March 22, 2026 – The concept of value investing, implemented as buying an asset for less than it is worth, appears to be simple and intuitive on the surface.

However, from a practical standpoint, sticking with a strategy that invests in securities trading below their intrinsic value, particularly if this strategy underperforms the market for multiple years in a row, is easier said than done. Additionally, a more “pure” form of value investing, which involves not only buying undervalued securities but also short selling overvalued ones, can add complexity and in turn, even more skepticism (which is only amplified during periods of underperformance).

Value investing, as both a market philosophy and a formal investment discipline, has evolved over the past century along a long arc that spans from early security analysis to modern academic finance. Its history is best understood as a continuous dialogue between practitioners focused on intrinsic value and academics seeking to explain return premia through systematic factors, while continuously being advanced through continued market application and testing.

The intellectual foundations of value investing are based on the work of Benjamin Graham and David Dodd, whose early research was published in the seminal 1934 text, Security Analysis. Writing in the aftermath of one of the most challenging periods for investing, the Great Depression, Graham and Dodd advanced a framework grounded in the concept of investment analysis through the lens of intrinsic value, emphasizing the importance of a margin of safety, a result of buying a security far below their assessment of intrinsic value.

Academic engagement with the idea of value investing emerged in the context of the efficient market hypothesis, developed in the 1960s by scholars such as Eugene Fama. Early formulations of the efficient market hypothesis suggested that publicly available information should be fully reflected in asset prices, leaving little room for systematic outperformance through strategies such as value investing.

The first academic research specifically on value investing was published in 1977, Investment Performance of Common Stocks in Relation to Their Price-Earnings Ratios: A Test of the Efficient Market Hypothesis by Sanjay Basu. In the study, Basu concluded that stocks with a low Price / Earnings multiple outperformed those with a high multiple: “During the period April 1957-March 1971, the low P/E portfolios seem to have, on average, earned higher absolute and risk-adjusted rates of return than the high P/E securities.”

Since then, research from academics, including Eugene Fama and Kenneth French, as well as practitioners, including Cliff Asness, has added to the body of research supporting the outperformance of the so-called value factor. Moreover, over the years, additional quantitative metrics beyond price / earnings and price / book value to measure value have emerged, including enterprise value / EBITDA and price / free cash flow, among others.

That said, while academic research has noted the outperformance of value investing over long periods throughout history, there have been periods of significant underperformance (particularly during the late 2010s) that have led many market prognosticators to question value investing’s continued effectiveness. Some argued that structural changes, including the rise of intangible capital and winner-take-all dynamics in technology sectors, have weakened traditional value metrics. Others maintained that the premium remains intact but is subject to long and painful drawdowns, consistent with a risk-based explanation.

It is due to these value drawdowns that some capital allocators have started to believe that value investing is dead.

