November 16, 2025 – With era-defining technological advancements come investment booms.

One of the first technology-driven investment booms in America was the railroad boom of the 1880s. At the time, the U.S. economy was undergoing rapid industrialization, with westward expansion creating demand for transportation. Investors believed railroads would become a growing and highly profitable infrastructure backbone, similar to how some investors today view artificial intelligence and data centers.

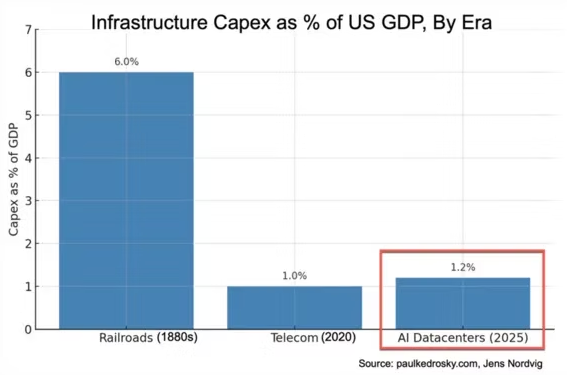

As capital poured into the sector, driven by a rational investment thesis that drove investor bullishness, the industry expanded rapidly. U.S. rail mileage nearly doubled between 1880 and 1890, built out by capital expenditures totalling an estimated 6% of GDP. To this day, the buildout of the railroads represents the largest industrial capital expenditure (“capex”) boom in American history.

As with most booms, speculative activity was rewarded in the market and was readily financed. As a result, many railroads built lines speculatively ahead of demand (i.e. railroads to nowhere). The rapid infrastructure buildout, which was heavily reliant on debt financing, resulted in overbuilding and a lack of pricing power due to too much competition. Ultimately, demand did not match the bullish market projections, ultimately leading to the industry’s collapse.

Roughly 70% to 80% of the trackage added in the 1880s entered receivership by 1900.

After the wipeout, the industry consolidated into a handful of large, rationalized systems, which continue as key drivers of economic growth to this day.

More than a hundred years later, another generational capex boom occurred.

In the 1990s, the internet revolution created expectations of exponential traffic growth on the “information superhighway”. With projections of ultrafast growth rates in internet traffic, investors were keen to ride the “new economy” growth wave. The internet was the future.

Capital market participants readily provided cheap capital to fund the buildout of internet infrastructure. U.S. telecom carriers tripled capex from 1996 to 2000. As a result, companies laid enough fiber to meet decades of demand (and enough fiber to circle Earth 4,000×).

Ultimately, some of the same issues that impacted the railroad boom 110 years prior were repeated with the internet infrastructure buildout. Market bullishness led to massive overcapacity, which was financed primarily with debt, and forecast demand was proven overly linear and too optimistic. In addition, as dozens of long-haul carriers raced to add capacity, excessive competition destroyed margins. Ultimately, when the internet bubble burst in 2000 to 2002, many of the largest internet infrastructure providers went bankrupt, devastating investors. Subsequently, the investment boom turned bust, with capital expenditures falling more than 60%.

However, the initial thesis proved correct, and the internet was the future. Internet users continue to enjoy the benefits of the capex boom 25 years later.

Artificial intelligence is one of the greatest technological revolutions in history. A foundational shift analogous to railroads in the 1880s or the internet in the 1990s, AI is expected to substantially automate and augment human labour across industries, driving productivity gains and unlocking new revenue streams. The opportunity is vast, and it is no surprise that investors are eager to participate and finance the AI infrastructure build out.

