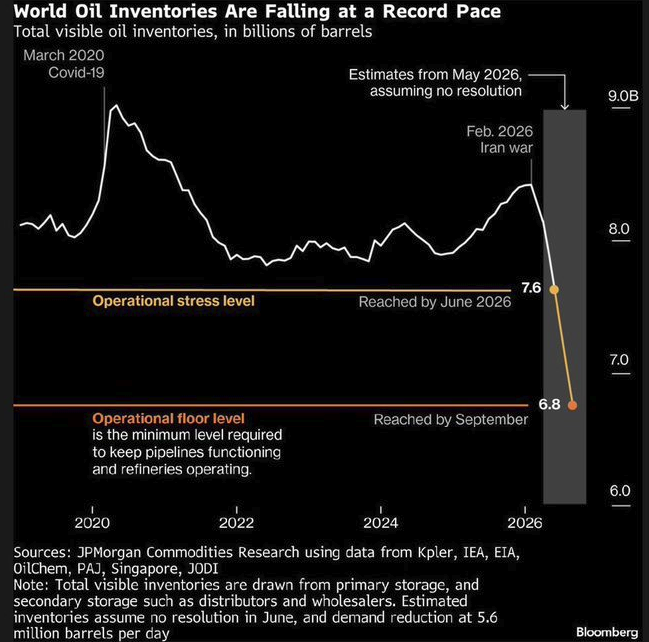

1. War – The conflict in Iran has created a myriad of threats to the global economy. Disruption around the Strait of Hormuz has caused oil and LNG prices to surge globally. Supply chains have been battered. Despite constant talk of a ceasefire, the disruption in the Strait continues, and it remains effectively closed to the transportation of oil. As a result, global oil inventories have fallen at a record pace. Since the war began, the world has lost about 1 billion barrels of oil inventory. The rapid decline in inventories is accelerating, as oil markets are losing 100 million barrels every week the Strait of Hormuz remains shut.

As global oil inventories deplete, the risks to the global economy compound.