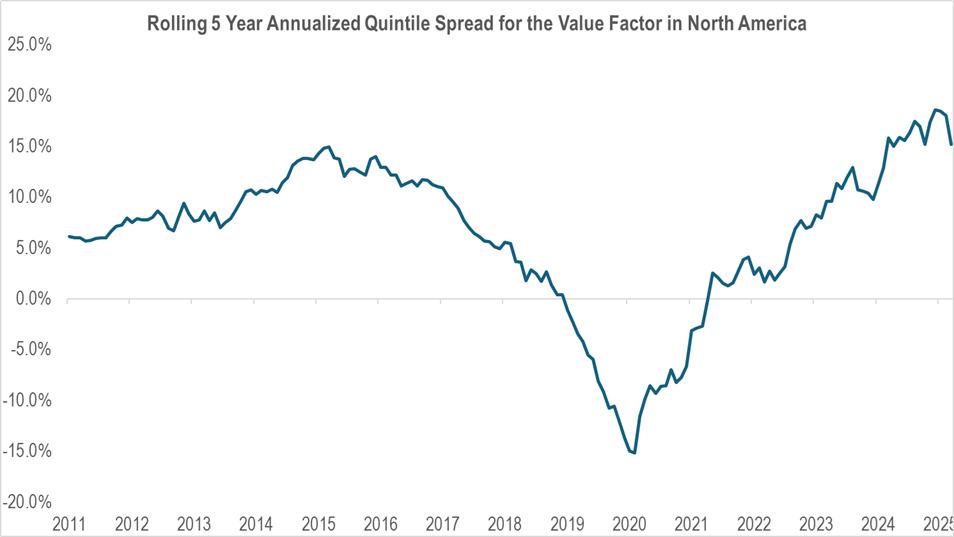

To investigate the claim, we ran a backtest analyzing the 5-year annualized performance of a portfolio that is long the top quintile value stocks (long the cheapest securities) and is short the bottom quintile value stocks (betting against the most expensive securities) in North America starting in 2006 (with the 5-year returns beginning in 2011). The analysis utilizes Accelerate’s proprietary composite of value factors and is rebalanced monthly.

As seen below, since 2011, the value premium has been positive, generating a 6.2% annualized spread between the cheapest stocks and the most expensive.

Source: Accelerate

However, the spread was punishingly inconsistent, with the 5-year annualized returns for the long short value portfolio turning deeply negative in the periods ending in 2020 through 2022. In fact, the long short value portfolio’s worst 5-year return bottomed at -15% annualized at the end of 2020, when overvalued speculative securities reached their peak share price performance following the Covid pandemic.

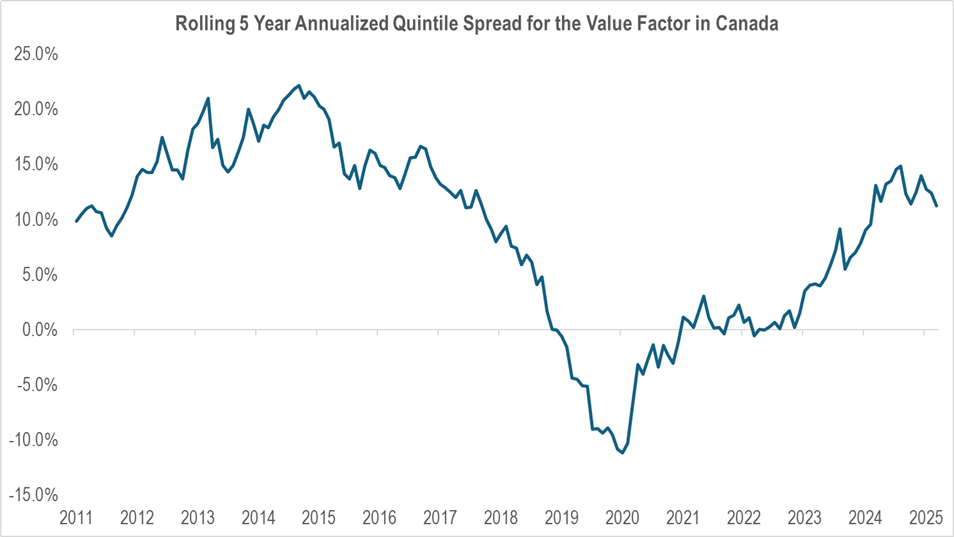

The Canadian stock market featured a similar performance for the long short value portfolio, however, the bottom was not as punishing. Since 2011, the long short value portfolio has generated an 8.6% average annualized 5-year rolling return since 2011. That said, it was not an easy ride for investors, as the worst period resulted in a return of -11.1% annualized for the 5-year period ending in 2020.

Source: Accelerate

With that tough stretch of 5-year annualized returns, it is no wonder that many investors gave up on value in the early 2020s.

Thankfully, since then, not only has value investing not died, however, it has made a roaring comeback. During the most recent 5-year period, the North American long short value portfolio reached 15.2% annualized, while the Canadian portfolio that is long the cheapest and short the most expensive stocks generated an 11.2% annualized return.

As Mark Twain said in 1897, “The reports of my death are greatly exaggerated.”