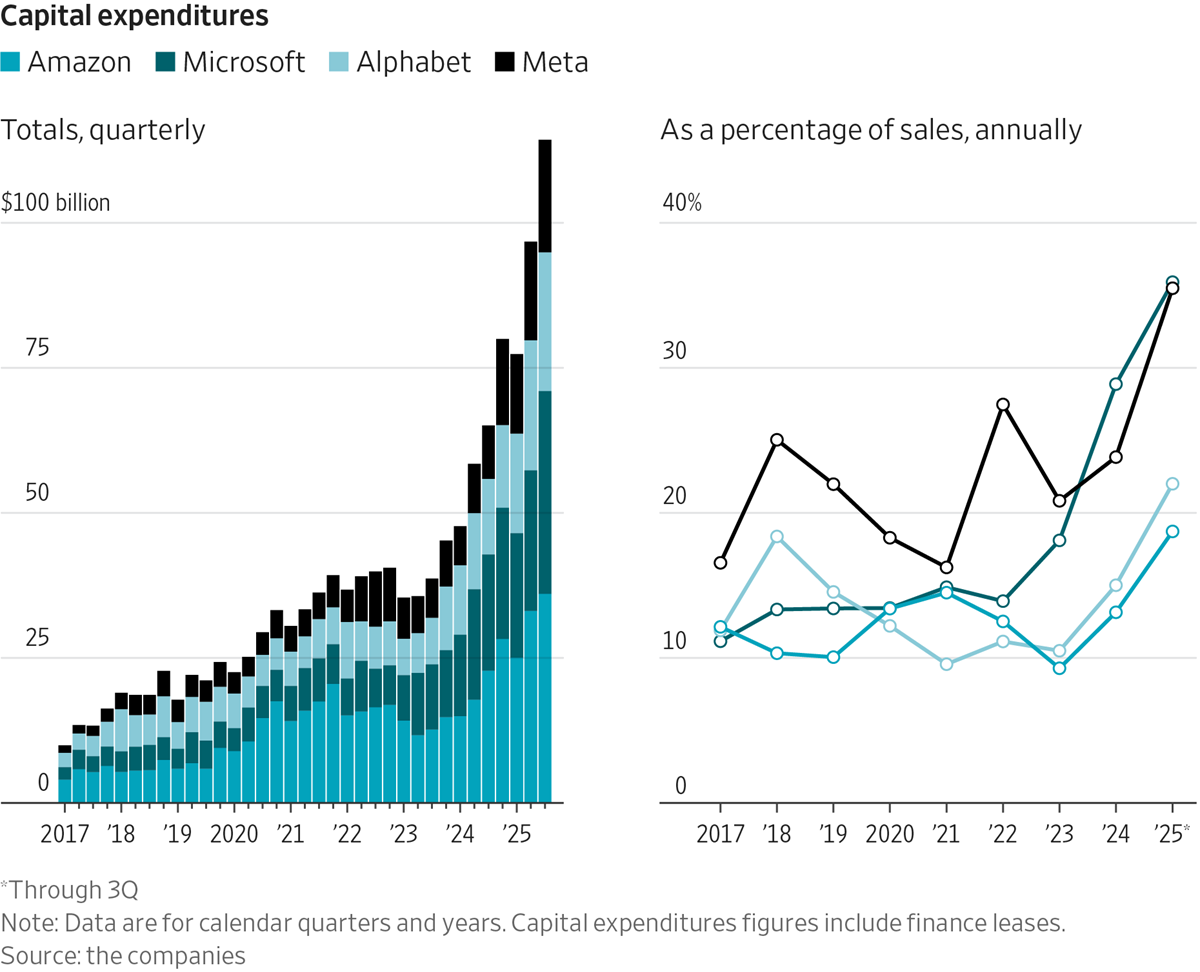

The hyperscalers, a group that includes Amazon, Microsoft, Google (Alphabet) and Meta, are among the market’s leading AI infrastructure providers. This group of massive technology companies is expected to spend $370 billion this year on AI infrastructure, totalling an estimated 1.2% of GDP.

While this level of investment is significant, thus far it pales in comparison to the capex boom that built America’s rail network.

However, AI-related capex is forecast to increase dramatically over the coming years. Research analysts at JPMorgan project that total investment in global AI infrastructure through 2030 will amount to $5 trillion. If this level of investment is attained, it will dramatically exceed the previous record railroad capex boom from nearly 150 years ago.

These analysts calculated that in order to achieve a relatively modest 10% return on capital, AI products would have to create an additional $650 billion of revenue per year, indefinitely. That is a far cry from market-leader OpenAI’s current revenue of approximately $20 billion.