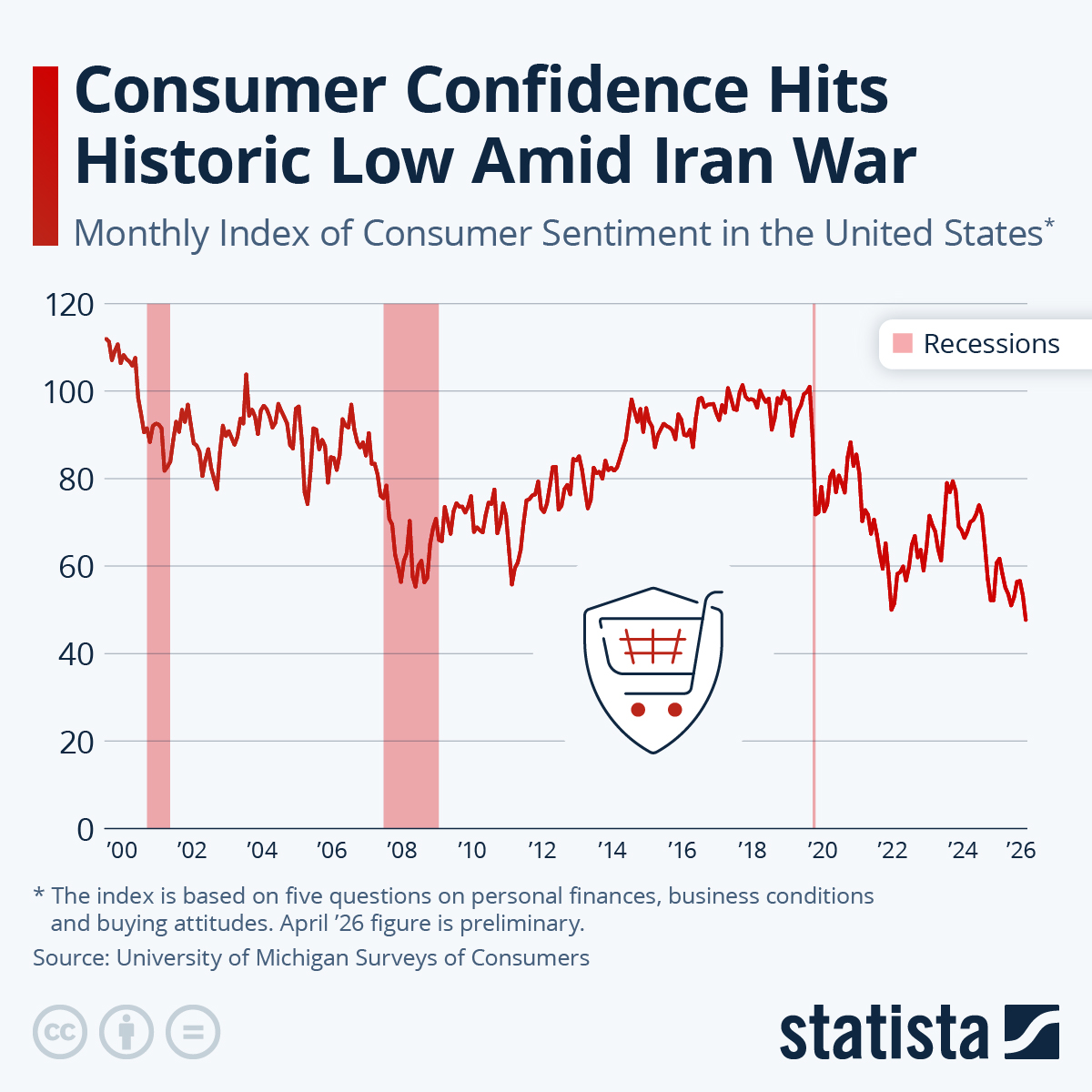

2. Geopolitical Chaos – Last year’s trade war continues to reverberate through the global economy. Certain supply chains remain battered, and uncertainty around global commerce has surged. Tariffs, sanctions, export controls, and geopolitical blocs are reducing efficiency in global trade and investment. As a result, consumer confidence has hit record lows.

Given that consumers and their personal consumption expenditures account for nearly 70% of the U.S. economy, plummeting consumer confidence, which can lead to reduced consumer spending, presents a major risk to the economy.

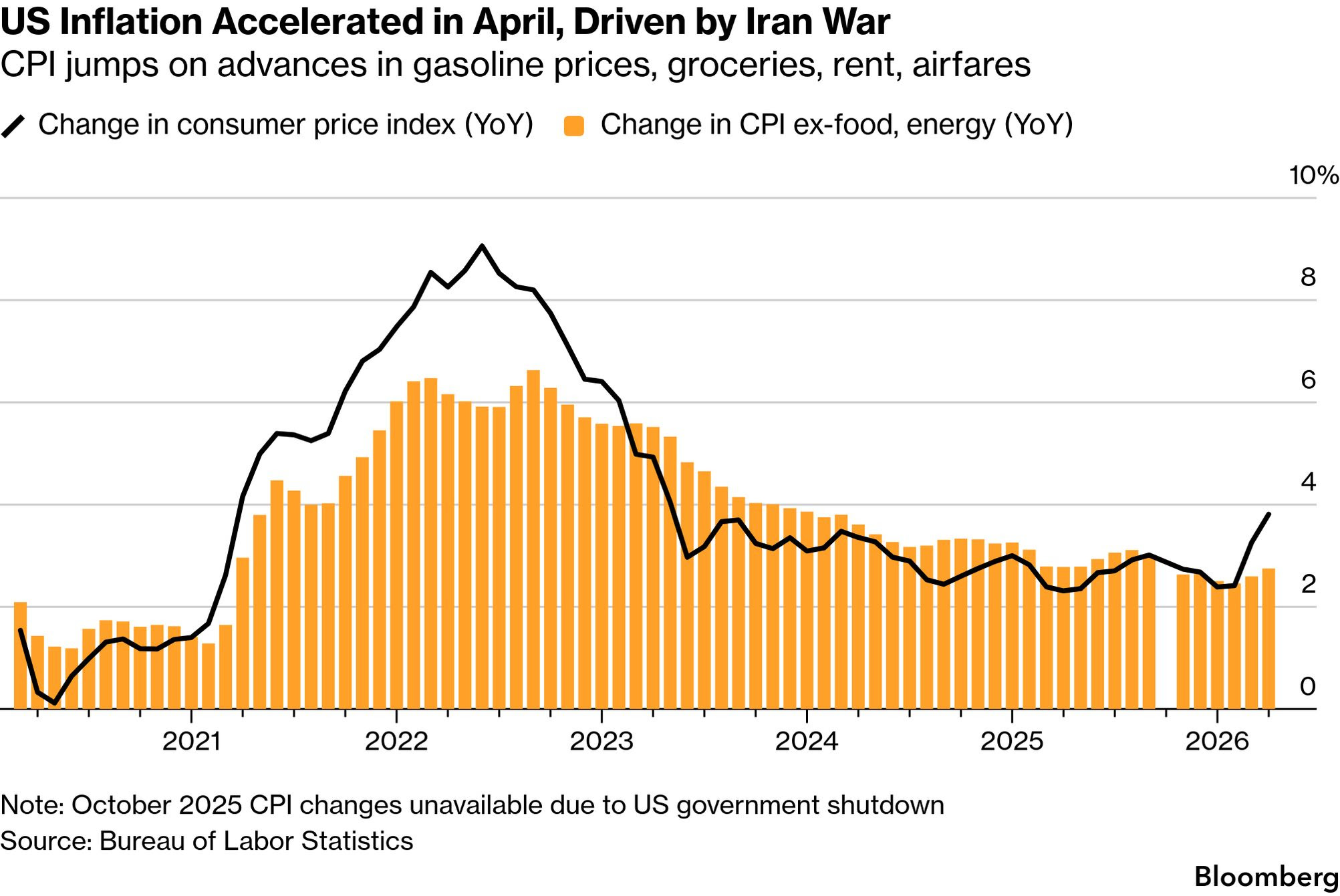

3. Surging Inflation – Legendary economist Milton Friedman frequently compared inflation to alcoholism: the good effects (temporary spending power) come first, and the devastating effects come later. When governments or central banks stimulate the economy too much, the early effects can look positive: more spending, easier credit, rising asset prices, stronger employment, and a sense of prosperity. However, later come the costs: higher prices, eroded purchasing power, distorted investment decisions, and eventually tighter monetary policy.