Today, value investing occupies a unique position within both academic finance and portfolio management. It is both one of the most well-documented empirical regularities and one of the most contested in terms of interpretation.

That said, from a practitioner’s standpoint, the data show that value investing, particularly from a long-short perspective, remains an attractive investment strategy. Given the effectiveness of the value factor, which tends to improve when combined with other robust and uncorrelated systematic factors into a multi-factor approach, investors may benefit from utilizing factor rankings when selecting securities in which to go long or short. To help facilitate idea generation, we highlight one top-decile stock that is forecasted to outperform and one bottom-decile stock that is predicted to underperform in this month’s AlphaRank Top Stocks.

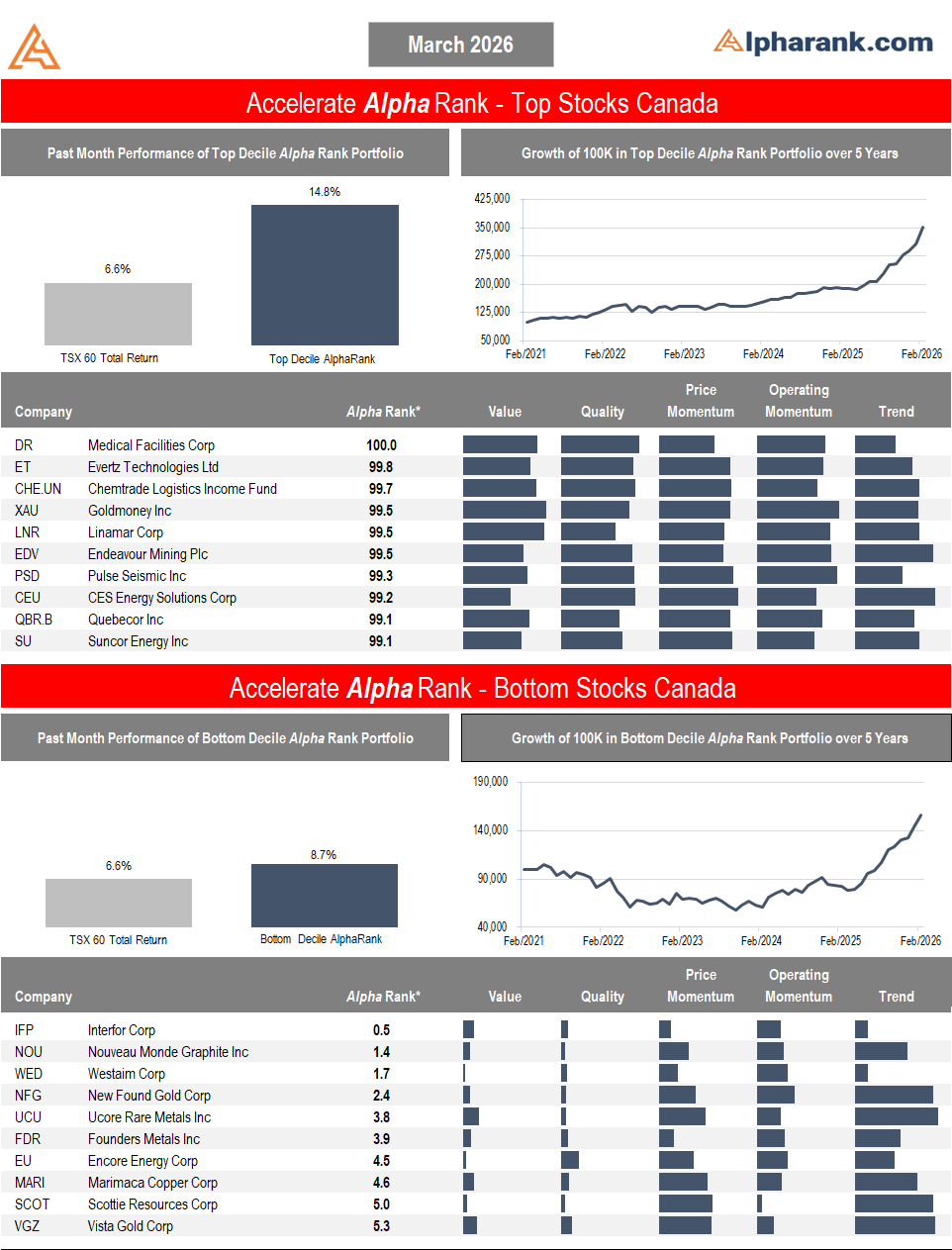

OUTPERFORM: Quebecor Inc (TSX: QBR.B) is a Montreal-based telecommunications and media company. While historically known for its media assets, the company today is fundamentally a telecom operator, with Vidéotron and Freedom Mobile driving the majority of its value. The strategic shift from a regional cable and media company into a national wireless challenger is central to the investment thesis. Québecor generates stable and growing cash flow despite modest top-line expansion. Revenue growth has been relatively muted, but EBITDA has remained resilient and free cash flow has accelerated meaningfully. Trading at a below-market 8.5x EBITDA and a 7.0% free cash flow yield, while generating a return on capital of 25.7%, QBR.B represents a compelling combination of value and quality. With positive share price momentum, along with an AlphaRank score of 99.1/100, we expect QBR.B shares to continue to outperform. Disclosure: Long QBR.B shares in the Accelerate Canadian Long Short Equity Fund (TSX: ATSX).