Moreover, AI-related companies have issued approximately $170 billion of debt so far this year to fund data centers, representing more debt than they issued over the past three years combined. The use of leverage reduces a firm’s margin of safety and can result in problems if demand does not meet forecasts.

With this boom, the hyperscalers are significantly increasing their capital expenditures as a percentage of sales, more than doubling over the past several years. These technology companies, which have historically had attractive asset light business models focused on selling software, are shifting to asset heavy business models that emphasize capital intensity and AI infrastructure investment.

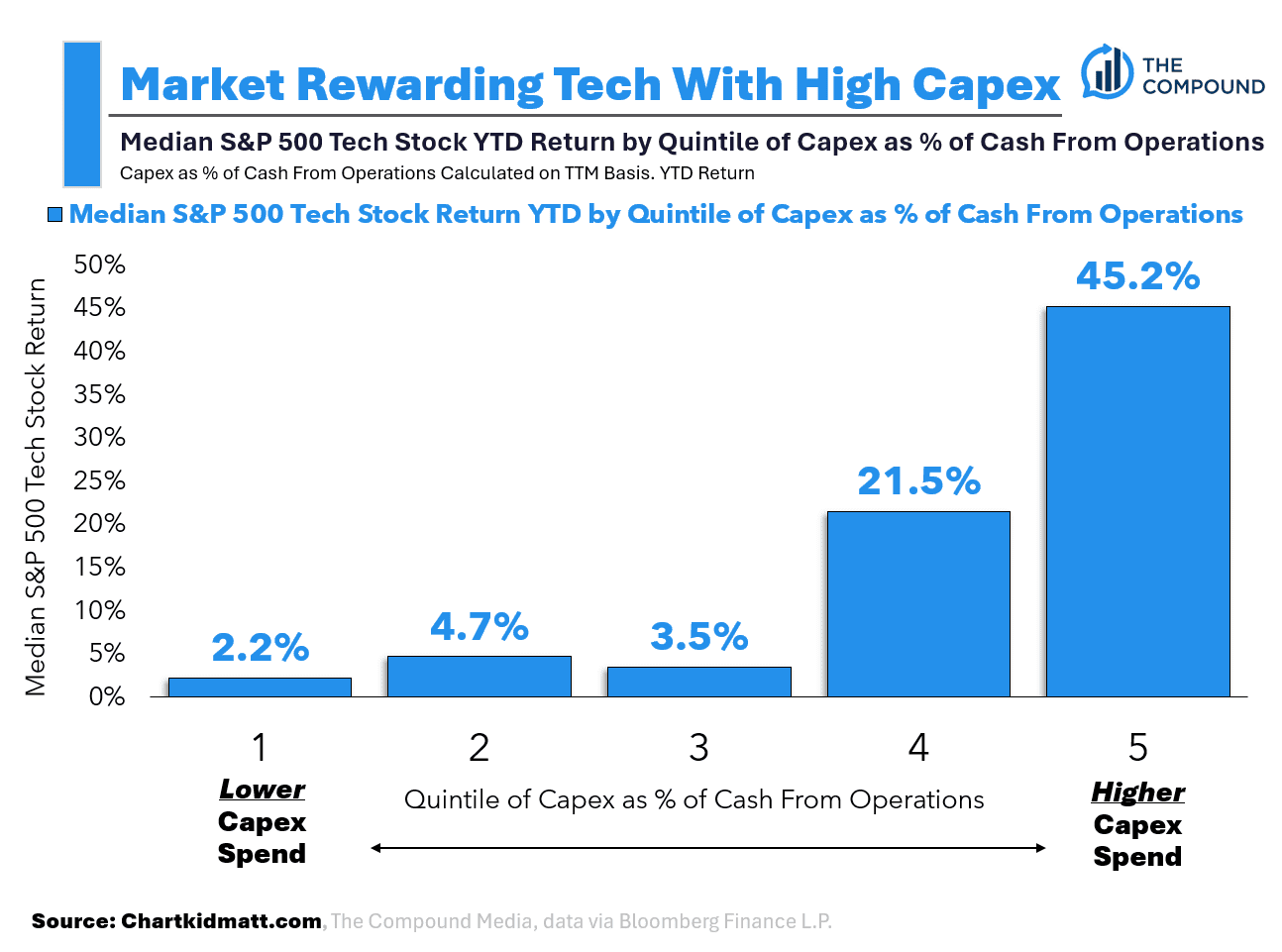

Thus far, the market has rewarded AI-related capex spending. Year-to-date, S&P 500 tech stocks that have spent the most on capex as a percentage of their cash flow have enjoyed a median share price performance of more than 45%. Investor sentiment related to spending on AI infrastructure remains positive, and therefore, rational actors will continue to follow this trend. As Citigroup’s former CEO Chuck Prince said regarding participating in a bull market, “as long as the music is playing, you’ve got to get up and dance.”

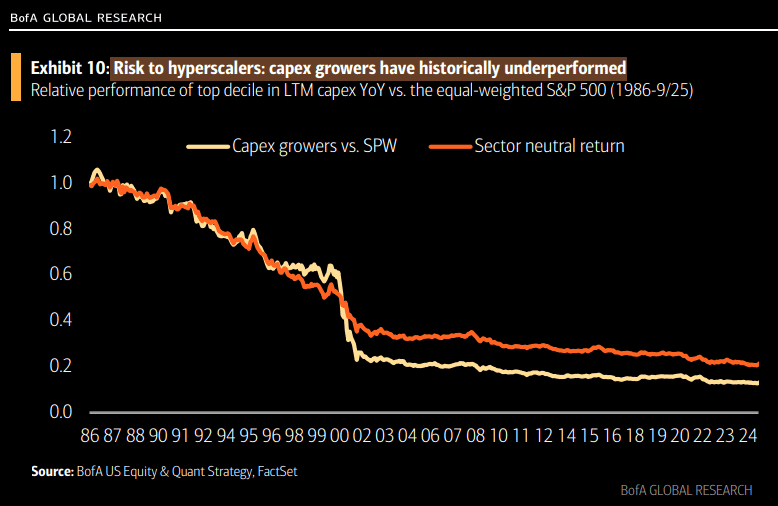

However, investor caution is warranted as the market’s largest stocks transition from asset light to asset heavy business models, supported by rapidly growing capex. Historically, capex growers have dramatically underperformed the market.

Capex growers such as the railroad companies of the 1880s and telecom companies of the 1990s suffered the same fate – dramatic share price underperformance, with many ultimately resulting in a total loss for investors.

Initially, the underpinning rationale for investing in era-defining technological advancements makes sense. World-changing technology ultimately ends up, well, changing the world.

That said, as the market’s leading AI companies dramatically ramp up their capital expenditures with the goal of winning the AI race, investors should tread lightly given the track record of past capex booms.

AI has clear echoes of past capital cycles, including the fastest capex ramp in history, speculative spending on data centers built ahead of steady revenue models, GPU shortages creating a false sense of scarcity that results in overordering, and an unclear determination of return on investment as the cost of inference rapidly declines. If forecasts of AI use prove overly optimistic, the capex boom may have lasting consequences for the market.

Accelerate manages five alternative investment solutions, each with a specific mandate:

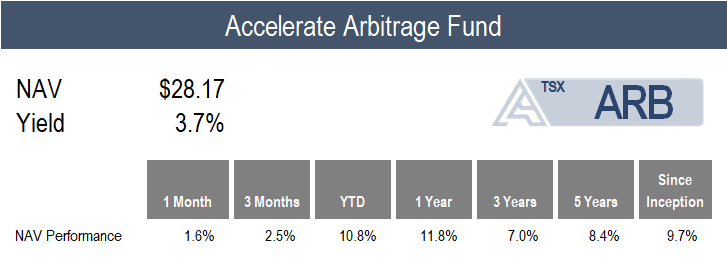

- Accelerate Arbitrage Fund (TSX: ARB): Merger Arbitrage

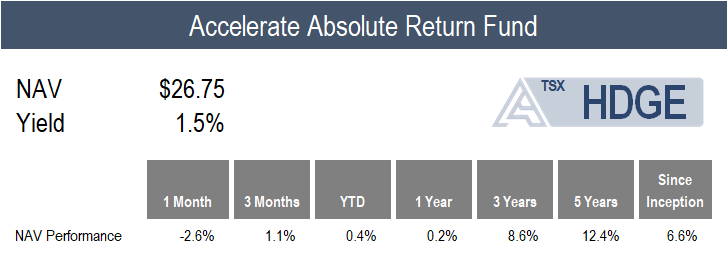

- Accelerate Absolute Return Fund (TSX: HDGE): Absolute Return

- Accelerate OneChoice Alternative Multi-Asset Fund (TSX: ONEC): Multi-Asset

- Accelerate Canadian Long Short Equity Fund (TSX: ATSX): Long Short Equity

- Accelerate Diversified Credit Income Fund (TSX: INCM): Private Credit

ARB gained 1.6% in October, compared with the benchmark S&P Merger Arbitrage Index’s 3.1% rise.

The M&A environment remains highly prospective for merger arbitrage, with a significant amount of deals coming to market. During the month, twenty-nine public mergers were announced in North America. Of these, ARB participated in five. In addition, fourteen SPAC IPOs came to market, of which ARB participated in seven.

Currently, ARB is 151.9% long and -10.2% short (162.1% gross), with 67% allocated to SPAC arbitrage and 33% to traditional merger arbitrage (including 18% to strategic M&A and 15% to leveraged buyouts).

We are pleased to announce that the Accelerate Arbitrage Fund (TSX: ARB) has been awarded a Top 3 global hedge fund performance ranking in the Merger Arbitrage category, as featured in the latest Barclay Managed Funds Report.

![]()

HDGE declined -2.6% in a challenging month for short selling.

Long-short factor performance was negative in October, as overvalued and low-quality securities outperformed undervalued and high quality stocks. Accordingly, the GS Most Shorted basket gained 10.6% for the month, while the GS U.S. Hedge Fund VIP basket ticked up by just 0.9%, leading to a -9.6% monthly drop for the long short hedge fund proxy.

Top Fund contributors for the month include a long position in Celestica and Cardinal Health, along with a short position in LGI Homes. Top Fund detractors include a long position in Adtalem Global Education, and short positions in Ichor Holdings and NeoGenomics.

![]()

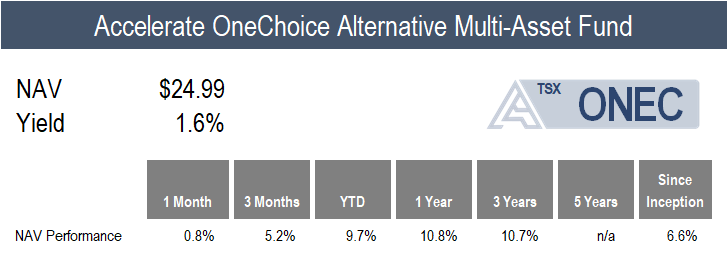

ONEC gained 0.8% in a month that featured wide dispersion in performance across alternative asset classes.

Leading the pack with a 4.8% rise was the Fund’s gold allocation. Positive contributors also include managed futures, which gained 3.8%, private credit, which generated a 2.2% return, and risk parity, which added 1.9%. Additionally, the Fund’s allocations to merger arbitrage, commodities, and leveraged loans generated positive returns of 1.6%, 1.5%, and 0.4%, respectively.

Monthly detractors in the ONEC portfolio include absolute return, infrastructure, real estate, and long-short equity, which declined by -2.6%, -2.0%, -1.6%, and -0.1%, respectively.

