March 30, 2026 – Seemingly every spring, geopolitical chaos erupts, causing equity prices to slump, interest rates to surge, and corporate deal activity to plummet.

Last April, there was the emergence of the U.S trade war, which introduced tariffs, supply chain disruptions, and persistent policy uncertainty, the result of which materially increased the cost of doing business. Companies faced higher financing costs due to a rapid increase in their cost of capital, and thus strategic decisions such as mergers and acquisitions were put on the back burner until the chaotic environment normalized.

This month, the U.S.–Israel–Iran war began with coordinated strikes on Iranian military and nuclear infrastructure, triggering retaliation along with disruptions to critical energy and shipping routes. The conflict has quickly evolved into a broader geopolitical shock, with attacks across the Middle East and threats to key chokepoints like the Strait of Hormuz, a vital artery for global oil supply. From a capital markets standpoint, the result has been similar to the trade war last spring – a significant decline in stock prices, a rapid rise in interest rates, and a surge in market volatility, which has once again caused the dealmaking machine to slump.

The second half of 2025 was characterized by a booming M&A market, an amount which pushed the yearly tally into the record books as the most active year for mergers and acquisitions. That trend in dealmaking continued unabated for the first couple of months of 2026, supported by stable equity markets, declining interest rates, and low expected policy uncertainty.

However, all of that changed as the war in the Middle East broke out, one consequence of which is that dealmaking came under fire.

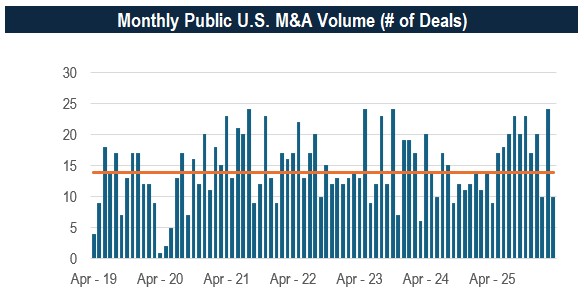

Month-to-date, just 10 public U.S. M&A transactions have been announced, well below the monthly average of 14 over the past seven years and 18 deal monthly average over the past year.

Source: Accelerate

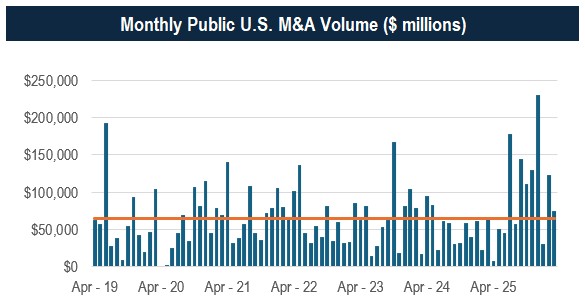

The deal slump primarily emerged after the first few days of the conflict, as the market began pricing in prolonged hostilities and increasing volatility. That said, the total transaction value of $75 billion for March actually came in above the seven year average of $65 billion, predominantly due to the $33.4 billion buyout of The AES Corporation by a consortium including GIP, EQT, CalPERS, and QIA, announced on March 2nd. Moreover, the pace of deal activity in March was far from the depths experienced during last April’s trade war, when aggregate monthly deal volume plummeted to just $7.6 billion.

Source: Accelerate

Nevertheless, despite the increase in market volatility and corresponding decrease in dealmaking activity, some large strategic transactions were announced during the month, including:

- Corebridge Financial’s $10.5 billion merger with financial services holding company Equitable Holdings

- Public Storage’s $10.5 billion combination with real estate investment trust National Storage Affiliates

- Cintas Corporation’s $5.5 billion acquisition of uniform and workwear supplier UniFirst Corporation