The U.S consumer price index recently hit 3.8%, representing an accelerated pace of inflation that has remained consistently above its 2% target for five years straight.

Inflation is like a hangover from yesterday’s stimulus: the party comes first, the pain comes later. The risks surrounding the potential emergence of a painful stagflationary environment are rising.

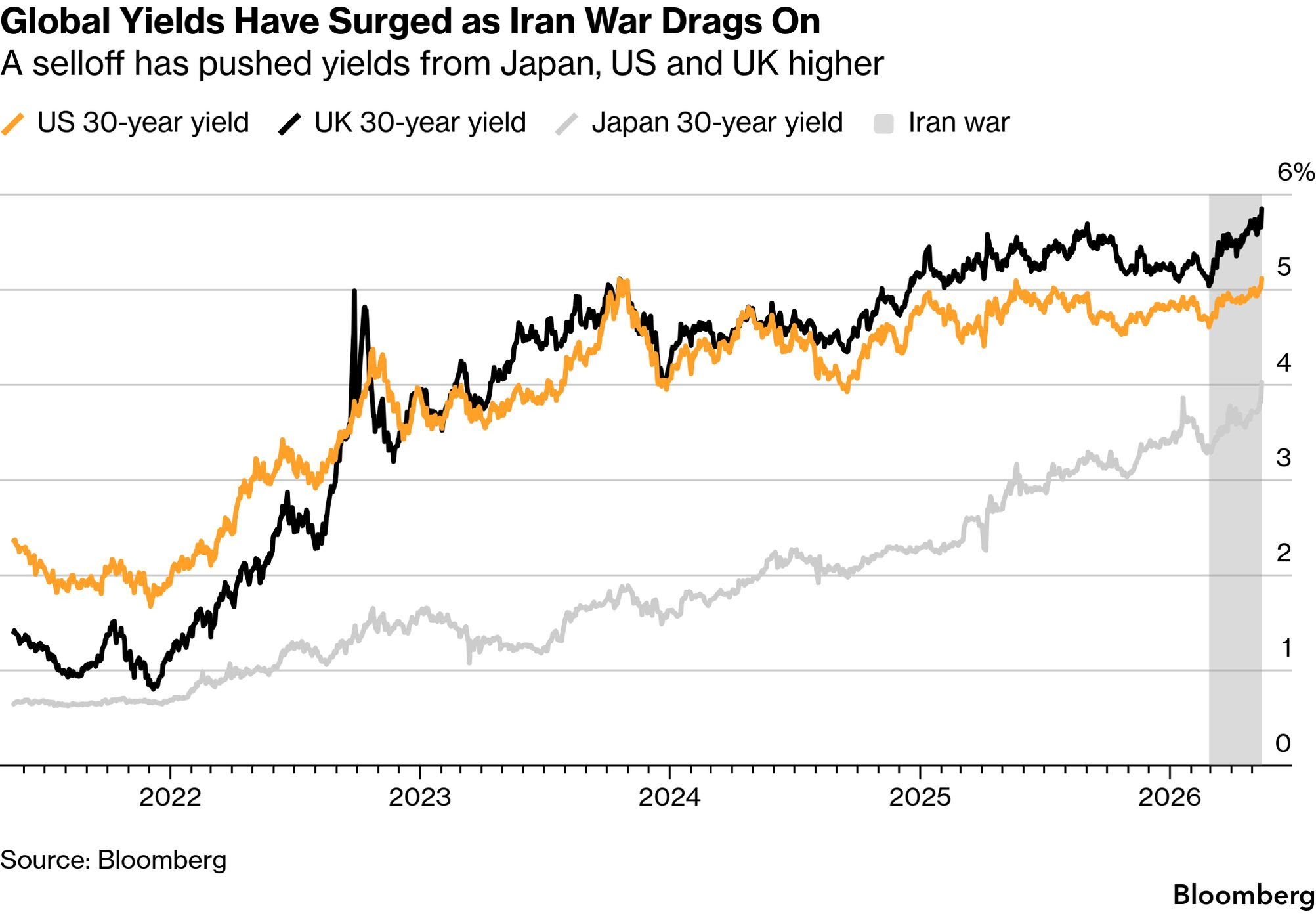

4. Rising Long-Term Bond Yields – Rising bond yields can hurt the economy and the stock market through several channels:

- They raise borrowing costs. Mortgages, car loans, corporate debt, and government financing become more expensive, which slows spending, investment, hiring, and housing activity.

