April 12, 2026 – The Iran conflict and the resulting disruptions around shipping through the Strait of Hormuz have had wide-ranging economic implications, with the most immediate and significant impact being the surge in commodity prices.

The chokehold on oil supply from the Strait blockade has caused energy markets to react swiftly. As oil prices have increased, refined fuels such as gasoline, diesel, and jet fuel have followed, driving up global transportation and logistics costs.

Additionally, natural gas prices have spiked due to disruptions to LNG production and transportation in the Middle East. The knock-on effects of an increase in natural gas prices are significant. For example, fertilizer prices have increased markedly because production is highly energy-intensive and the Middle East was a key exporter of inputs such as ammonia and urea. Consequently, higher fertilizer costs have led to increased prices for agricultural commodities such as wheat, corn, and soybeans, as farmers faced increased input costs and potential supply constraints.

Moreover, industrial commodities have seen prices rise. Aluminum prices have jumped because of higher energy costs and supply chain disruptions. Sulphur and helium prices have risen due to regional production exposure and transportation bottlenecks.

The overall economic effect of the Iran conflict has cascaded throughout commodity markets and supply chains. Energy prices moved first, which caused the prices of transportation, fertilizer, and industrial inputs to jump. Ultimately, consumers feel the effects through a spike in the prices at the pump and the grocery store.

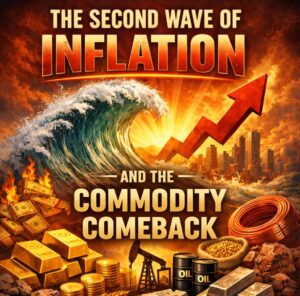

Unsurprisingly, inflation expectations have surged. The most recent University of Michigan survey on 1-year inflation expectations of U.S. households indicated a gloomy state of the consumer, as U.S. households expect the year-ahead inflation to spike to 4.8%, up from 3.8% last month.

Source: Trading Economics, University of Michigan

This recent surge in inflation expectations stands in stark contrast to the previous decline experienced earlier this year, as consumers and the economy were still adjusting to the inflation spike caused by the emergence of the trade war last spring.

It turns out that continued macroeconomic chaos is unpleasant for both consumers and investors.

That said, while consumers have to largely grin and bear the surge in commodity prices and inflation, investors can benefit from it.

Commodity investing allows investors to capitalize on price increases across the commodity complex. Allocating to the asset class is fundamentally different from traditional stock and bond investing because it does not produce cash flows via interest or dividends. Commodity investing provides exposure to real assets whose prices are driven by supply, demand, and inflation, rather than corporate earnings or interest rates. Allocators can invest in commodities through futures contracts or ETFs.

Commodities are typically grouped into four major categories:

- Energy – This includes oil, natural gas, and refined fuels. These are the most macro-sensitive and often the biggest drivers of inflation shocks.

- Metals – Precious metals like gold and silver act as stores of value, while industrial metals like copper and aluminum track global growth and infrastructure demand.

- Agriculture – These include grains, softs, and livestock. Prices are influenced by weather, geopolitics, and input costs like fertilizer and fuel.

- Other / niche commodities – This includes things like uranium, lithium, and carbon credits, which are often tied to structural themes such as energy transition.