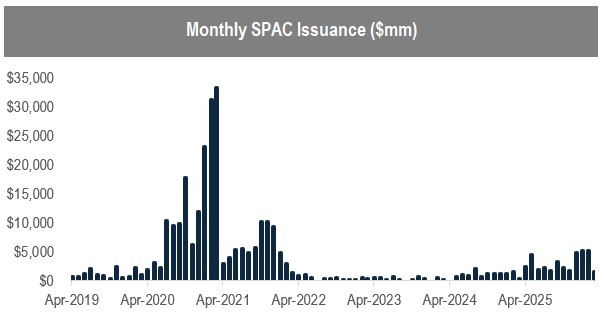

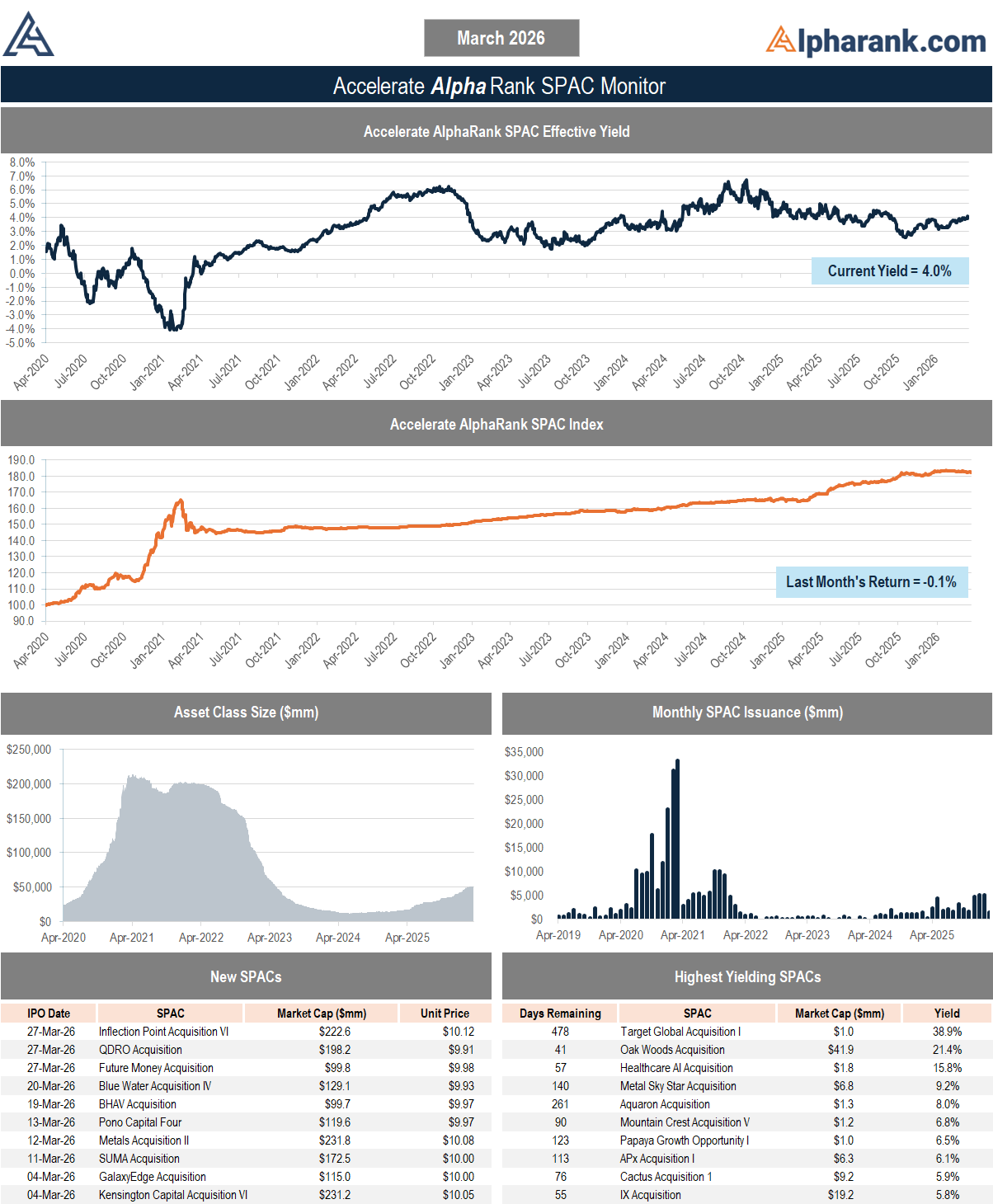

Another area of the merger market slowed last month. Special Purpose Acquisition Company (SPAC) issuance declined, with just 10 SPAC IPOs coming to market, raising $1.5 billion, representing a significant decline from the blistering pace in February, in which 27 SPACs went public, raising a total of $5.1 billion.

Source: Accelerate

We had previously lamented that recent SPAC IPO issuance activity far exceeded SPAC merger announcements, potentially leading to an excess supply and an increasingly unbalanced market. On a positive note, 8 blank check companies announced mergers this month, nearly matching the number of new SPACs coming to market.

However, the one thing missing from the SPAC market is investor enthusiasm. For example, on March 4th, Bleichroeder Acquisition II (NASDAQ: BBCQ) announced a $2.0 billion merger with quantum computing Pasqal. In a normal market, the SPAC shares likely would have risen significantly on the back of this deal announcement, as we have seen with previous quantum computing mergers. Due to current poor market sentiment, the enthusiasm for the Pascal deal did not arrive as expected, with the SPAC shares rising just 0.7%.

How long the conflict in the Middle East lasts is anyone’s guess. That said, last year’s trade war provides a reasonable precedent. Last spring, as the U.S. 10-year Treasury yield rose to 4.5% and the S&P 500’s decline neared -20%, harmful policy actions were reversed mere weeks after being announced, and subsequently, deal activity came roaring back. Using the recent surge in Treasury yields as a leading indicator, we would not be surprised to see the conflict in the Middle East die down sooner rather than later.