- They reduce stock valuations. Higher yields increase the discount rate applied to future earnings, making long-duration growth stocks particularly vulnerable.

- They pressure corporate profits. Companies face higher interest expense, weaker demand, and potentially lower margins.

- They tighten financial conditions. Higher yields can strengthen the dollar, weigh on commodities and emerging markets, and make credit harder to access.

Rising yields are a drag on the economy and valuation multiples: they make money more expensive, future earnings less valuable, and bonds more competitive with stocks.

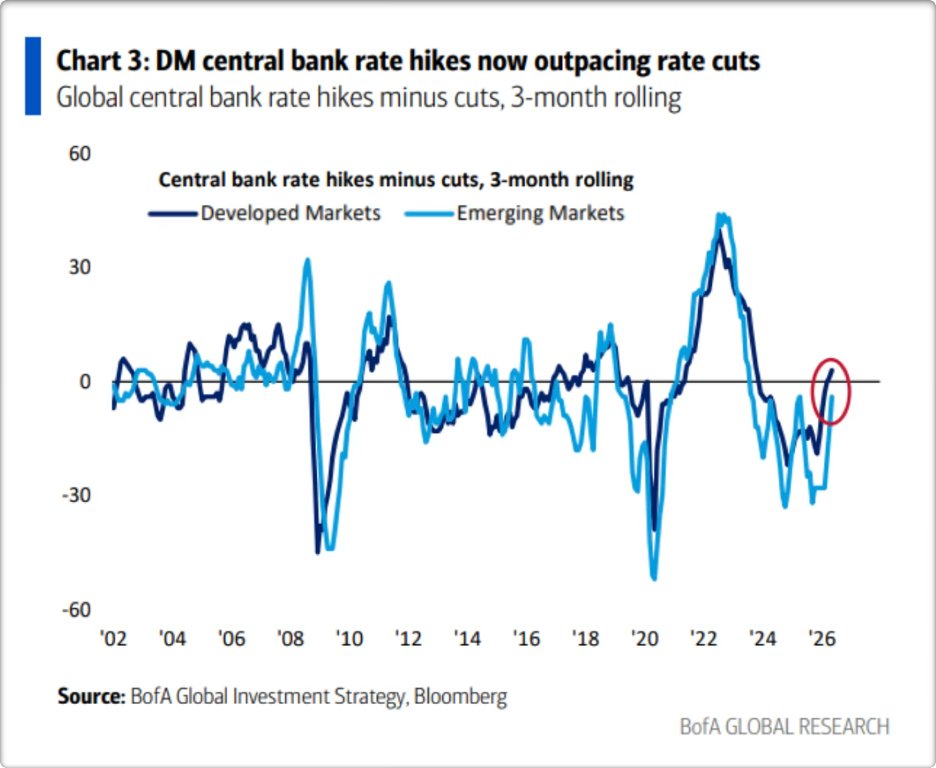

5. The End of a Rate Cutting Cycle – Financial conditions are tightening as most global central banks are moving from interest rate cuts to interest rate hikes. Currently, the fed funds futures market indicates that the U.S Federal Reserve is more likely to hike interest rates by the end of the year than not, with the probability of a rate cut near zero.

Rate cuts act as economic stimulus, while rate hikes act as brakes on the economy. Central bank benchmark rate increases are designed to cool inflation by making money more expensive. Potential side effects of rate hikes include slower economic growth, lower equity valuations, and pressure on corporate profits.