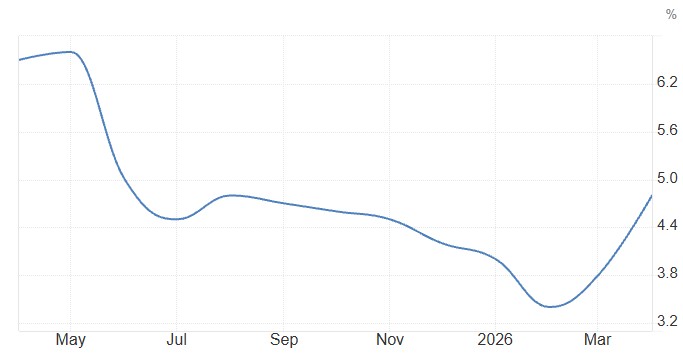

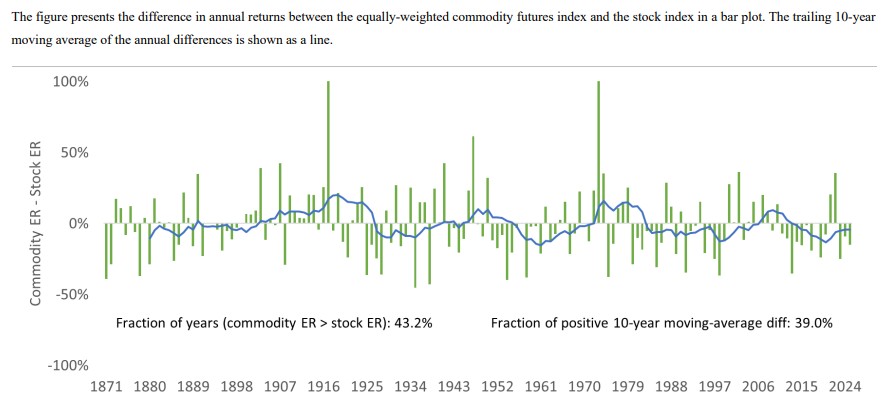

Historically, the returns of a broadly diversified index of commodity futures have provided investors with attractive returns. According to the paper, An Index of Commodity Futures Returns Since 1871 by Janardanan, Qiao, and Rouwenhorst, commodity futures have earned an average annual risk premium of 5.4% over the risk-free rate and a premium over U.S. inflation of more than 6% per annum going back more than 150 years.

Source: An Index of Commodity Futures Returns Since 1871

Moreover, commodity futures have outperformed equities in roughly 43% of years and in two out of every five decades, suggesting distinct return drivers and meaningful diversification benefits.

Source: An Index of Commodity Futures Returns Since 1871

Nevertheless, while commodities have underperformed equities over the long term, the main reason to allocate to them is their diversification benefit. Commodity returns are often uncorrelated or even negatively correlated with stocks and bonds. When equities struggle due to rising rates or margin pressure, commodities can outperform, improving portfolio risk-adjusted returns and reducing drawdowns.

Unlike equities, commodities can spike sharply when supply is disrupted. Events involving Iran or constraints in the Strait of Hormuz are good examples of situations in which energy prices surge quickly. These events create asymmetric upside that is hard to replicate elsewhere in a portfolio.

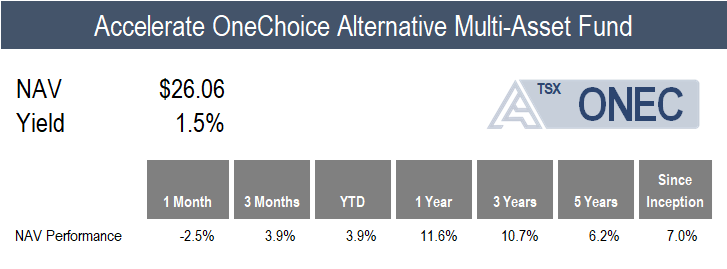

Given their positive contributions to an investment portfolio, commodities are typically used as a strategic allocation, often in the range of 5% to 15% of an overall portfolio. The Accelerate OneChoice Alternative Multi-Asset Fund (TSX: ONEC) has a 5% allocation to a basket of commodities, in addition to a 10% allocation to gold.

Investors may do well to consider either a strategic or tactical allocation to commodities amid the second wave of inflation and the commodity comeback.