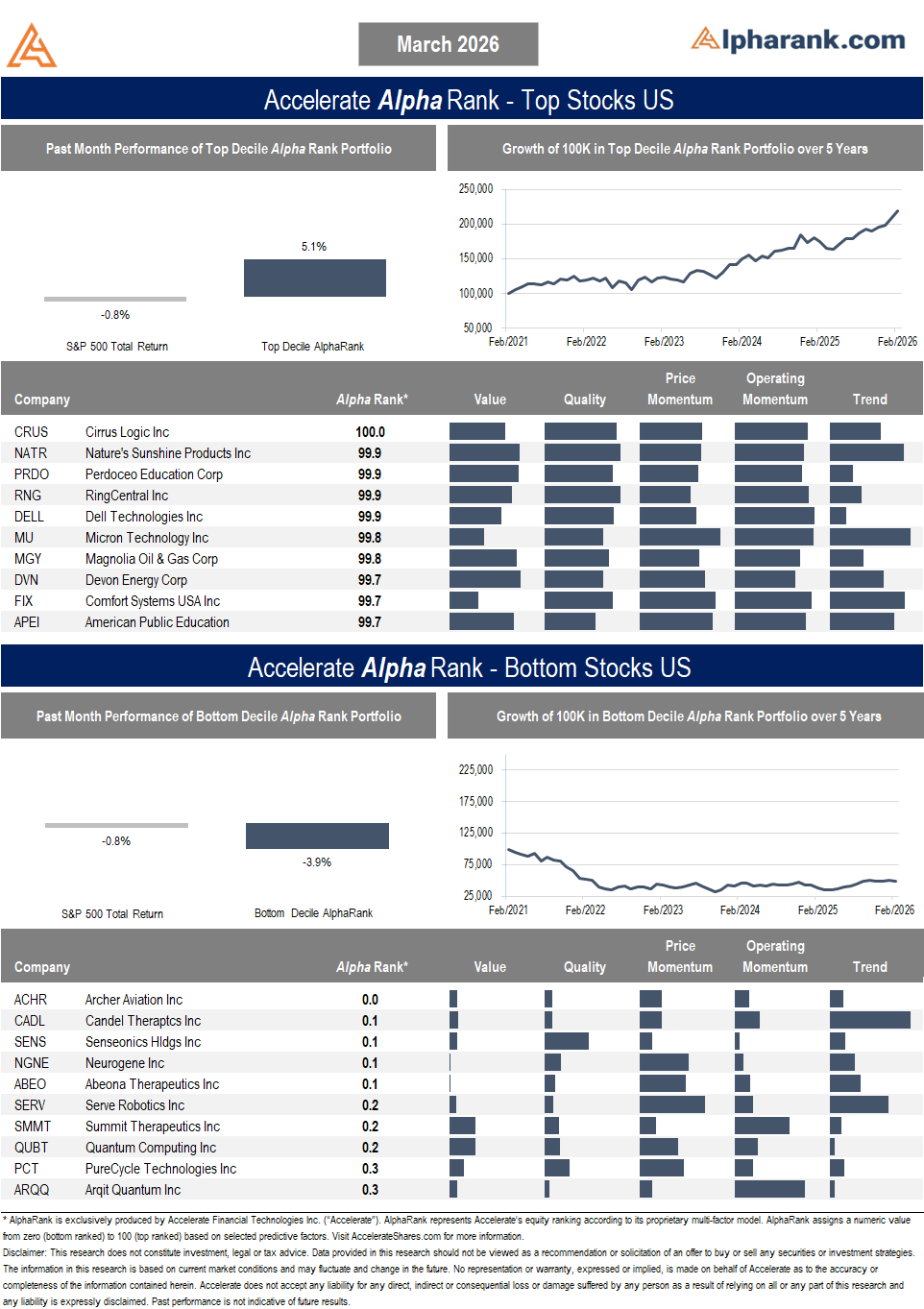

UNDERPERFORM: Archer Aviation Inc (NYSE: ACHR) is an early-stage aerospace company developing electric vertical takeoff and landing (eVTOL) aircraft, with the goal of launching “air taxi” services in urban environments. ACHR generates effectively zero revenue, with a net loss of approximately $618 million and operating cash burn of $433 million in 2025. It is reliant on continuously diluting shareholders to maintain solvency, presenting continuous downward pressure on the stock as more shares get sold into the market. As a result, the company’s shares outstanding have increased by 13x since 2020 and by 2.5x in just two years. Given that it recently missed quarterly expectations and free cash flow remains deeply negative, its path for a turnaround remains limited. With an AlphaRank score of 0.0/100 (the lowest ranking in the universe), we expect ACHR shares to continue to underperform. Disclosure: Short ACHR in the Accelerate Absolute Return Fund (TSX: HDGE).

The AlphaRank Top and Bottom stock portfolios exhibited positive relative performance last month:

- In Canada, the top-ranked AlphaRank portfolio of stocks gained 14.8%, outperforming the benchmark’s 6.6% increase, while the bottom-ranked portfolio of Canadian equities jumped 8.7%. The long-short portfolio (top minus bottom-ranked stocks) increased by 6.1%, as