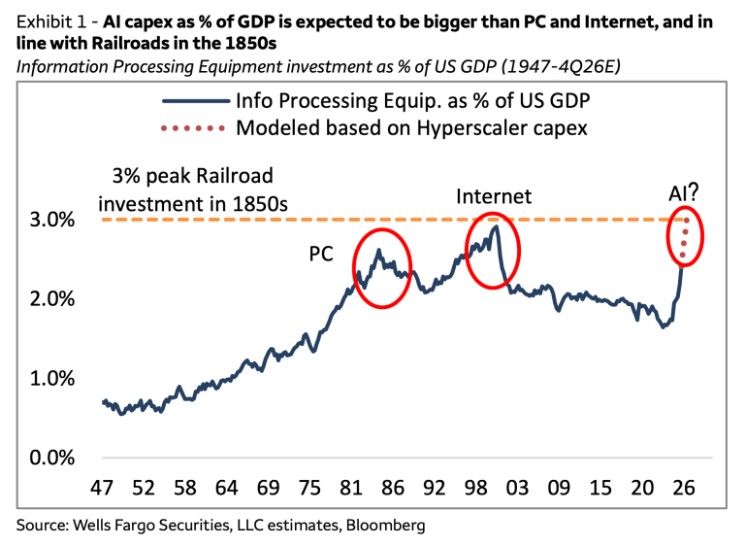

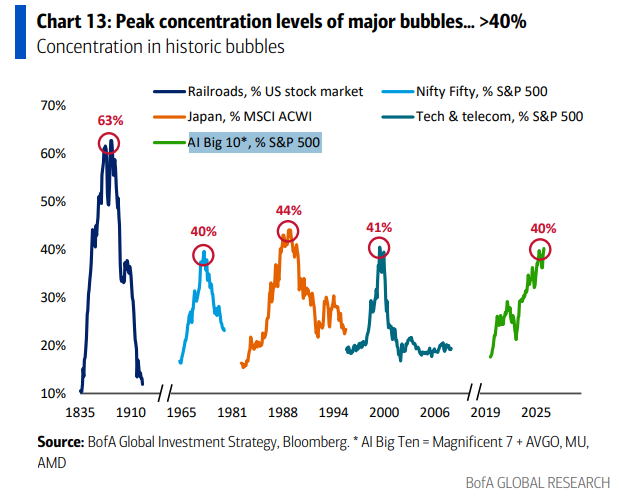

6. Unsustainable AI-Related Capital Expenditures – The technology behemoths known as the hyperscalers are expected to spend more than $700 billion on artificial intelligence-related capital expenditures this year. Additionally, forecasts indicate that this annual AI-related capex may exceed $1 trillion next year. The Wall Street Journal estimated that the AI economy grew by 31% while the non-AI economy grew by just 0.1%. The amount of capital expenditure going into AI as a % of GDP is expected to exceed past levels during previous investment manias including the tech bubble of the late 1990s and the railroad boom of the 1850s.

Current AI capex is huge, and investors are right to question whether it will generate adequate returns on capital. However, it can remain sustainable as long as hyperscalers keep generating sufficient cash flow and AI demand keeps converting into revenue, and if the resulting cash flows end up providing sufficient economic returns. If not, the historical precedents regarding the reversal of investment bubbles are not pretty. For example, when the tech bubble burst, it was the high asset firms, or those spending heavily on capital expenditures, who saw their share prices fall on average -90% from peak to trough. In comparison, low asset (or asset light) firms saw their share prices hold up relatively well.

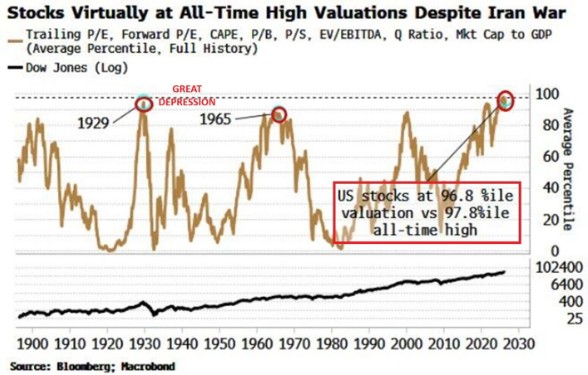

7. Sky-High Equity Valuations – Historically, future stock returns have been negatively correlated with valuations: the higher the starting valuation, the lower the expected long-term return, and vice versa. Over the long run, valuations act as gravity, eventually pulling returns back toward historical averages. Currently, the U.S. stock market’s valuation has reached record levels based on a myriad of metrics.

When valuations are high, future returns depend more heavily on earnings growth because there is less room for multiple expansion and a greater risk of multiple contraction. Empirical data indicate that valuation ratios have meaningful power in forecasting long-horizon stock returns, and high equity valuations typically correspond with lower-than-average future returns.

Why Does the Stock Market Continue to Ignore all of This?

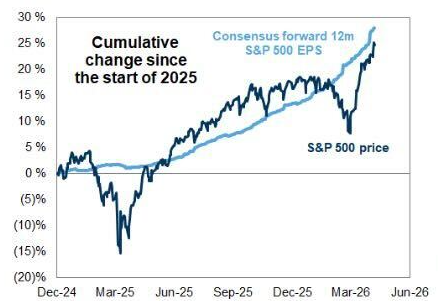

The answer is fairly simple: Earnings.

Despite the chaos, volatility, and risks, corporate profits are surging, and the stock market has followed.