Accelerate manages five alternative investment solutions, each with a specific mandate:

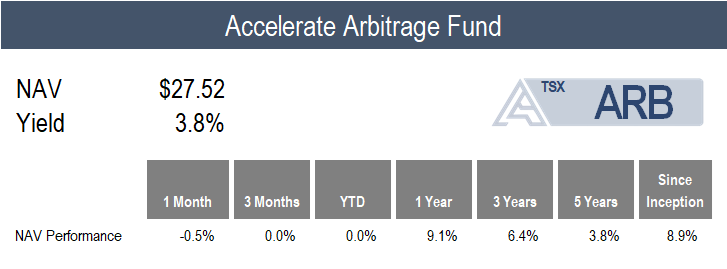

- Accelerate Arbitrage Fund (TSX: ARB): Merger Arbitrage

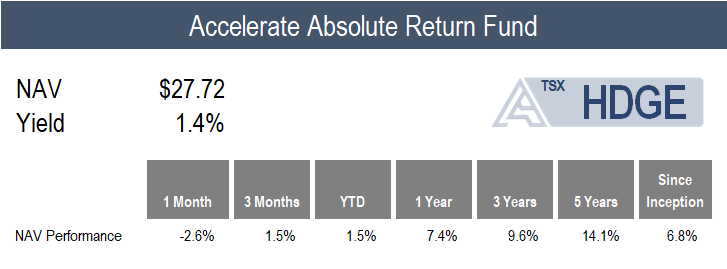

- Accelerate Absolute Return Fund (TSX: HDGE): Absolute Return

- Accelerate OneChoice Alternative Multi-Asset Fund (TSX: ONEC): Multi-Asset

- Accelerate Canadian Long Short Equity Fund (TSX: ATSX): Long Short Equity

- Accelerate Diversified Credit Income Fund (TSX: INCM): Private Credit

ARB declined -0.5% last month compared to the benchmark S&P Merger Arbitrage Total Return Index’s 0.4% gain.

The Fund’s modest loss was driven primarily by SPAC and merger arbitrage spreads widening slightly, with SPAC arbitrage yields rising from 3.7% to 4.0% and merger arbitrage yields increasing from 9.8% to 10.0%.

During the month, ARB added three new merger arbitrage positions (out of eighteen announced deals) to its portfolio. Out of the eleven SPAC IPOs during the month, ARB participated in five. Moreover, the bidding war for Janus Henderson Group ended, with interloper Victory Capital coming away defeated after the original bidder, Trian Fund Management, won the deal with a moderate 6.1% price increase. It was not what we were hoping for from a bidding war, but a reasonable result.

Currently, ARB is 156.7% long and -2.9% short (159.6% gross exposure), with 74% allocated to SPAC arbitrage and 26% to merger arbitrage (with 13% in LBOs and 13% in strategic M&A).

![]()

HDGE fell -2.6% in a challenging month for short portfolios.

Typically, in a declining market, HDGE’s low-quality “junk” stock short positions materially underperform the market, buoying Fund performance. Unfortunately, March was not a typical month, characterized by hedge fund degrossing and resulting in material junk stock outperformance. For example, the Goldman Sachs Most Shorted basket finished the month up 0.1%. Meanwhile, the Goldman Sachs Hedge Fund VIP long basket slumped by -7.5%, leading to a -7.6% decline for the long short hedge fund proxy (GS VIP longs – GS Most Shorted).

Top Fund contributors include short positions in Quanterix, Archer Aviation, and Newell Brands. Top Fund detractors include long positions in Herbalife and OceanaGold, as well as a short position in Spire Global.

![]()

ONEC declined by -2.5% in March – a month in which relative alternative asset class performance flipped.

In February, all alternative asset classes in ONEC contributed positively except for the credit bucket (which includes broadly syndicated loans and private credit). In March, the credit bucket was one of the few allocations with positive performance, as private credit gained 3.9% and broadly syndicated loans ticked up 0.8%. ONEC’s other positive contributor last month was its commodities portfolio, which jumped by 5.2%.

In contrast, gold, real estate, and risk parity were the Fund’s biggest monthly detractors, with losses of -11.8%, -7.5%, and -5.6%. Also, long short equity, managed futures, and absolute return each declined by between -2.0% and -4.0%. Finally, the Fund’s merger arbitrage and infrastructure allocations declined by less than -1.0%.