the top-ranked stocks outperformed the bottom-ranked securities. Over the past five years, the top decile AlphaRank portfolio has gained more than 250%, while the bottom-ranked portfolio has risen 56%.

- In the U.S., the top-decile-ranked equities rose by 5.1%, outperforming the S&P 500’s -0.8% return. Meanwhile, the bottom-ranked stocks decreased by -3.9%, resulting in a 9.0% return for the top decile minus the bottom decile long-short portfolio. Over the past five years, the top-ranked U.S. equities have gained nearly 120%, while the bottom-ranked portfolio has declined by approximately -50%.

AlphaRank Top Stocks represents Accelerate’s predictive equity ranking powered by proven drivers of return. Stocks with the highest AlphaRank are projected to outperform, while stocks with the lowest AlphaRank are anticipated to underperform. AlphaRank assigns a numeric value to each security, ranging from 0 (bottom-ranked) to 100 (top-ranked), based on selected predictive factors. All Canadian and U.S. stocks priced above $1.50 per share and with a market capitalization exceeding $100 million are evaluated. In both the Accelerate Absolute Return Fund (TSX: HDGE) and the Accelerate Canadian Long Short Equity Fund (TSX: ATSX), Accelerate funds may be long many top-ranked stocks and short many bottom-ranked stocks. See AccelerateShares.com for more information.