![]()

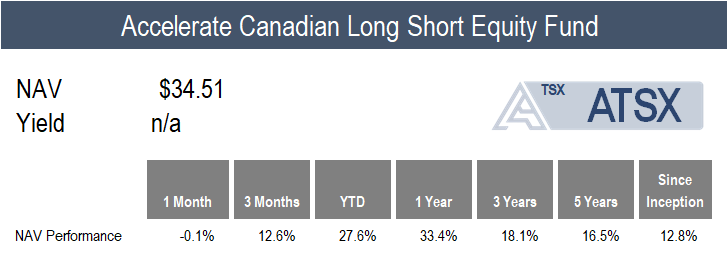

ATSX declined -0.1% in October compared to the benchmark S&P/TSX 60’s 0.8% increase.

Canadian long-short factor performance was challenged last month, primarily driven by the significant outperformance of low-quality and overvalued stocks.

Top Fund contributors for the month include long positions in Aritzia, Finning International, and Celestica. Top Fund detractors include short positions in TransAlta, Aecon Group, and Brookfield Renewable Partners.

![]()

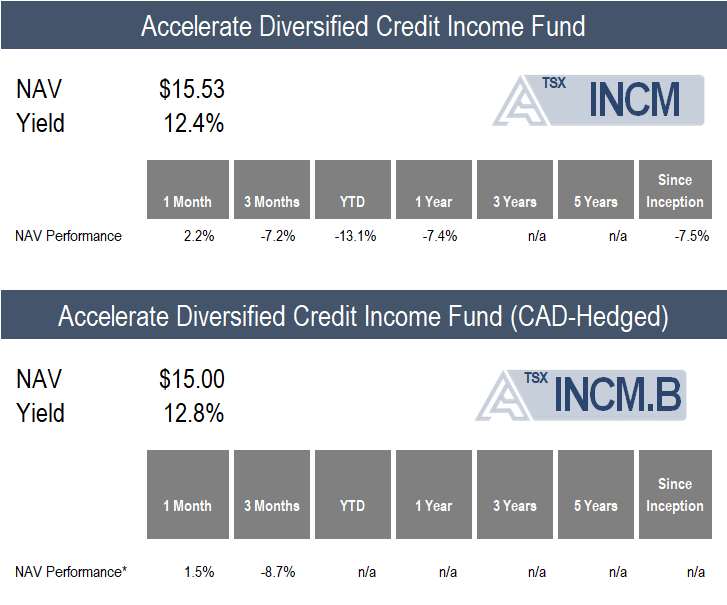

INCM generated a 2.2% return for the month (1.5% in CAD-hedged terms) primarily generated by the portfolio’s yield, as NAV discounts remained significant and widespread.

While sentiment in private credit remains deeply negative, recent fundamental credit performance has been relatively strong. The largest listed private credit fund (and INCM’s largest position), Ares Capital, reported its Q3 results at the end of October. Ares’ Q3 performance was compelling, with a rising NAV, declining non-accruals, declining PIK income, and rising capital deployment with stable spreads. The remainder of INCM’s private credit portfolio is reporting its third quarter results throughout the first half of November, and a thorough analysis will be provided in the upcoming weeks.

Currently, INCM is allocated to 20 listed private credit funds, which hold more than 5,000 loans and investments. Of these loans, 86.6% are secured and 92.5% are floating rate, with a weighted average yield of 12.5%. INCM currently trades at a -16.9% discount to the underlying net asset value of its loan pools.

![]()

Have questions about Accelerate’s investment strategies? Click below to book a call with me:

-Julian

Disclaimer: This distribution does not constitute investment, legal or tax advice. Data provided in this distribution should not be viewed as a recommendation or solicitation of an offer to buy or sell any securities or investment strategies. The information in this distribution is based on current market conditions and may fluctuate and change in the future. No representation or warranty, expressed or implied, is made on behalf of Accelerate Financial Technologies Inc. (“Accelerate”) as to the accuracy or completeness of the information contained herein. Accelerate does not accept any liability for any direct, indirect or consequential loss or damage suffered by any person as a result of relying on all or any part of this research and any liability is expressly disclaimed. Past performance is not indicative of future results. Visit www.AccelerateShares.com for more information.