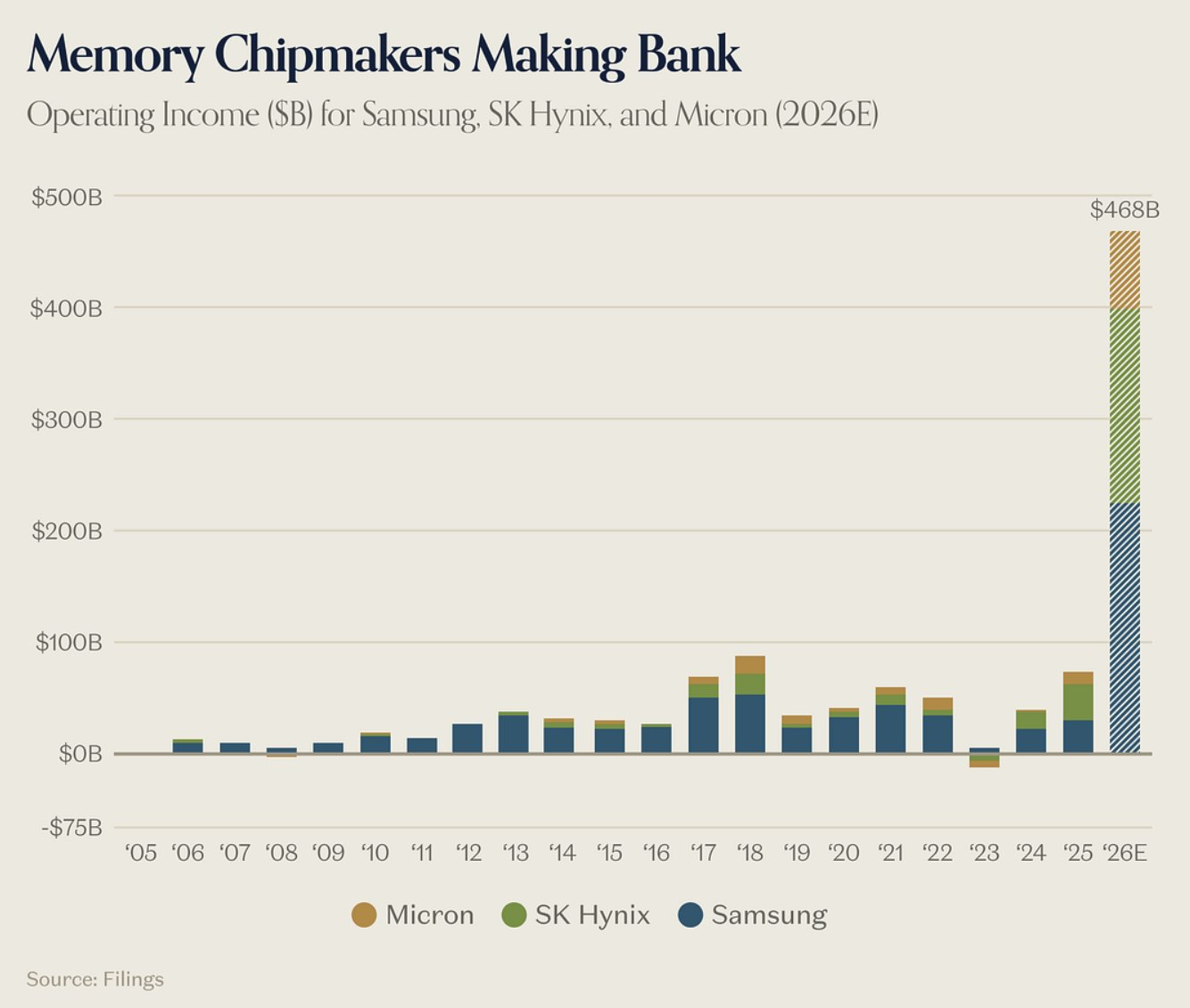

There is no sector more representative of surging profits driving stock prices higher than memory chipmakers. The profit growth from the three major memory players, including Micron, SK Hynix, and Samsung, has been downright absurd. This group’s first-quarter revenue greatly exceeded their previous best year, and their current year profit forecast (with a growth rate of more than 450%) is expected to be 5-fold greater than their previous best year.

Memory chip profits are surging because AI has turned memory from a commodity into a scarce bottleneck. AI servers need huge amounts of high-bandwidth memory, and SK Hynix, Samsung, and Micron are benefiting from the AI infrastructure buildout. Memory supply is tight, and prices are rising sharply. With powerful operating leverage, explosive profit growth results.

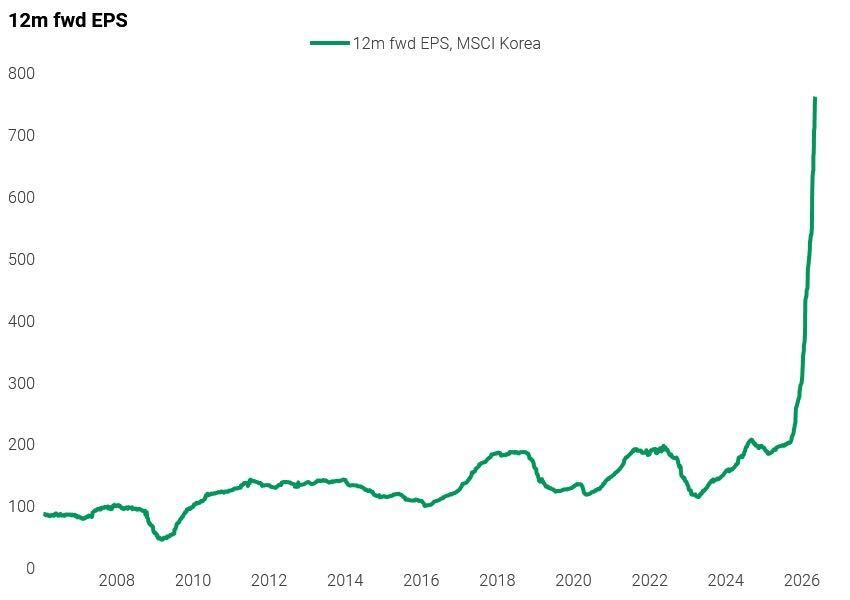

The stunning profit growth of memory chipmakers has been concentrated in South Korea’s stock market, where earnings growth has gone vertical.