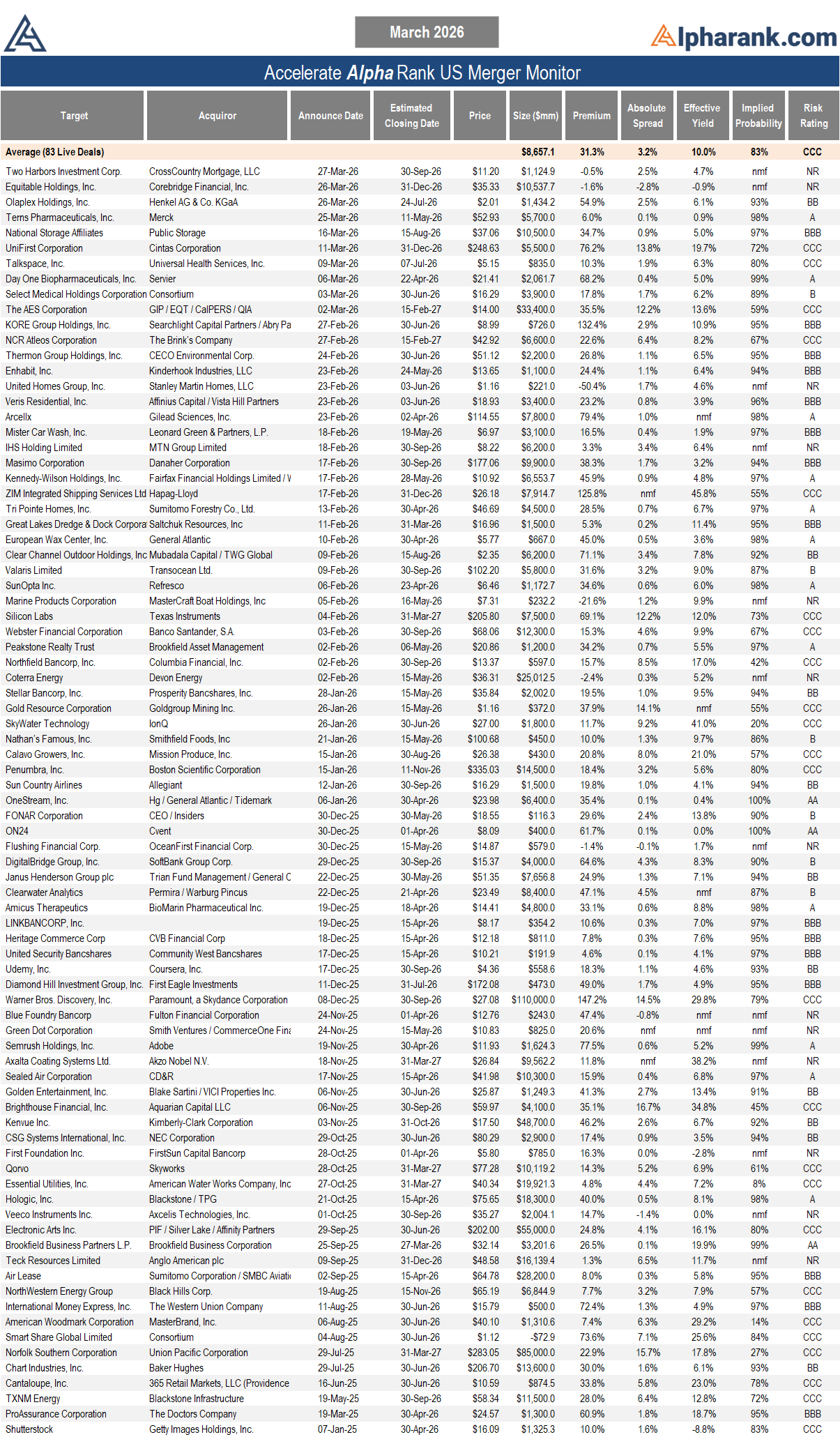

The AlphaRank.com Merger Monitor below represents Accelerate’s proprietary analytics database on all announced liquid U.S. mergers. The AlphaRank Merger Arbitrage Effective Yield represents the average annualized returns of all outstanding merger arbitrage spreads and is typically viewed as an alternative to fixed income yield.

Each individual merger is assigned a risk rating:

- AA – a merger arbitrage rated ‘AA’ has the highest rating assigned by AlphaRank. The merger has the highest probability of closing.

- A – a merger arbitrage rated ‘A’ differs from the highest-rated mergers only by a small degree. The merger has a very high probability of closing.

- BBB – a merger arbitrage rated ‘BBB’ is of investment grade and has a high probability of closing.

- BB – a merger arbitrage rated ‘BB’ is somewhat speculative in nature and has a greater than 90% probability of closing.

- B – a merger arbitrage rated ‘B’ is speculative in nature and has a greater than 85% probability of closing.

- CCC – a merger arbitrage rated ‘CCC’ is very speculative in nature. The merger is subject to certain conditions that may not be satisfied.

- NR – a merger-rated NR is trading either at a premium to the implied consideration or a discount to the unaffected price.

The AlphaRank merger analytics database is utilized in running the Accelerate Arbitrage Fund (TSX: ARB), which may have positions in some of the securities mentioned.

* AlphaRank is exclusively produced by Accelerate Financial Technologies Inc. (“Accelerate”). Visit Alpharank.com for more information. Disclaimer: This research does not constitute investment, legal or tax advice. Data provided in this research should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this research is based on current market conditions and may fluctuate and change in the future. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Accelerate may have positions in securities mentioned. Past performance is not indicative of future results.