![]()

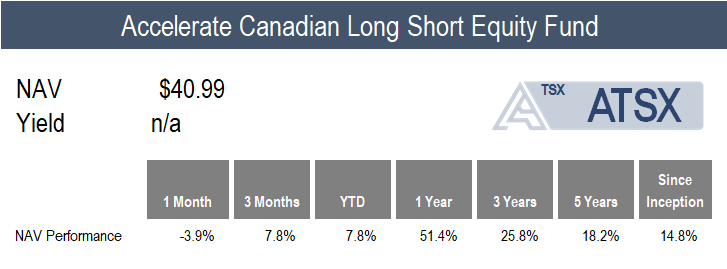

ATSX dropped by -3.9% last month, compared to the benchmark S&P/TSX 60 Index’s -3.1% loss.

Top Fund contributors include short positions in goeasy and Ivanhoe Mines, as well as a long position in Athabasca Oil. Top Fund detractors include a short position in Boralex, along with long positions in Orla Mining and OceanaGold.

![]()

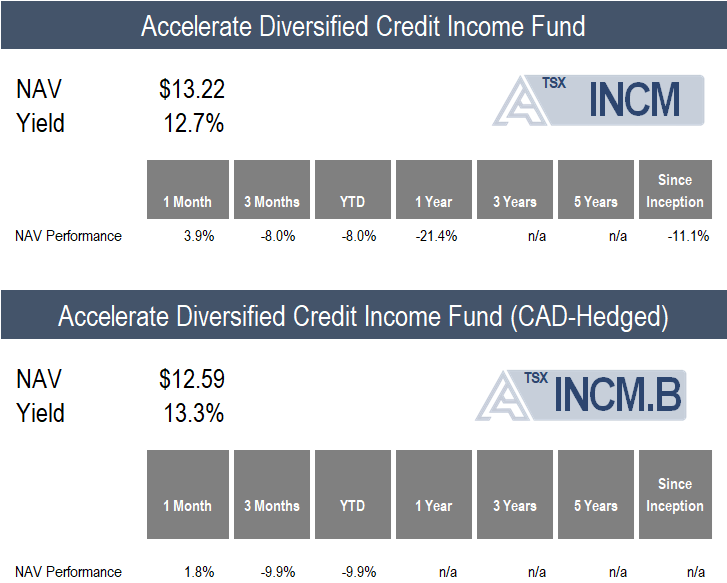

INCM gained 3.9% in March (1.8% on a currency hedged basis).

While private credit has been mired in negative sentiment for the past seven months due to several narratives, the primary of which is the AI will kill software thesis, we believe the recent relative outperformance of private credit has been driven by attractive valuations. It is a reasonable thesis that the -25% average NAV discount for listed BDCs reflects a credit default scenario that is unlikely to occur. As discussed in our most recent Liquid Private Credit Monitor, underlying private credit fundamentals remain far better than what listed BDC prices imply.

Currently, INCM is allocated to 20 private credit portfolios (through listed BDCs), totaling more than 5,000 loans and investments, of which 83.9% are senior secured and 89.5% are floating rate. The current yield on the INCM portfolio is 12.6%, and it trades at a -25% discount to its net asset value. INCM’s exposure to software loans is 16.2% of its portfolio.

![]()

Have questions about Accelerate’s investment strategies? Click below to book a call with me:

-Julian

Disclaimer: This distribution does not constitute investment, legal or tax advice. Data provided in this distribution should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. Please read the relevant prospectus before investing. For a summary of the risks of an investment in the Accelerate ETFs, please see the specific risks set out in the prospectus. ETFs are not guaranteed and the information in this distribution is based on current market conditions and may fluctuate and change in the future. Past performance is not indicative of future results. Decisions regarding tax, investments, and all other financial matters should be made solely with the guidance of a qualified professional. Visit www.AccelerateShares.com for more information.