As a result, the country’s stock market has experienced exceptional returns. South Korea’s 127% one-year return has driven its aggregate market capitalization above Canada’s.

Having 50% of the equity index in memory providers SK Hynix and Samsung is like having the two best NHL players, Connor McDavid and Leon Draisaitl, on the same team. Oh wait…

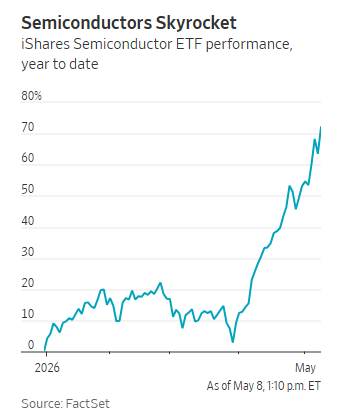

A similar but less extreme dynamic is playing out in the U.S stock market, in which significant profit growth resulting from record AI spending is causing the share prices of semiconductor companies to rally.

The stock market is going up because earnings are rising. Earnings are rising because AI spending is surging. AI spending is surging because, well, its result is to be seen. The sustainability of the current AI capex boom is the biggest bull-bear debate in the market currently. Next year’s forecast of more than $1 trillion in AI investment, and the resulting profits, trumps all other risks threatening the global economy (pun intended).

The main uncertainty facing investors is not war, geopolitical chaos, surging inflation, rising long-term bond yields, the end of a rate cutting cycle, or sky high equity valuations. It is how sustainable is the current AI investment boom. The boom-bust nature of historical precedents should give investors pause.

While Beatlemania lasted roughly three to four years at peak intensity, investors should be prepared for an environment in which the AI boom turns bust.

But for now, as the good times roll, bullish investors are choosing to just let it be.

Accelerate manages five alternative investment solutions, each with a specific mandate:

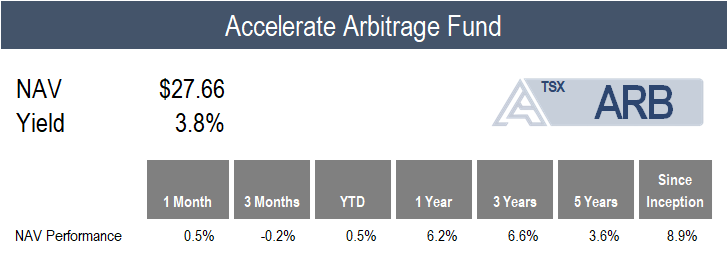

- Accelerate Arbitrage Fund (TSX: ARB): Merger Arbitrage

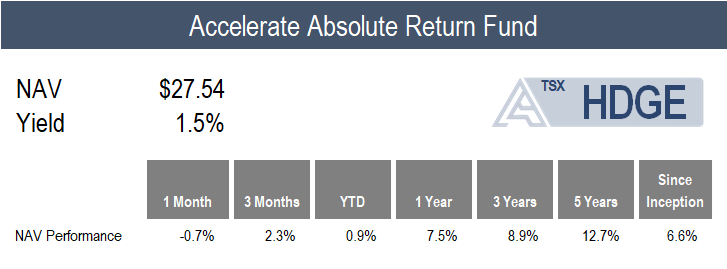

- Accelerate Absolute Return Fund (TSX: HDGE): Absolute Return

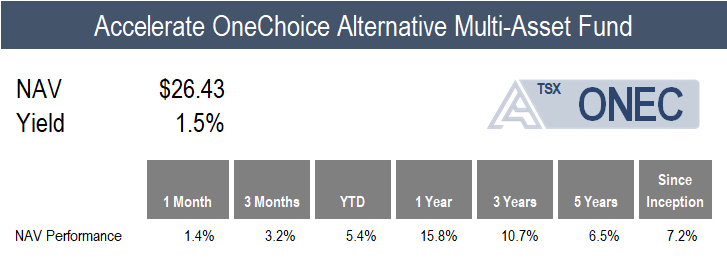

- Accelerate OneChoice Alternative Multi-Asset Fund (TSX: ONEC): Multi-Asset

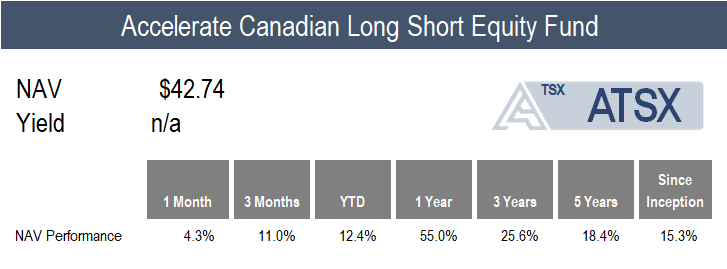

- Accelerate Canadian Long Short Equity Fund (TSX: ATSX): Long Short Equity

- Accelerate Diversified Credit Income Fund (TSX: INCM): Private Credit

ARB gained 0.5% in April compared to the benchmark S&P Merger Arbitrage Total Return Index’s 0.8% gain.

The Fund established several new investments during the month, including six merger arbitrage positions (two in the U.S. and four in Canada) as well as eleven SPAC IPO allocations.

Currently, ARB is 163.7% long and -3.2% short (166.9% gross exposure), with 71% allocated to SPAC arbitrage and 29% to merger arbitrage (with 9% in LBOs and 20% in strategic M&A).

![]()

HDGE declined by -0.7% in a difficult month for short selling and hedging.

While April was challenging for beta-neutral equity portfolios, the bulk of the damage occured in the U.S. value and quality factors. The top 10% most overvalued stocks were up 18.1%, outperforming the top 10% most undervalued stocks by 10.3%. Meanwhile, the top 10% of the lowest-quality stocks rallied by 16.4%, outperforming the top decile of quality stocks by 10.1%. For reference, the Goldman Sachs Most Shorted basket, typically representative of the market’s most attractive stocks to bet against, rallied 14.2% in April.

Top Fund contributors include long positions in Seagate Technology, Micron Technology, and Garrett Motion. Top Fund detractors include short positions in Fuelcell Energy, Hudson Pacific Properties, and Molina Healthcare.

![]()

ONEC gained 3.2% in April, primarily driven by a bounce back in the Fund’s private credit and real estate allocations, which rose 9.1% and 6.5%, respectively.

Other positive contributors to ONEC’s performance include long short equity, risk parity, commodities, leveraged loans, and managed futures, which generated returns of 2% to 5%.

The Fund’s merger arbitrage allocation added 0.5%, while its gold and infrastructure allocations were flat. ONEC’s absolute return allocation had a -0.7% return.

![]()

ATSX increased by 4.3% last month, in line with the benchmark S&P/TSX 60 Index’s 4.3% return.

Canadian long short factor portfolios held up significantly better than those in the U.S., such that ATSX’s long positions offset the negative performance contribution of its short positions. Specifically, the Canadian long short value, quality, and price momentum factors generated negative returns, which were offset by the positive returns from the operating momentum factor.

Top Fund contributors include long positions in Bombardier, Finning International, and IGM Financial. Top Fund detractors include a short position in Well Health Technologies, along with long positions in BRP and Orla Mining.

![]()

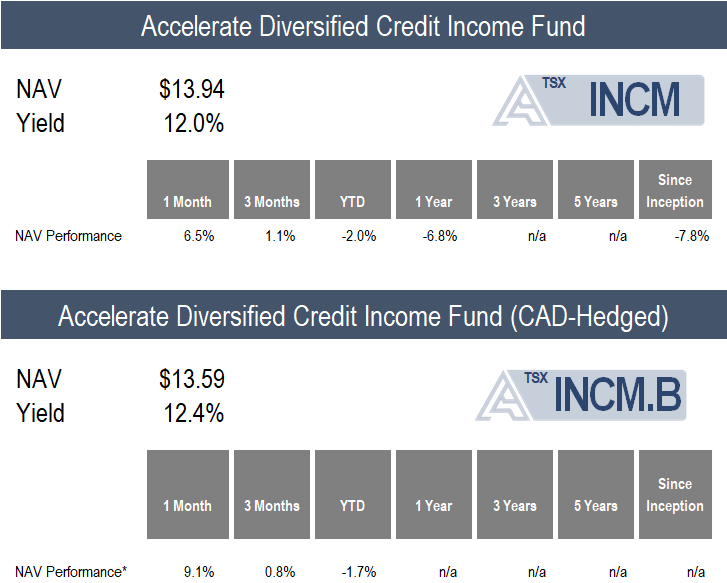

INCM gained 6.5% in April (9.1% on a currency hedged basis).

INCM’s private credit holdings bounced back from deeply discounted levels, with the average NAV discount rising month-over-month from more than -25% to -21%.

Currently, INCM is allocated to 20 private credit portfolios (through listed BDCs), totaling more than 5,000 loans and investments, of which 86.5% are senior secured and 92.2% are floating rate. The current yield on the INCM portfolio is 11.8%, and it trades at a -21% discount to its net asset value. INCM’s exposure to software loans is 16.6% of its portfolio.

![]()

Have questions about Accelerate’s investment strategies? Click below to book a call with me:

-Julian

Disclaimer: This distribution does not constitute investment, legal or tax advice. Data provided in this distribution should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. Please read the relevant prospectus before investing. For a summary of the risks of an investment in the Accelerate ETFs, please see the specific risks set out in the prospectus. ETFs are not guaranteed and the information in this distribution is based on current market conditions and may fluctuate and change in the future. Past performance is not indicative of future results. Decisions regarding tax, investments, and all other financial matters should be made solely with the guidance of a qualified professional. Visit www.AccelerateShares.com for more information.